And When Was the Last Time You Checked Your Long/Short Fund’s Correlation to the S&P?

January 30, 2018

Diversification. That’s the expected benefit of adding an equity alternative fund to a portfolio. The test of any alternative mutual fund must be: Is it sufficiently non-correlated to reduce the risk of a traditional stock and bond portfolio?

Financial advisors, there’s no time like now to be thinking about the overall correlation of allocations within clients’ portfolios. Risk assets have had an extended, strong run and a pullback could be imminent. At the same time, it makes sense to confirm that what you think are less correlated assets are in fact less correlated.

A November 2017 Steben & Company whitepaper raised the question about the effect of a net long bias in the equity and credit exposures of many hedge funds.

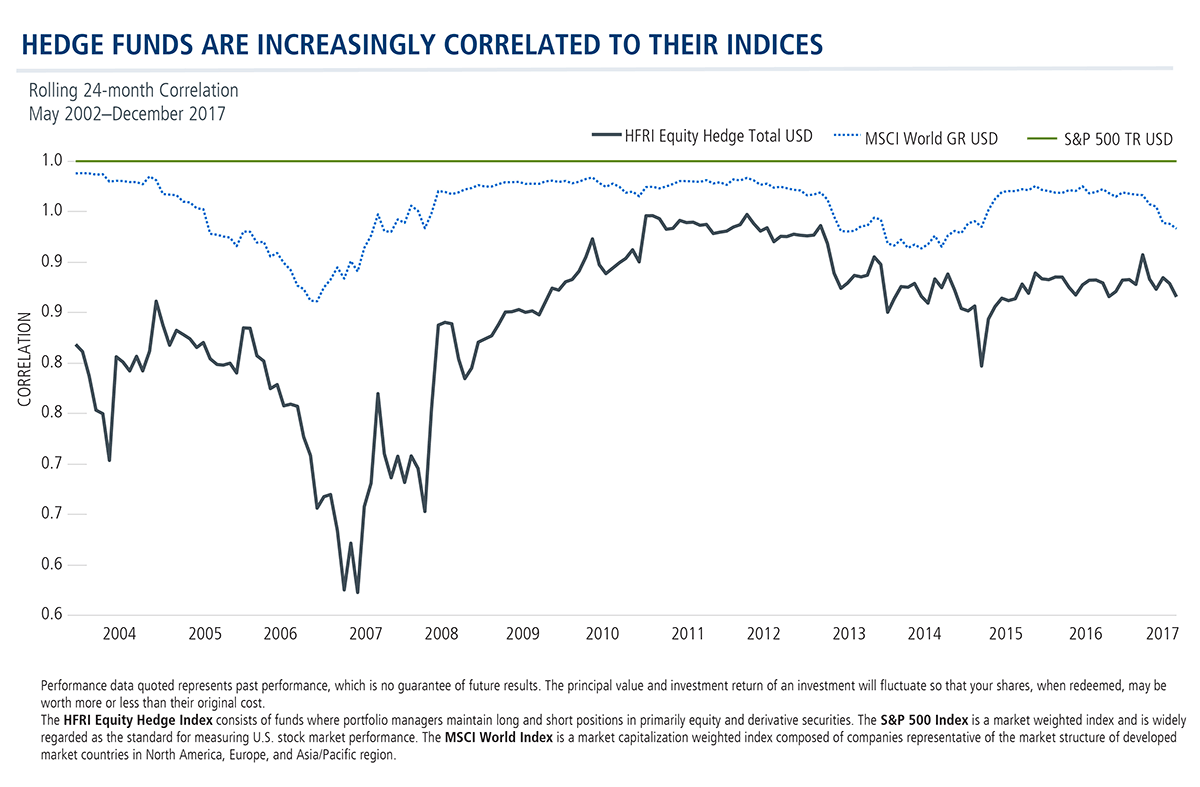

“Prior to the 2008 financial crisis, the correlation [between the HFRI Fund Weighted Composite Index and the S&P 500 Index] ranged between 0.4 and 0.8. But in the post-crisis bull market the correlation has floated at a higher level of 0.8 to 0.9,” Steben wrote.

Here’s what the HFRI Equity Hedge Index looks like, including as correlated to the MSCI World Index and S&P 500 Index.

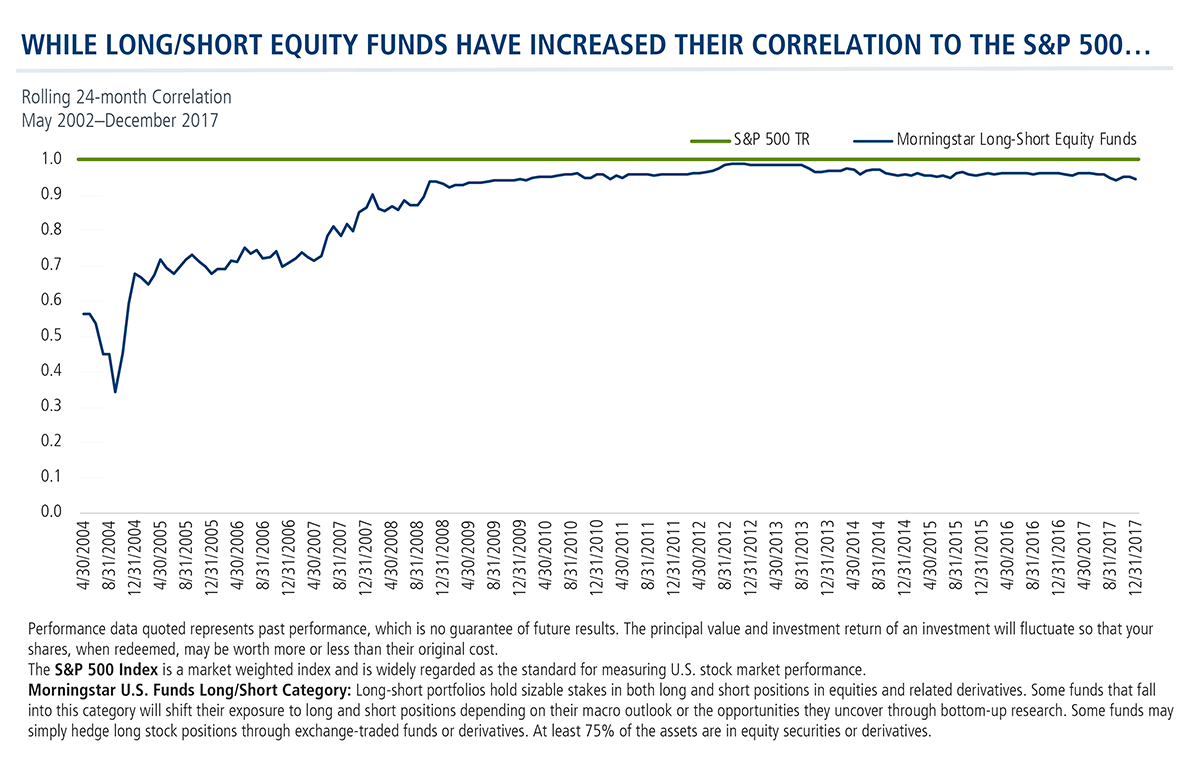

A look at the correlations between the S&P 500 and the Morningstar Long/Short Equity Funds category shows a similar trend since 2010—high correlations between the alts group and the broad market index.

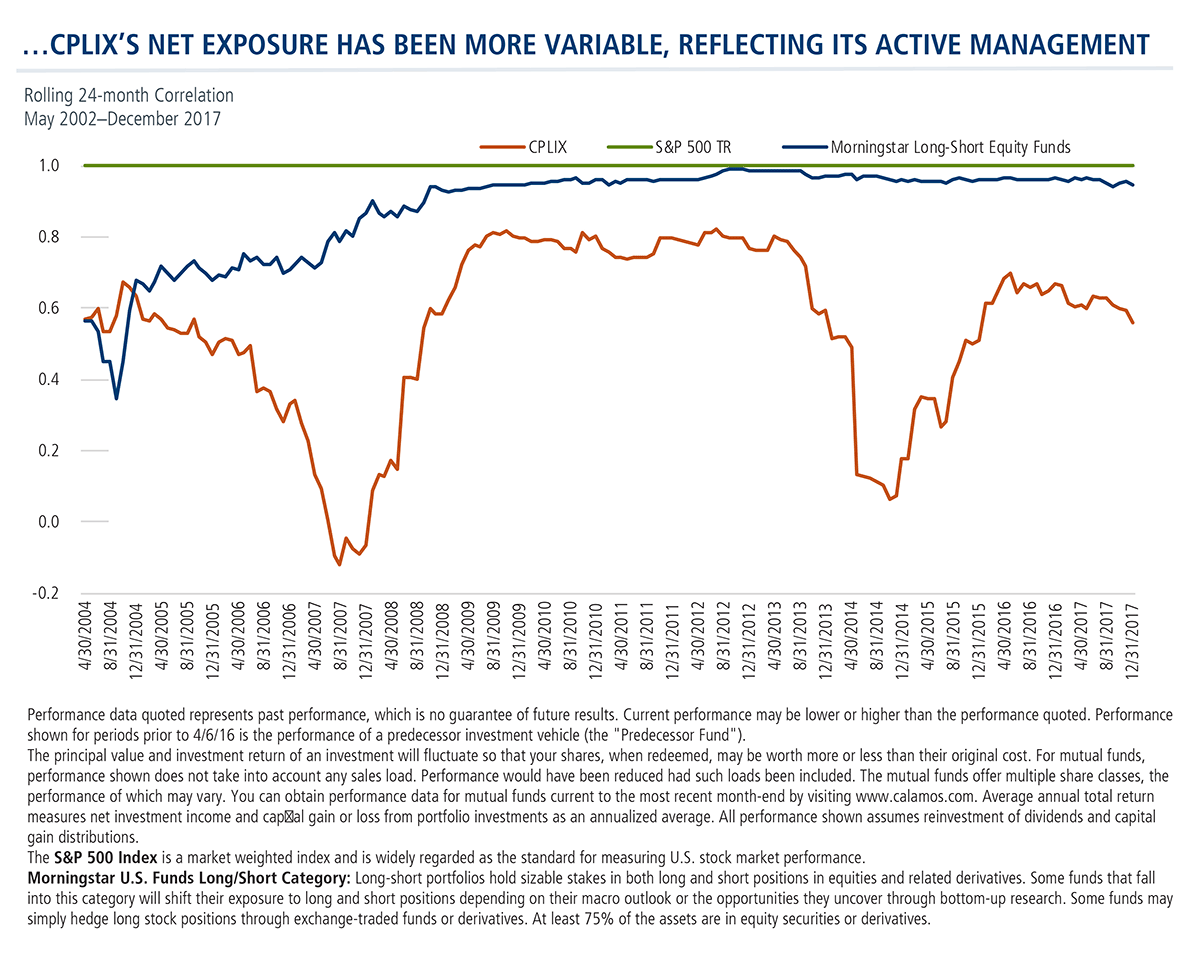

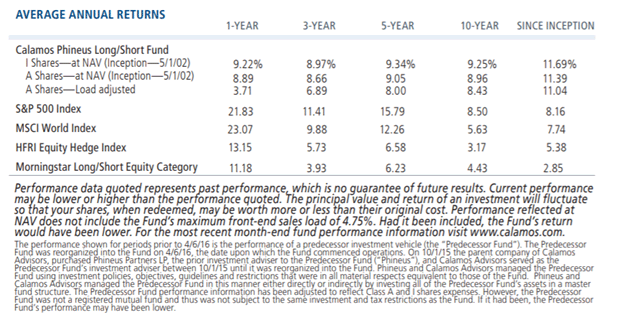

Financial advisors tell us that what they like about Calamos Phineus Long/Short Fund (CPLIX) is that it’s being managed as they’d expect. As of December 31, 2017, since the fund's inception, CPLIX’s correlation to the S&P 500 was 0.6. Compare that to its peer group’s 0.9 correlation to the S&P 500.

This illustration of CPLIX’s variable correlations with the broad equity market over time demonstrates active management at work and hints at the contribution the fund can make in an investment portfolio. (For background, see an older post: Using ETFs to Manage Long and Short Exposure.)

CPLIX has been able to provide equity-like performance with significantly lower correlations to equity markets relative to its peers, diversifying the equity exposure in a portfolio.

Financial advisors, for more information about CPLIX and how it could help you manage your clients' risk exposure, talk to a Calamos Investment Consultant at 888-571-2567 or email caminfo@calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Data as of 12/31/17

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, options risk, and leverage risk.

Class I shares are offered primarily for direct investment by investors through certain tax-exempt retirement plans (including 401(k) plans, 457 plans, employer-sponsored 403(b) plans, profit sharing and money purchase pension plans, defined benefit plans and non-qualified deferred compensation plans) and by institutional clients, provided such plans or clients have assets of at least $1 million. Class I shares may also be offered to certain other entities or programs, including, but not limited to, investment companies, under certain circumstances.

Alternative investments may not be suitable for all investors, and the risks of alternative investments vary based on the underlying strategies used. Many alternative investments are highly illiquid, meaning that you may not be able to sell your investment when you wish to.

Active management does not guarantee investment returns or eliminate the risk of loss.

Unmanaged index returns assume reinvestment of any and all distributions and do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in an index.

The S&P 500 Index is a market weighted index and is widely regarded as the standard for measuring U.S. stock market performance.

The MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of developed market countries in North America, Europe, and Asia/Pacific region.

The HFRI Equity Hedge Index consists of funds where portfolio managers maintain long and short positions in primarily equity and derivative securities.

Morningstar U.S. Funds Long/Short Category: Long-short portfolios hold sizable stakes in both long and short positions in equities and related derivatives. Some funds that fall into this category will shift their exposure to long and short positions depending on their macro outlook or the opportunities they uncover through bottom-up research. Some funds may simply hedge long stock positions through exchange-traded funds or derivatives. At least 75% of the assets are in equity securities or derivatives.

800997 118