Reclaiming the Investor Psyche: A Roadmap

Michael Grant

Investment success requires taking on risk in exchange for return. Since John P. Calamos, Sr., founded Calamos Investments in 1977, our aim, as active managers, has been not to avoid risk, but to engage it in a sensible and measured manner.

But the years since the Global Financial Crisis (GFC) have skewed how investors think about risk. In the interest of stability, governments and central bankers alike have pursued policies that have remapped investors’ understanding of economic growth, corporate profitability and insolvency risk —and how all of these impact equity returns.

Today we conclude a three-part series written to help financial advisors think about what’s changed, why and what it means for clients’ pursuit of investment returns in the coming years. In the final post in the series, Michael Grant, Calamos Co-CIO, Head of Global Long/Short Strategies and Senior Portfolio Manager of Calamos Phineus Long/Short Fund (CPLIX), looks ahead to how anti-globalization will affect investing opportunities.

Winds of Change: Will Anti-Globalization Lead to a World Less Favorable for Capital?

Also see:

The U.S.: An Island of Economic Dynamism and Non-monetary Reflation

A Global Long/Short View: Why Europe Is In Trouble

Investors at the halfway mark of 2018 are entering the late stage of the post-2008 investment cycle. What comes after late-cycle is “end-cycle” and the proverbial bear market. A bear market, as defined by Michael Grant, is “the discontinuity that marks a shift in the investment setting that disrupts the leadership assets of the cycle in question.”

Grant detects foreboding among investors that the end of the equity cycle is near, for reasons that go beyond the simple longevity of the U.S. expansion.

“One can discern the signs of change,” says Grant. “The most obvious is the fractious wave across the Western world which has transformed democratic expression into event risks for markets.”

In his view, the U.S. 2016 presidential election and the UK’s Brexit referendum can be understood as challenges to the existing orthodoxy: outsiders versus an establishment that became too identified with the costs of globalization.

“The investment world has sensed that politics are becoming less favorable for capital. The conversations about immigration and the movement of capital, the revival of worker wages and trade—all have implications for corporate profit margins, eventually.”

In this context, Grant says the wariness of the financial world for U.S. President Donald Trump is about more than his peculiar style and personality. “Trump is symbolic of the popular revolt against the political and economic orthodoxy of globalization, which has been a disaster for the developed working class,” he says.

Not surprisingly, he adds, this political mood feeds perception of vulnerability. “We estimate about one-quarter of the structural improvement in U.S. corporate profitability of past decades is related to the manufacturing shift to the low-cost emerging world. Politics do matter.”

There is a silver lining, however.

Grant says that China’s “great power mercantilist ambitions” are incompatible in the long run with an open global economy. “To some degree,” he says, “Trump has recognized the climax of the old order, and is creating a new source of profitability to replace the old: a revitalized ‘domestic America.’”

2018: Messages of the Market

One inflection for investors entering 2018 was higher equity volatility. Grant views it as a rehearsal for greater upheavals to come. Q1 was the first setback in equities since 2008 that didn’t benefit the defensive sectors, reflecting what he considers “a real discontinuity.”

“In Q1, investors finally acknowledged trend reversal in the organizing paradigm of the post-2008 era: prolonged U.S. monetary super-stimulus and the secular bull market in bonds.”

The “game of rate suppression and capital subsidization” is now over, he says, helped along by the end of fiscal austerity. This is the end of a long era in which the economic process has been dominated almost exclusively by central bank.

Today’s politics of protest include central banking as part of the order that’s being disrupted. “After all, who elects the central bankers?” Grant asks.

The policy message of Trump is that reflation must continue by non-monetary means. This implies that the extraordinary return on capital will drift lower in coming cycles—“largely to the benefit of labor,” he adds.

“We are already seeing the consumption content of economic growth rise at the expense of investment. In the next downturn, we expect the Western consumer to be a refuge.”

A key turn of Grant’s roadmap is the transition from global-to-domestic, in terms of investment themes and sources of profitability.

“Politics is splintering the global economy into blocs. And the distribution of profit growth in coming years will reflect this,” he says.

The underperformance of emerging equities is another piece of this puzzle, reflecting what Grant says is “oversupply and overcommitment to producer assets” at the expense of consumer-led models of growth. Calling the end of the “globalization boom,” Grant believes the emerging economies will need to compete much harder for international capital.

End-cycle Defined

The capacity of the U.S. economy to progress toward monetary normalization is critical, according to Grant. No other economic bloc has addressed the legacy of the GFC as successfully as the U.S., he argues.

The current investment cycle will not end with deflation, he says. Instead, he says, it will end with the normalization of U.S. interest rates, which “naturally comes down to judging when enough is enough.”

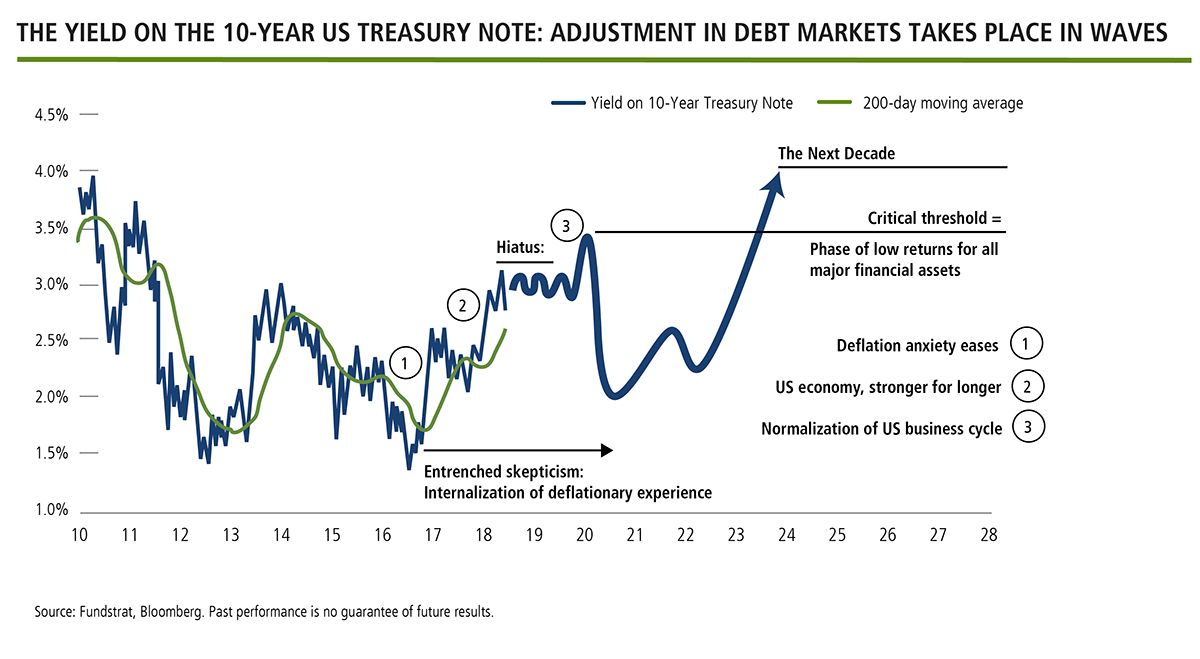

As the 10-year Treasury yield approaches 4%, the leading asset of this investment cycle—U.S. growth stocks—becomes vulnerable, Grant says.

For now, the U.S. economy is enjoying robust cash flows and the consumer backdrop is what Grant considers “strikingly benign.” The late-cycle boost to U.S. corporate profitability, aided by tax reform, is unprecedented. He doesn’t see the rising leverage of corporates as an imminent threat to the expansion.

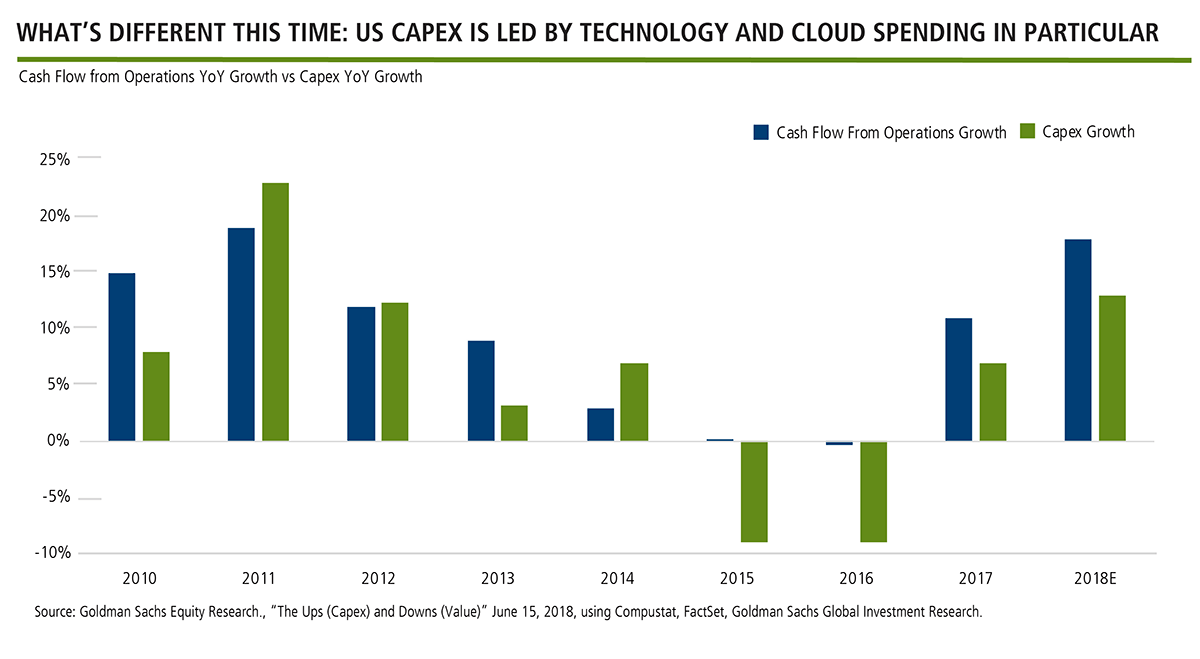

Acknowledging the unusually long expansion, Grant notes something that’s different this time: the cyclical leadership of U.S. technology, whose margins and balance sheets are very different from the traditional industrial sectors.

Given that technology has led, Grant expects technology’s eventual stumble to be “more macro than micro in character.”

“The pervasive theme of the build-out of cloud infrastructure implies that the risk, when it arrives, will be top-down, contagious and self-reinforcing.” The Global Long/Short Team’s “granular analysis of cloud spending implies another large step-up is required in 2019 to support today’s valuations of these companies,” Grant adds.

Eventually, interest rates are the link between “U.S. normalization in all its forms” and the extended credit cycle in the emerging world and China in particular. “China’s problems do not arise amidst deflation and rate suppression,” he says. “They will appear when the developed world confronts a 4% U.S. Treasury yield.”

And, that’s when conditions change again for investors. As Grant says, “A context of rising interest rates alters the conception of a ‘defensive asset’ for a diversified portfolio and for equities in particular.”

Looking ahead, Grant expects the climax of U.S. profitability in 2019-2020 to converge with the end of the credit cycle in the emerging world. “The transmission mechanism is credit, which is why the end-cycle should be understood through the eyes of the debt people.”

From that perspective, the “threshold of disruption” is probably somewhere above 3.5% on the 10-year U.S. Treasury, he opines. “Much above that level and returns for all risk assets fall to very low levels.”

In summary, Grant views 2018 as a more disturbed setting for financial markets:

- Revival of financial volatility is the consequence of fading deflation risk, at least in the U.S. The world economic upswing will extend through 2019, possibly 2020, but globalization becomes splintered into economic blocs.

- In H1 2018, investors acknowledged the transition: the organizing paradigm of the long bull move in risk assets, driven by a declining cost of capital and unprecedented Central Bank intervention, has climaxed.

- The Quantitative Tightening inflection (2016-2020) is a return to a more normal cost of debt, particularly in the U.S. The inflection will be slow and prolonged but is significant because it signals discontinuity for the investment cycle.

- Rising interest rates suggest multiple disturbances and phases of consolidation in bond markets. The constraint is the tension between the U.S. economy, which can absorb policy normalization versus Europe and the emerging world, which have only suppressed insolvency, not resolved it.

- The U.S. is an island of comparative economic dynamism and non-monetary reflation in a still deflationary world. Led by the developed consumer, profitability will increasingly diverge across regions in coming years.

- Both Europe and China will remain the object of suspicion for many in the investment industry. In both there is a perception of structural unsustainability. This foreboding is well founded, but the end of the credit cycle can be delayed amid policies of rate suppression.

- Grant recommends investors favor countries that require less dependence upon Central Bank “monetary alchemy” in all its forms. “Permanent capital subsidization is anti-capitalist and noxious for equity owners,” Grant believes.

- The investment world is no longer the derivative of a single “globalization” narrative. This raises the value of regional asset allocation: investors are advised to avoid those countries with high exposure to the “return-to-mean” of producer assets.

- Grant’s dual imperatives of the next downturn: domestic and defensive. “Domestic versus global may be as relevant to performance outcomes as quality versus risk,” he says. As importantly, cash resumes its traditional role as an active portfolio tool.

The Fading of Passive Management, Another Legacy of 2008

As detailed in this series, the next several years will be characterized by discontinuities. This, according to Grant, argues against buy and hold, which has faded in 2018. He expects the advantage to shift from passive investing to active long/short management in coming years.

For Grant, faith in passive investing is another legacy of 2008.

“Think about the basic difference between passive and active. Passive is money and opinion that follows price. It is momentum by nature and maintains its semblance of control with an analysis of what happened yesterday. It is logic by looking backwards.”

“Active, at its best, anticipates discontinuity. Many fundamental strategies are more passive than active because they do not acknowledge the role of discontinuity in the investment cycle,” he says.

QE pushed investors out of cash in their search for yield, Grant says. But there was a side effect, which he identifies as blurriness over what a “riskless” asset is.

“Some part of the monies in passive products has no vocation in equities,” he says. “Today, passive monies reflect exuberance, which is why we anticipate corrections that become shorter in time but more erratic in price.”

“Even if the bull market continues into 2019,” Grant concludes, “we can imagine a more disturbed setting for equity investors that will require the breadth of skill of active management.”

For the full Reclaiming the Investor Psyche: A Roadmap series, download this PDF.

Advisors, for more information, talk to a Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.