CTSIX at Age 10: Older, Wiser—and On the Lookout for More ‘Big Winners’

April 9, 2021

Have you considered the importance of your selection of a small cap fund? Investment professionals tell us that they count on the contribution from small caps to be one of the main drivers of outperformance within an overall portfolio.

That’s true for a few reasons, says Brandon M. Nelson, Senior Portfolio Manager. “Small caps offer the best opportunity to find big winners,” he says. But, Nelson immediately adds, because “small cap performance tends to exaggerate the decisions of the portfolio manager: Good decisions get disproportionately rewarded by the market, bad decisions get disproportionately punished.”

Nelson recently had the occasion to review some of his team’s past decisions as Calamos Timpani Small Cap Growth Fund (CTSIX) turned 10 years old on March 23.

The recollection starts with 2011 and 2012 investments in Ulta Beauty (ULTA), Transdigm (TDG) and Lendingtree (TREE), all of which are now multibillion dollar companies.

Other holdings were young companies that have gone on to establish themselves as the best of breed in a range of industries:

- Diamondback Energy (FANG), added to the portfolio in 2012

- Old Dominion (ODFL), a “low-profile” trucking company when added in 2014

- Lithia Motors (LAD), a 2012 holding now a prominent auto retailer

- Repligen (RGEN), was owned in 2014 when it was a microcap that barely had analyst coverage. Today it’s a widely held life sciences tools company.

- Square (SQ), owned in 2017 and 2018, now it's a “financial technology staple.”

These four, still in the portfolio, were purchased well below their current market prices:

- Lithia Motors (LAD), first purchased in 2012

- Five9 (FIVN), first purchased in 2016

- Chegg (CHGG), first purchased in 2016

- RingCentral (RNG), first purchased in 2017

In the last 10 years, the fund has owned 34 companies, or three to four per year, that were acquired, and often at substantial premiums.

Each company has its own story, of course, but CTSIX’s investment in them was underpinned by a consistent investment process. To Nelson, it’s the manager with a proven and repeatable process that has the edge in consistently generating relative outperformance.

“Our big winners over the years had two traits in common,” says Nelson. “1. Each had a small, but growing share of a multibillion dollar market and 2. Each was managed by people who knew how to efficiently run a business and, at the same time were strong communicators and effective at managing expectations for the outside world.

“These traits,” he continues, “laid the groundwork to allow these companies to have sustained fundamental momentum—fast growth and underestimated growth. It’s what we looked for 10 years ago, and it’s the cornerstone of what we look for in any investment today. Those big winners are always out there. It’s our job to find them.”

The pursuit is what motivates the CTSIX team, all the while realizing, Nelson says, that “small caps can be ‘squirrelly.’

“They often act like misbehaving children,” according to Nelson. “If you are going to traffic in small caps and seek those big winners, you need a strict sell discipline to prevent those ‘children’ from driving you crazy and ruining your performance.”

“I’ve known that a strict sell discipline is critical my whole 25-year career, but it’s been reinforced several times in the last 10 years.”

What’s Ahead

Small caps were off to a strong start in the first quarter of the year until the rally “took a pause,” as Nelson says, in March. It presented another opportunity for CTSIX to distinguish itself.

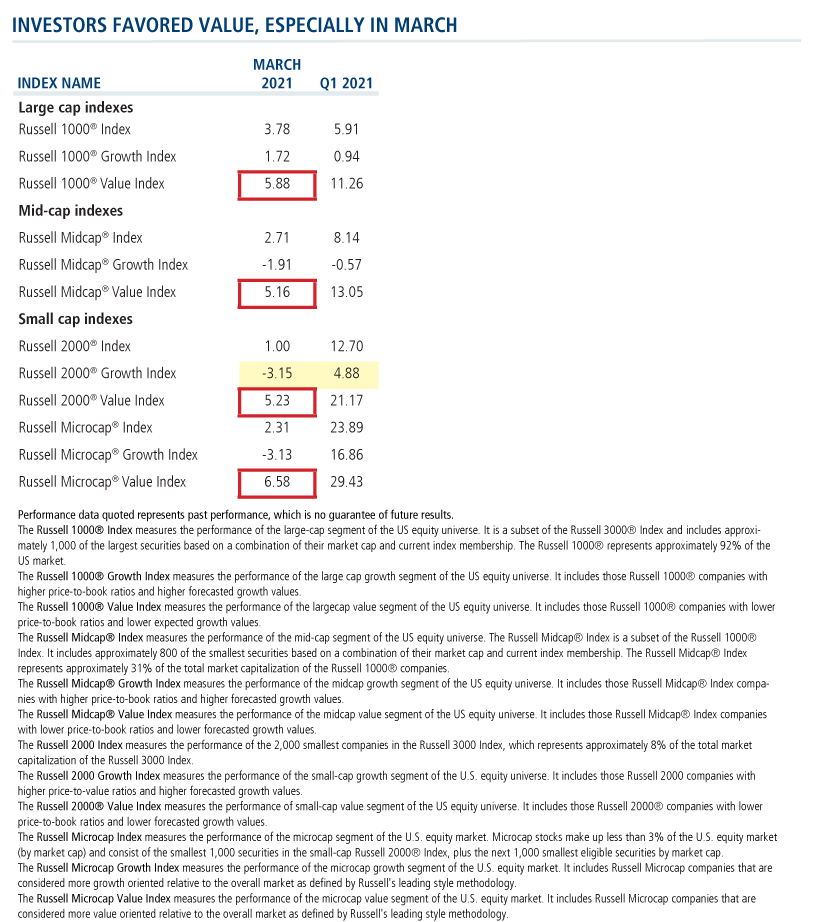

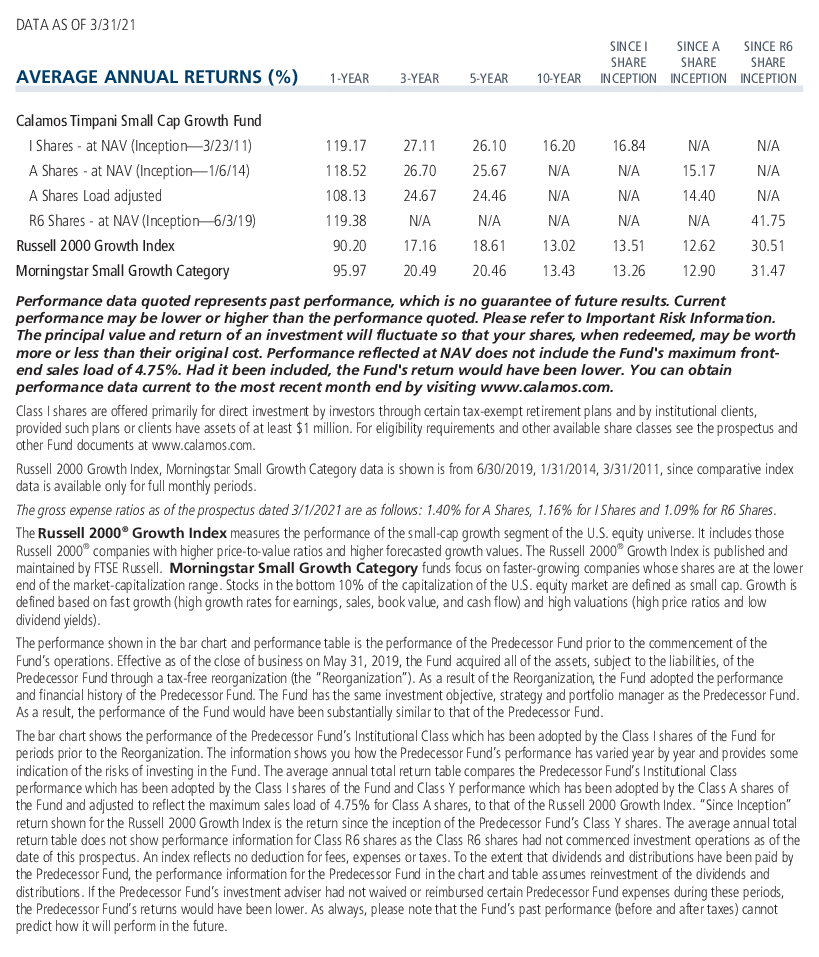

In the quarter, and especially in March, value significantly outperformed growth across all market capitalizations. Despite the fact that CTSIX is consistently “growthier” than its growth benchmarks, the fund outperformed for the quarter. It returned 10.08% or 520 basis points more than the Russell 2000 Growth.

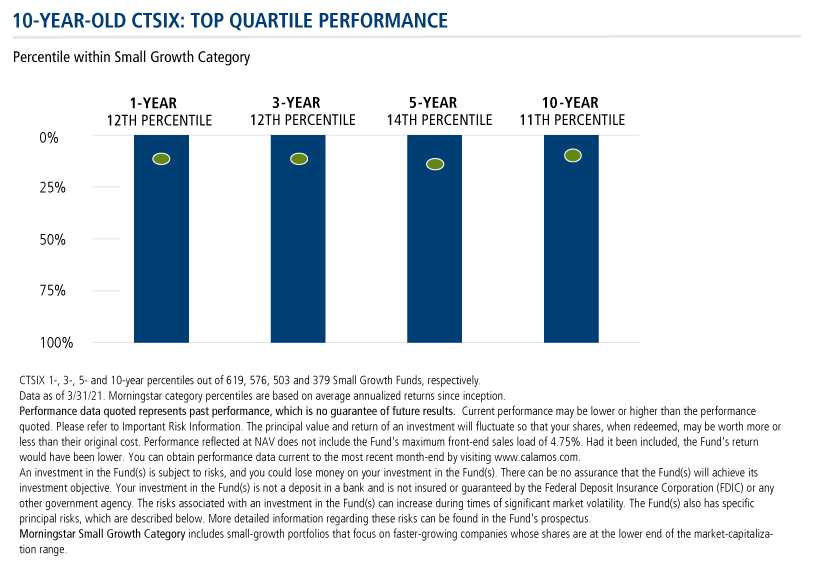

As the fund finishes its first decade in the top quartile of the Morningstar Small Cap Growth category, Nelson is optimistic about what’s ahead. “We’re just seven months into small cap leadership,” he says.

”Recall that history shows the average length of time for small cap leadership is seven years.” (When small caps have led, they’ve led meaningfully and for an extended period of time—an average of 84 months and historically never less than 40 months—read more in this post.)

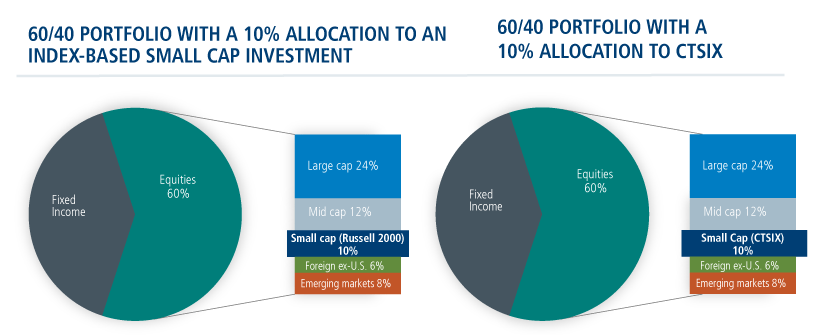

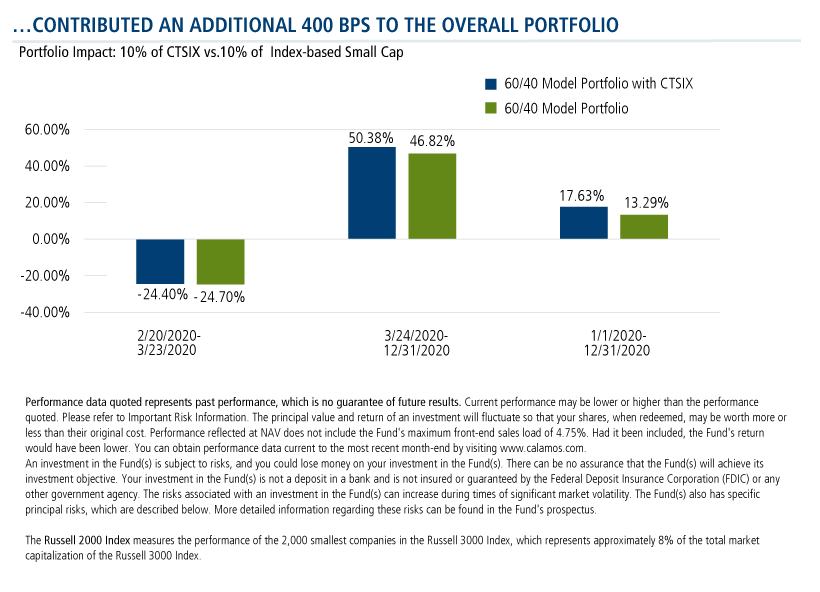

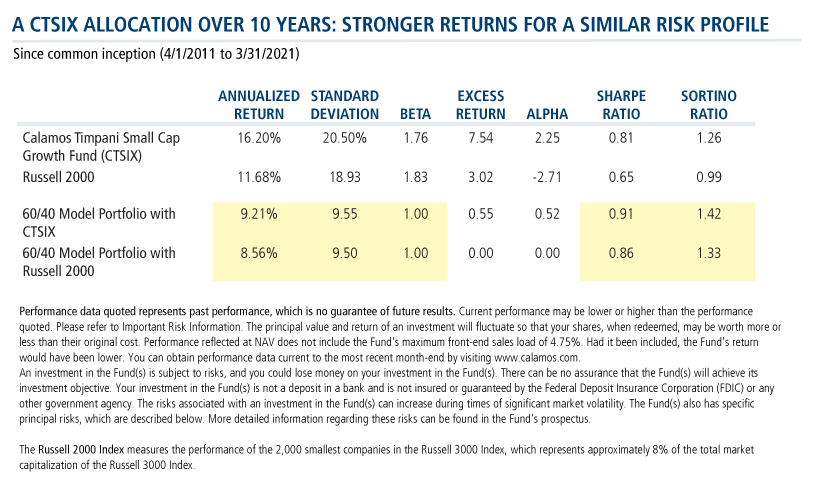

CTSIX’s Impact on a Portfolio Last Year and in the Last Decade

Here’s a look at the difference CTSIX would have made to a portfolio both last year and over the last decade.

The 60/40 portfolio on the left includes a 10% small cap allocation to a fund that tracks the Russell 2000. On the right is a similar portfolio—except that the small cap allocation is to CTSIX.

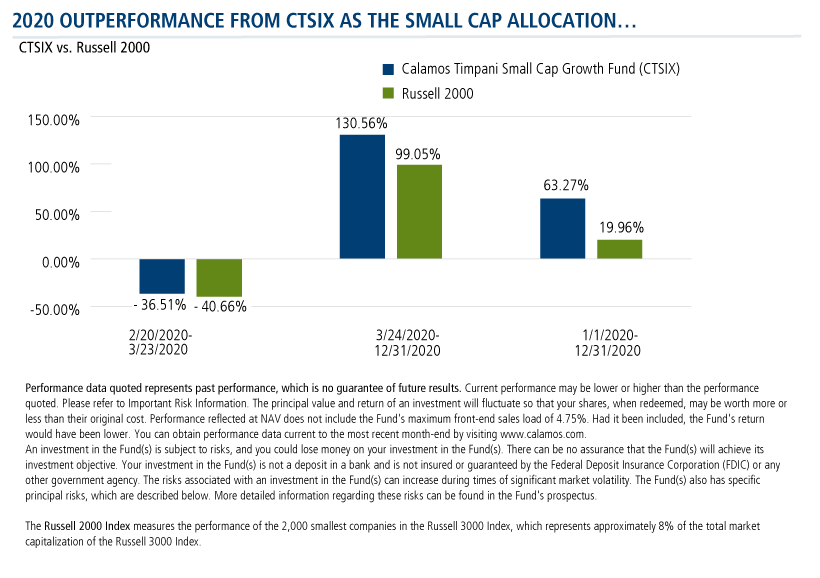

CTSIX far outpaced the index last year, and outperformance from that 10% allocation would have provided a 400 basis point advantage to the overall portfolio.

Investment professionals, for more about CTSIX’s first 10 years or the view ahead, contact your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Top 10 Holdings

As of 3/31/21

| Company | Sector | % |

|---|---|---|

| Lithia Motors, Inc. - Class A | Consumer Discretionary | 4.3% |

| Lpl Financial Holdings, Inc. | Financials | 3.2% |

| Montrose Environmental Group, Inc. | Industrials | 2.5% |

| Kirkland's, Inc. | Consumer Discretionary | 2.2% |

| Allegiant Travel Company | Industrials | 2.2% |

| TopBuild Corp. | Consumer Discretionary | 2.1% |

| Magnite, Inc. | Consumer Discretionary | 2.1% |

| Saia, Inc. | Industrials | 2.1% |

| SiTime Corp. | Information Technology | 2.0% |

| Vericel Corp. | Health Care | 2.0% |

| Total | 24.7% |

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Opinions are subject to change due to changes in the market, economic conditions or changes in the legal and/or regulatory environment and may not necessarily come to pass. This information is provided for informational purposes only and should not be considered tax, legal, or investment advice. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund's prospectus.

The principal risks of investing in the Calamos Timpani Small Cap Growth Fund include: equity securities risk consisting of market prices declining in general, growth stock risk consisting of potential increased volatility due to securities trading at higher multiples, and portfolio selection risk. The Fund invests in small capitalization companies, which are often more volatile and less liquid than investments in larger companies. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

Morningstar RatingsTM are based on risk-adjusted returns for Class I shares and will differ for other share classes. Morningstar ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly historical performance (reflecting sales charges), placing more emphasis on downward variations and rewarding consistent performance. Within each asset class, the top 10%, the next 22.5%, 35%, 22.5%, and the bottom 10% receive 5, 4, 3, 2 or 1 star, respectively. Each fund is rated exclusively against U.S. domiciled funds. The information contained herein is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Source: ©2021 Morningstar, Inc. All rights reserved.

The Russell 1000® Index measures the performance of the large-cap

segment of the US equity universe. It is a subset of the Russell 3000®

Index and includes approximately 1,000 of the largest securities based on

a combination of their market cap and current index membership. The

Russell 1000® represents approximately 92% of the US market. T

The Russell 1000® Growth Index measures the performance of the large cap growth segment of the US equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000® Value Index measures the performance of the largecap value segment of the US equity universe. It includes those Russell 1000® companies with lower price-to-book ratios and lower expected growth values.

The Russell Midcap® Index measures the performance of the mid-cap segment of the US equity universe. The Russell Midcap® Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap® Index represents approximately 31% of the total market capitalization of the Russell 1000® companies.

The Russell Midcap® Growth Index measures the performance of the midcap growth segment of the US equity universe. It includes those Russell Midcap® Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell Midcap® Value Index measures the performance of the midcap value segment of the US equity universe. It includes those Russell Midcap® Index companies with lower price-to-book ratios and lower forecasted growth values.

The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index.

The Russell 2000 Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-value ratios and higher forecasted growth values.

The Russell 2000® Value Index measures the performance of small-cap value segment of the US equity universe. It includes those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values.

The Russell Microcap Index measures the performance of the microcap segment of the U.S. equity market. Microcap stocks make up less than 3% of the U.S. equity market (by market cap) and consist of the smallest 1,000 securities in the small-cap Russell 2000® Index, plus the next 1,000 smallest eligible securities by market cap.

The Russell Microcap Growth Index measures the performance of the microcap growth segment of the U.S. equity market. It includes Russell Microcap companies that are considered more growth oriented relative to the overall market as defined by Russell's leading style methodology.

The Russell Microcap Value Index measures the performance of the microcap value segment of the U.S. equity market. It includes Russell Microcap companies that are considered more value oriented relative to the overall market as defined by Russell's leading style methodology.

Alpha is a historical measure of risk-adjusted performance. Alpha measures how much of a portfolio’s performance is attributable to investment-specific factors versus broad market trends. A positive alpha suggests that the performance of a portfolio was higher than expected given the level of risk in the portfolio. A negative alpha suggests that the performance was less than expected given the risk.

Beta is a common measure of historic volatility, beta measures how much of an investment’s performance is attributable to market-wide factors (such as a rising stock market). An investment that goes up or down as much as a broad market measure has a beta of 1. An investment that captures only half of the market’s movements would have a beta of 0.5.

Sharpe ratio is a calculation that reflects the reward per each unit of risk in a portfolio. The higher the ratio, the better the portfolio's risk-adjusted return is.

Sortino ratio is an excess return over the risk-free rate divided by the downside semi-variance, and so it measures the return to “bad” volatility. (Volatility caused by negative returns is considered bad or undesirable by an investor, while volatility caused by positive returns is good or acceptable.)

Standard deviation is a measure of volatility.

802347 421

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived on April 09, 2022