Using ETFs to Manage Long and Short Exposure

March 20, 2017

This post was written by Calamos Senior Vice President Robert F. Bush, Jr.

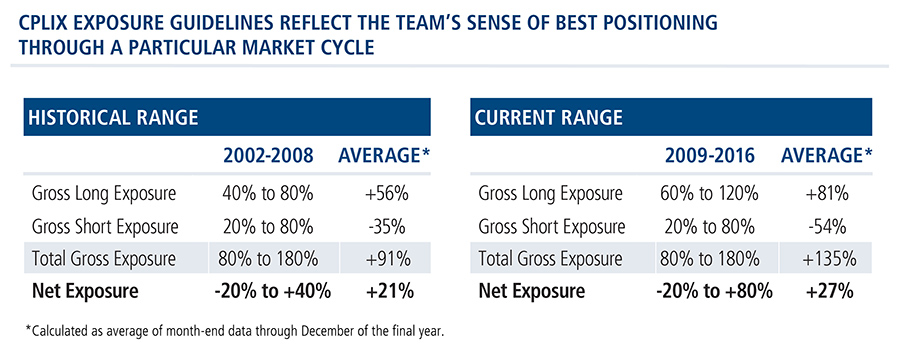

Active management of long and short exposure is a key differentiator between Calamos Phineus Long/Short Fund and its long/short equity competitors. Over the 15 years since the fund’s inception, the fund has achieved its returns with an average net exposure of approximately 27%.

Exposure limits have been in place largely since the fund’s inception in 2002 and are consistent with what has been achieved: keeping up with markets when they’re rising while minimizing drawdowns when markets are falling.

Exposure limits have been in place largely since the fund’s inception in 2002 and are consistent with what has been achieved: keeping up with markets when they’re rising while minimizing drawdowns when markets are falling.

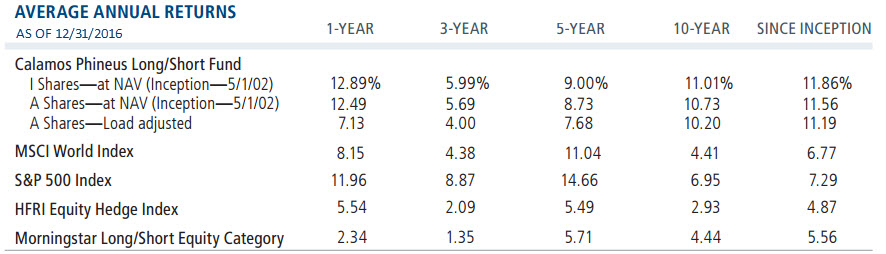

In recent discussions, advisors have marveled at the fact that CPLIX beat the Standard & Poor’s 500 in the last two consecutive years, despite how very different 2015 and 2016 were. In fact, that was a feat accomplished by just 3% of all active large cap managers (source: Morningstar, data as of 12/31/16).

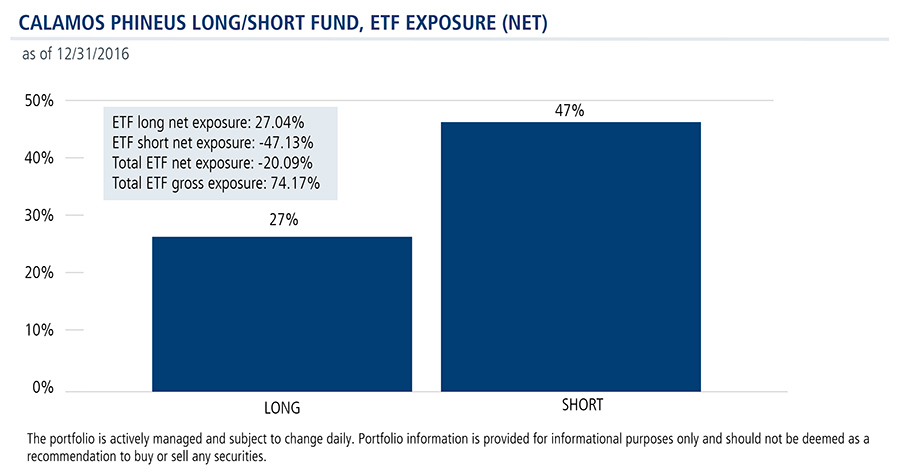

This ability to maintain low market exposure while outperforming the major benchmarks partly reflects an adroit use of exchange-traded funds (ETFs) as risk management tools. Our global long/short team uses ETFs to access long and short exposures to various sector and geographic themes, as well as to hedge downside risk. (Financial advisors, for information on the fund’s current holdings, download the most recent quarter’s portfolio data or talk to a Calamos Investment Consultant.)

ETFs have been an ongoing part of the Calamos Phineus Long/Short Fund’s strategy since the beginning. As the ETF market has developed over the past 15 years, the opportunity has expanded. When the fund increased its long exposure guidelines after 2008 (partly to take advantage of the secular buy opportunity), the use of ETFs became more prevalent on both the long and short side.

Reducing Idiosyncratic Risk

Portfolio management seeks to optimize flexibility and efficiency (e.g., the specific targeting of themes).

Individual securities are used to provide a defined and precise investment theme at the corporate level, while ETFs are baskets of securities and can reduce the idiosyncratic risk of individual companies. We believe that ETFs, when used in tandem with individual securities, can create additional opportunities for return without increasing the overall risk of the portfolio.

For U.S. investments, it is not uncommon for the fund to have positions (long and short) in both companies and ETFs that reflect a common sector bias. Such was the case recently, when the fund was short both a consumer staple ETF and individual consumer staples companies.

ETFs represent a far larger percentage of positions on the short side than on the long side. This enables greater flexibility for entering and exiting short positions tactically, and for shifting overall portfolio exposures.

In these instances, and unlike the general bias of the long side, the team is not typically seeking alpha in these adjustments of short exposure. Instead, the team is using ETFs as a tool to hedge either sector or general market uncertainties.

In these instances, and unlike the general bias of the long side, the team is not typically seeking alpha in these adjustments of short exposure. Instead, the team is using ETFs as a tool to hedge either sector or general market uncertainties.

"Let’s say that we want to build up the net exposure by 10 or 20 points or vice versa,” explains Michael Grant, Senior Co-Portfolio Manager. “The flexibility of ETFs allows us to execute that at will. Otherwise, one might say, ‘I would like to be more short. Please, team, find me some shorts. And the next four weeks are spent trying to do the due diligence and so forth. The risk is that by the time the shorts are identified the opportunity has moved on.’”

Individual stocks are also shorted, but the extent of such is heavily driven by the nature of the financial cycle. More generally, shorting at the company level is viewed as a tactical rather than structural opportunity. This is based on the simple fact that companies are designed and motivated to grow, prosper and succeed, not fail.

ETFs for Non-U.S. Holdings

For non-U.S. investments, the team selectively uses ETFs on the long side of the ledger, especially in emerging markets (EM) where markets can be especially nuanced. For example, the fund has used ETFs to gain select EM exposure in Vietnam, India and Mexico.

In the team’s experience, there are often circumstances when it’s more appropriate to focus on making top-down judgments. ETFs provide a more effective way to capture these top-down themes versus emphasizing individual security convictions. That said, individual security selection is a vital part of the long portfolio. On the short side, the use of individual securities is less common overseas than in the U.S.

While the team’s portfolio guidelines include restrictions on individual equity positions (5% cap on long, 3% cap on short), they don’t apply to ETFs as baskets of securities. As noted earlier, the team uses ETFs to access broad exposure to sector or geographic themes. For example, there was a recent long position in one Europe ETF that stood at approximately 12% of NAV.

Sector and major market hedges (U.S. and global) can be used for short exposures, providing the advantage of tactically adjusting the fund’s overall exposure to general market risk.

Financial advisors, please see the Calamos Phineus Long/Short Fund profile for more information or talk to your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. For the most recent month-end fund performance information visit www.calamos.com.

The performance shown for periods prior to 4/5/16 is the performance of a predecessor investment vehicle (the “Predecessor Fund”). The Predecessor Fund was reorganized into the Fund on 4/5/16, the date upon which the Fund commenced operations. On 10/1/15 the parent company of Calamos Advisors, purchased Phineus Partners LP, the prior investment adviser to the Predecessor Fund (“Phineus”), and Calamos Advisors served as the Predecessor Fund’s investment adviser between 10/1/15 until it was reorganized into the Fund. Phineus and Calamos Advisors managed the Predecessor Fund using investment policies, objectives, guidelines and restrictions that were in all material respects equivalent to those of the Fund. Phineus and Calamos Advisors managed the Predecessor Fund in this manner either directly or indirectly by investing all of the Predecessor Fund’s assets in a master fund structure. The Predecessor Fund performance information has been adjusted to reflect Class A and I shares expenses. However, the Predecessor Fund was not a registered mutual fund and thus was not subject to the same investment and tax restrictions as the Fund. If it had been, the Predecessor Fund’s performance may have been lower.

Alternative investments may not be suitable for all investors, and the risks of alternative investments vary based on the underlying strategies used. Many alternative investments are highly illiquid, meaning that you may not be able to sell your investment when you wish to.

Unmanaged index returns assume reinvestment of any and all distributions and do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in an index.

The S&P 500 Index is a market weighted index and is widely regarded as the standard for measuring U.S. stock market performance.

MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of 21 developed market countries in North America, Europe, and the Asia/Pacific region. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index. The MSCI World Index consists of the following 23 developed market country indexes: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States.

Morningstar U.S. Funds Long/Short Category. Long-short portfolios hold sizable stakes in both long and short positions in equities and related derivatives. Some funds that fall into this category will shift their exposure to long and short positions depending on their macro outlook or the opportunities they uncover through bottom-up research. Some funds may simply hedge long stock positions through exchange-traded funds or derivatives. At least 75% of the assets are in equity securities or derivatives.

ETFs. ETFs, or exchange-traded funds, are marketable securities that track an index, a commodity, bonds, or a basket of assets like an index fund. Unlike mutual funds, ETFs trade like a common stock on a stock exchange. They are priced throughout the day as they are bought and sold.

Net exposure. The difference between a portfolio’s long and short exposure, expressed as a percentage. If a portfolio holds a larger percentage in long positions than in short positions, the portfolio is “net long.” Conversely, a portfolio is “net short” when it has a larger percentage in short positions than in long positions.

Gross exposure. The sum of long exposure and short exposure, gross exposure measures how much of the portfolio’s assets are invested and the amount of leverage in the portfolio.

Diversification and asset allocation do not guarantee against a loss. This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts related to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE