Investment Team Voices Home Page

Investment Team Voices Home Page

Welcome Back, Mr. Bond

Michael Grant, Co-CIO

October 26, 2023

- Real interest rates have reached their highest levels in decades. As investors grapple with the implications, bond markets may be signaling more economic resilience in 2024.

- One consequence is a less favorable liquidity backdrop for financial asset prices. However, the economic implications are more nuanced because absolute levels of economic liquidity appear abundant.

- “Higher for longer” will squeeze parts of the economy and set the stage for a downturn in 2025. For now, we believe equities are digesting a classic mid-cycle correction rather than “end-of-cycle.”

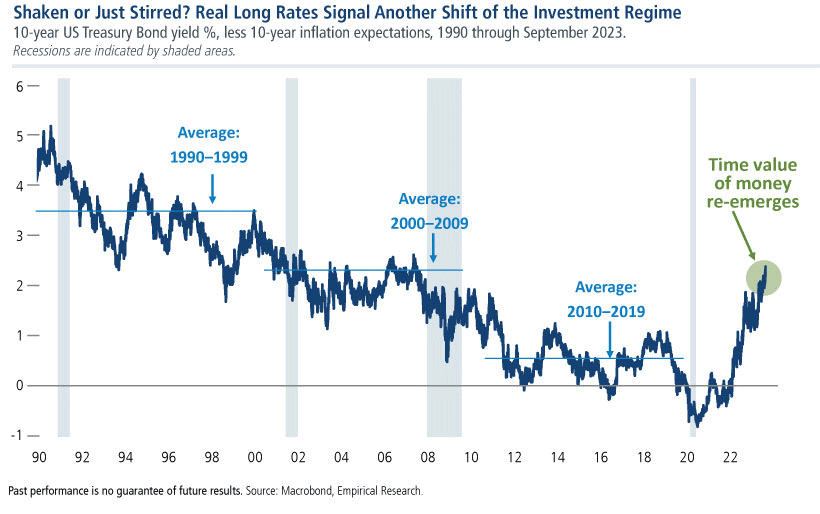

Unprecedented low interest rates and central bank distortions have been the hallmark of the post-2008 era. The past quarter was notable for the gathering sense that this landscape is giving way to something very different, with real interest rates attaining their highest levels in more than two decades. Investors are naturally grappling with the implications of this latest “new normal.”

See Michael Grant's quarterly update for his complete market commentary and outlook, plus the latest performance and positioning for the Calamos Phineus Long/Short Fund.

The short explanation for the rise in rates is the resiliency of the US economy and of consumer incomes in particular. Recession risk has remained remarkably low in 2023 and may well remain low through 2024. This recession deferred may be why the equity correction has been orderly despite the headwinds of the spring banking crisis, the housing recession, and the acute pause in technology spending.

Put another way, yields are rising because they can and may signal the sustainability of today’s economic expansion. Rather than fueling waves of asset price distortion, positive real rates channel capital into productive uses and thus to higher real wages and higher real returns. Unsurprisingly, unwinding the legacy of unnaturally low interest rates is a transition, and markets are in the midst of pricing this risk.

One consequence is a less favorable liquidity backdrop for financial asset prices. However, the implications for the economy are more nuanced because absolute levels of economic liquidity appear abundant. The prima facie evidence is the pristine condition of private sector balance sheets. In effect, liquidity is being drawn from the financial system and into the economy: good news for Main Street, less good for Wall Street.

Another feature of this setting is that the rate sensitivity of the US economy is an echo of prior decades. Both consumers and corporates refinanced their debt obligations through the pandemic, and the rise in rates has therefore had minor effects on spending. For example, net debt servicing costs for US corporates has declined in 2023 because of the weighty share of firms with net cash positions.1

Something that undermines the business sector will likely be the catalyst of an eventual downturn. Yet this is hard to conceive given today’s healthy profitability and balance sheets of larger corporates.2 While fixed investment has been an important tailwind in 2023, this spending has not been financed by increased leverage. The “financing gap”3 for the corporate sector remains at historically low levels.

The data underline what is truly unusual about today’s economic landscape: There is a remarkable absence of the late-cycle excesses that would normally be the ingredients for a cyclical downturn. Of course, these aggregates do not capture the reality that rate pressures are troublesome for some parts of the economy. We view these pressures as more chronic than acute for the business cycle in 2024.

Housing is an example of this dichotomy. Housing sales and affordability have collapsed to the deep recessionary levels of the 2009 era, yet home prices and housing starts have proven resilient. Underlying demand relative to supply appears very favorable, with positive implications for when the rates’ pressures ease. In other words, the conditions are ripe for a softer landing on the recuperative side of today’s bond massacre.

All of this contrasts with the vulnerabilities of an aged or mature expansion. A tight labor market is often associated with late-cycle risk, yet there is an absence of the usual spending or borrowing excesses. In prior cycles, these included an overextension of spending on housing and autos, rising leverage across households and corporates alike, and downward pressure on profit margins. So far, little of this is apparent.

Of course, this aggregate data hides the harsher truth that parts of the economy are under duress due to normalized interest rates. This contrast between the broader economy and its interest-sensitive parts may provide insight into how the remaining years of this expansion unfold. These stresses can moderate activity, which is our forecast for 2024. Yet it is difficult to conceive how they might cascade into recession-like conditions.

Inflation dynamics are an essential part of this outlook. The stunning disinflation of the past year has turned a potential crisis for the business cycle into a mild irritant. Chairman Powell is unlikely to declare victory anytime soon, which implies policy will continue to lean against economic growth. Nonetheless, the Federal Reserve can be responsive to any financial or economic breakage as and when it appears.

The timing of the next recession is hard to predict because so much of todays’ landscape is “different this time.” Higher lending rates and tighter bank standards have been blunted by healthy balance sheets and robust corporate earnings. Recession may come later than many expect as the drag of higher rates is offset by fading supply shocks, the legacy of pandemic savings, and pro-cyclical fiscal support.

Bond Markets Rarely Lie, So What Are They Telling Us?

Real interest rates have risen more than 100 basis points in 2023, with much of this move occurring since June. While equities have struggled in the past quarter, the pullback has been orderly and for the major equity benchmarks, underwhelming given the sizable move in rates. Either investors do not believe this rate move will prove long lasting, or markets are telling us there is a new resiliency to the economic outlook.

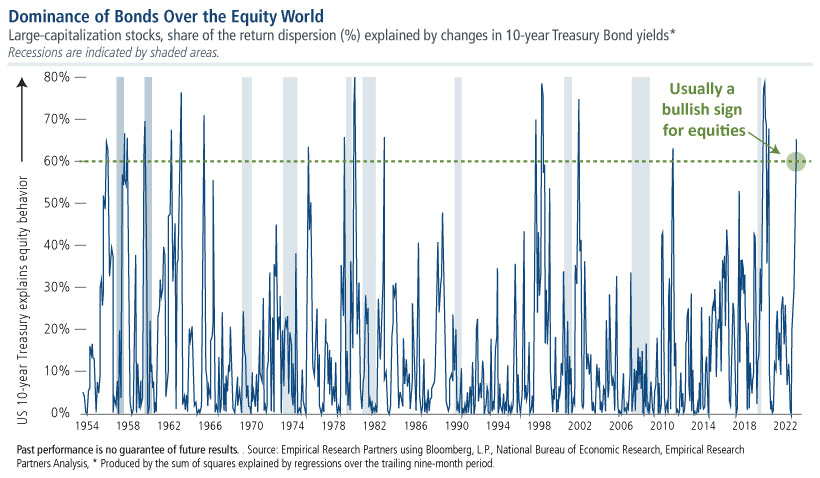

Bond markets rarely lie. The US 10-year yield has explained almost two-thirds of the cross-equity return distributions4 in 2023—one of the highest readings in six decades.5 This implies that rate pressures are becoming acute in parts of the economy regardless of its supportive features. These pressures need to culminate soon in a manner that moderates economic activity and eases financial conditions into 2024.

For the Calamos Phineus Long/Short Fund (CPLIX), positioning turned defensive in July on the assumption that the disinflation narrative had run its course. The US 10-year yield has held center stage since, and we anticipate a cycle peak near current levels of 5%. In short, today’s rate pressures are creating their own conditions for some modest respite, and in the absence of recession this degree of dominance by bonds over equities has historically proven a bullish sign.

Financial markets are mirrors of economic life, and tracing their behavior to a single thread of reason can be hard. However one might disaggregate the causes and effects of today’s rate moves, “higher for longer” will squeeze parts of the economy and set the stage for a downturn in 2025. For now, we believe equities are digesting a classic mid-cycle correction that investors can tactically lean into entering 2024.

Beyond some modest upside for equities into spring (S&P 500 target of 4500), investors should consider how a normalized setting for interest rates—with a normalized US 10-year yield of 5%—impacts the contours of our industry. We see a more cyclical setting for financial asset prices, with equities trading within a broad multi-year range and the US 10-year yield challenging both its 6% upper and 4% lower boundaries in coming cycles.

Welcome back, Mr. Bond.

Michael Grant, Co-CIO

1Firms with more cash than debt have benefited from higher interest income that has offset higher interest expense. For US consumers, the embedded mortgage servicing cost of 3.6% is about half the current mortgage rate of 7% plus.

2With its predominance of fixed-rate debt, larger-cap companies have a circumscribed exposure to higher rates; more than 40% of their fixed-rate debt matures beyond 2030. Less than 20% of debt for S&P 500 companies is rate sensitive versus about 35% for small-cap stocks.

3The degree to which private non-residential capital investment is funded by savings versus borrowings.

4The aggregate of individual stock deviations of performance versus the equity benchmark and the degree to which these deviations are correlated (or explained) by movements in the US 10-year yield.

5Today’s result ranks in the top 15 readings of the past 70 years and more than 4X the average of that period.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee a profit or protect against a loss. Alternative strategies entail added risks and may not be appropriate for all investors. Indexes are unmanaged, not available for direct investment, and do not include fees and expenses.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, Alternative investments may not be suitable for all investors. The fund takes long positions in companies that are expected to outperform the equity markets, while taking short positions in companies that are expected to underperform the equity markets and for hedging purposes. The fund may lose money should the securities the fund is long decline in value or if the securities the fund has shorted increase in value, but the ultimate goal is to realize returns in both rising and falling equity markets while providing a degree of insulation from increased market volatility.

82228 1023