Our Alternative Funds Work

December 4, 2017

Alternative funds have taken their lumps recently as commentators have criticized the performance of some funds launched in the aftermath of the 2008 financial crisis as a noncorrelated antidote to traditional stock and bond funds.

This post isn’t about that criticism or funds that have disappointed.

Rather, we offer our income and equity alternative funds as examples of how liquid alt funds can and do work.

Here’s a quick look at why and how our funds defy some of the broad generalizations being made about alternative mutual funds.

Calamos’ Bona Fides as an Alternative Manager

At the core of our funds’ effectiveness is our heritage: John P. Calamos, Sr. founded Calamos Investments 40 years ago to provide innovative strategies for managing risk and enhancing investment returns. John pioneered the use of convertible securities when they were essentially an alternative asset class.

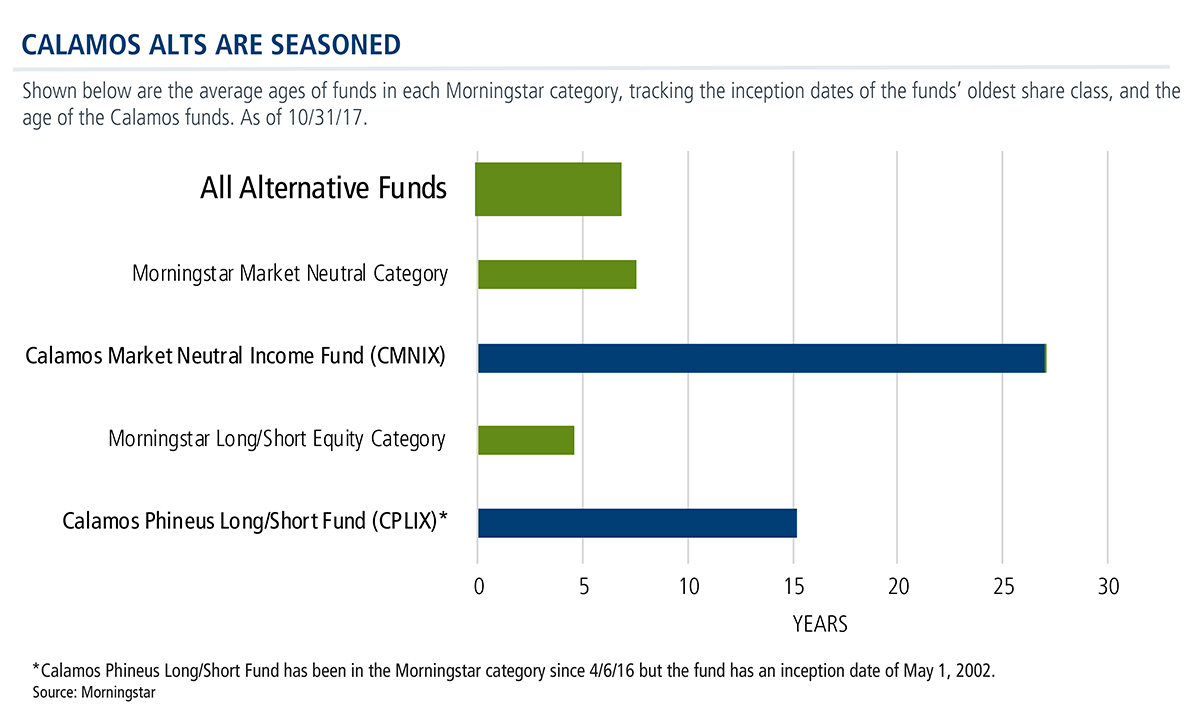

Surviving the Test of Time

Calamos Market Neutral Income Fund (CMNIX) debuted in 1990, making the 27-year-old fund one of the first liquid alternatives. The rich history of Calamos Phineus Long/Short Fund (CPLIX) dates back to 2002 (see post).

By contrast, the average alternative fund tracked by Morningstar is less than seven years old—so have yet to be tested by ugly markets.

In Pursuit of Consistent Strategies

Long track records, of course, enable financial advisors to evaluate funds’ performance over multiple market cycles. Equally important: The funds’ performance results were achieved using essentially the same strategies employed today.

CPLIX has been managed by the same portfolio manager, Michael Grant, since its 2002 inception, and the strategy components of CMNIX have been relatively consistent for almost three decades.

Investment Results

See this post for more on CMNIX’s performance consistency and this post for CPLIX’s consistent performance.

CMNIX has earned a ????? overall rating in the Morningstar Market Neutral funds category of 112 funds based on risk-adjusted returns as of 9/30/17.

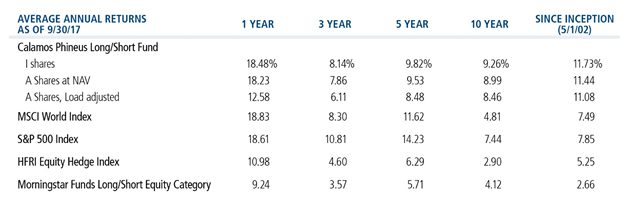

Calamos ranks CPLIX in the 1st percentile within the Morningstar U.S. Funds Long/Short Category and has outperformed both the Standard & Poor’s 500 Index and MSCI World Index since its May 2002 inception for the period ended 9/30/17.¹

Steering Clear of Blow-ups

An alternative fund can serve as a portfolio ballast in bear markets. But at all times, our alts are focused on the risks inherent in any market.

With our income alternative CMNIX, the goal is to “take advantage of the opportunities the market presents,” says Senior Co-Portfolio Manager Eli Pars.

Its blend of covered call writing and convertible arbitrage strategies has led to a lower risk profile and attractive returns due to the strategies’ differing responses to volatility.

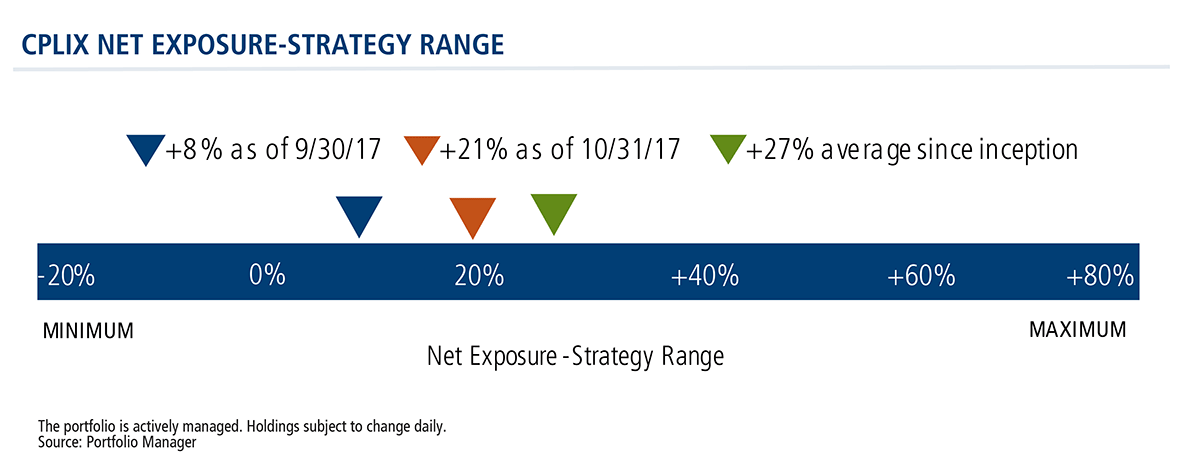

As an equity alternative, CPLIX benefits from being able to go long or short.

Investors need to take risk, insists Grant. “[Investors] are paid to take risk. Equities are a favorable asset class because when you take risk, the expectation is greater return. A lot of investors lose sight of that and they over-diversify and then they stop taking risk and they wonder why there’s no return.”

“The advantage of the long/short model and the ability to short,” Grant continues, “is to take off some equity tails, volatile, downside moments when it becomes very hard to believe in the long-term story for equities. The long/short model gives us the flexibility to implement that.” (For more, see The Long/Short Model video.)

Over the 15 years since the fund’s inception, the fund has achieved its returns with an average net exposure of approximately 27%. (For more, see Using ETFs to Manage Long and Short Exposure.)

Mindful of Expenses

Our alternative funds offer nontraditional strategies without the hedge fund pricing.

In fact, CMNIX—the largest fund in Morningstar’s Market Neutral category—has one of the lowest expense ratios in its Morningstar category or across all alternatives tracked by Morningstar (data as of 9/30/17). For more, see Not Every Alternative Fund Is Pricey.

CPLIX has an expense cap in place.

We started 2017 as the #10 manager of assets in the Alternatives category tracked by Morningstar. By the end of the third quarter, we were the 8th manager by AUM (Morningstar, 9/30).

We attribute this growth to broadening platform availability, growing advisor support and the funds’ continued performance as expected. We are committed to demonstrating the contribution that can be made by allocating up to 20% of clients’ portfolios to alternatives (for one idea, see this post).

Advisors, for more information on how our alternatives work, please talk to your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 2.25%. Had it been included, the Fund’s return would have been lower. For the most recent month-end fund performance information visit www.calamos.com.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. For the most recent month end performance information click on the performance tab.

The performance shown for periods prior to 4/6/16 is the performance of a predecessor investment vehicle (the “Predecessor Fund”). The Predecessor Fund was reorganized into the Fund on 4/6/16, the date upon which the Fund commenced operations. On 10/1/15 the parent company of Calamos Advisors, purchased Phineus Partners LP, the prior investment adviser to the Predecessor Fund (“Phineus”), and Calamos Advisors served as the Predecessor Fund’s investment adviser between 10/1/2015 until it was reorganized into the Fund. Phineus and Calamos Advisors managed the Predecessor Fund using investment policies, objectives, guidelines and restrictions that were in all material respects equivalent to those of the Fund. Phineus and Calamos Advisors managed the Predecessor Fund in this manner either directly or indirectly by investing all of the Predecessor Fund’s assets in a master fund structure. The Predecessor Fund performance information has been adjusted to reflect Class A and I shares expenses. However, the Predecessor Fund was not a registered mutual fund and thus was not subject to the same investment and tax restrictions as the Fund. If it had been, the Predecessor Fund’s performance may have been lower.

Calamos Phineus Long/Short Fund performance shown is net of fees based on 1.75% total expense ratio. This expense ratio is comparable to the expected expense cap on I-Share class. The U.S. OE Long/Short Category performance is based on the category average.

Calamos Market Neutral Income Fund’s load-waived Class I shares received 4 stars for 3 years, 5 stars for 5 years, and 5 stars for 10 years out of 112, 74 and 34. Market Neutral funds, respectively, for the period ended 9/30/17.

¹The percentile rankings illustrated are created by Calamos Financial Services LLC. The percentile rank measures the Fund’s total return among the Morningstar U.S. Funds Long/Short Category. The percentile rank shown for periods prior to 4/6/16 is the percentile rank of a predecessor investment vehicle (the “Predecessor Fund”). The Predecessor Fund was reorganized into the Fund on 4/6/16. The Fund is included in the Morningstar U.S. Fund Long/Short category as of 4/6/16. This is the fund's total-return percentile rank relative to all funds that have the same category for the same time period.

Some of the risks associated with investing in alternatives may include hedging risk–hedging activities can reduce investment performance through added costs; derivative risk–derivatives may experience greater price volatility than the underlying securities; short sale risk - investments may incur a loss without limit as a result of a short sale if the market value of the security increases; interest rate risk–loss of value for income securities as interest rates rise; credit risk–risk of the borrower to miss payments; liquidity risk–low trading volume may lead to increased volatility in certain securities; non-U.S. government obligation risk–non-U.S. government obligations may be subject to increased credit risk; portfolio selection risk – investment managers may select securities that fare worse than the overall market. Alternative investments may not be suitable for all investors.

Class I shares are offered primarily for direct investment by investors through certain tax-exempt retirement plans (including 401(k) plans, 457 plans, employer-sponsored 403(b) plans, profit sharing and money purchase pension plans, defined benefit plans and non-qualified deferred compensation plans) and by institutional clients, provided such plans or clients have assets of at least $1 million. Class I shares may also be offered to certain other entities or programs, including, but not limited to, investment companies, under certain circumstances.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

Covered Call Writing: As the writer of a covered call option on a security, the fund foregoes, during the option’s life, the opportunity to profit from increases in the market value of the security, covering the call option above the sum of the premium and the exercise price of the call.

Convertible Securities Risk: The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors also, may have an effect on the convertible security’s investment value.

Convertible Arbitrage Risk: If the market price of the underlying common stock increases above the conversion price on a convertible security, the price of the convertible security will increase. The fund’s increased liability on any outstanding short position would, in whole or in part, reduce this gain.

The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, options risk, and leverage risk.

Citigroup 30-Day T-Bill Index is generally considered representative of the performance of short-term money market instruments.

Bloomberg Barclays U.S. Government/Credit Index comprises long-term government and investment grade corporate debt securities and is generally considered representative of the performance of the broad U.S. bond market. Unlike convertible bonds, U.S. Treasury bills are backed by the full faith and credit of the U.S. government and offer a guarantee as to the timely repayment of principal and interest.

Morningstar Market Neutral Category represent funds that attempt to eliminate the risks of the market by holding 50% of assets in long positions in stocks and 50% of assets in short positions.

S&P 500 Index is generally considered representative of the U.S. stock market.

S&P 500 Growth Index consists of growth companies in the S&P 500 Index, measured using three factors: sales growth, the ratio of earnings change to price and momentum.

S&P 500 Value Index consists of value companies in the S&P 500 Index, measured using three factors: sales growth, the ratio of earnings change to price and momentum.

MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of 21 developed market countries in North America, Europe, and the Asia/Pacific region. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index.

800919 1217