How CICVX’s Active Management Won the Latest Bout of Equity Volatility

February 13, 2019

It’s no time to be passive when the market is dropping 19% one quarter and then climbing back 8% the next month. Below Joe Wysocki, Calamos Senior Vice President, Co-Portfolio Manager including of Calamos Convertible Fund (CICVX), discusses some of the key decisions he and the team have been making.

“It was the best of times, it was the worst of times.”

I couldn’t help but think of the above quote given the recent market volatility. In two short months the news headlines have gone from “Dow, S&P Post Worst December Since 1932, Nasdaq Has Worst on Record” only to be followed by “The Best January in 30 Years.”

“Is this investing or is it gambling?” my father asked over the holidays.

One of the key advantages of convertibles is how we use them to manage through volatility—striving to capitalize on the opportunity that comes with it. Let’s review how converts handled this latest test that began just before the end of the fourth quarter of last year.

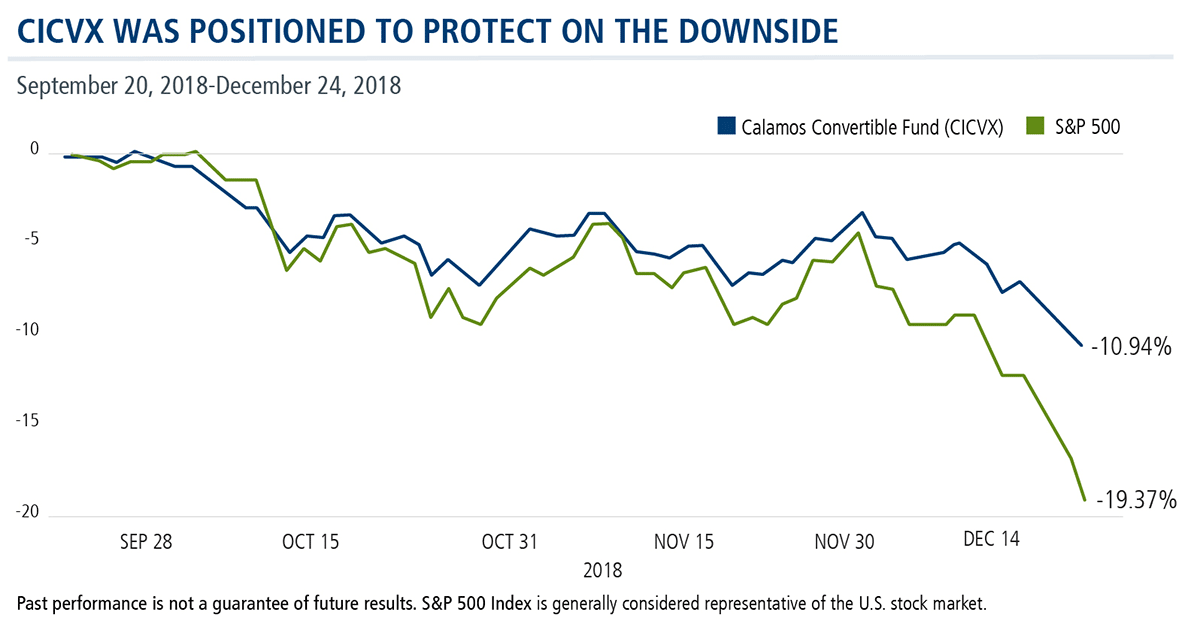

September Positioning Sought Downside Protection

The S&P 500 peaked on September 20, 2018 only to drop almost 20% by December 24, 2018, three months later.

As active managers, we often talk about the importance of monitoring market risks and rebalancing convertibles to assure that the portfolio maintains the optimal risk/reward tradeoff. That’s what we were doing during the summer months of ’18 when the market was hitting new highs (see this post for Wysocki’s comments on managing technology risk in August 2018). Our focus was on monitoring our rising equity sensitivity and credit quality while making sure that the portfolio was appropriately positioned against downside risk.

Changes made by September helped insulate investors in Calamos Convertible Fund (CICVX) for what was to come. CICVX’s halved the decline of the broader equity market.

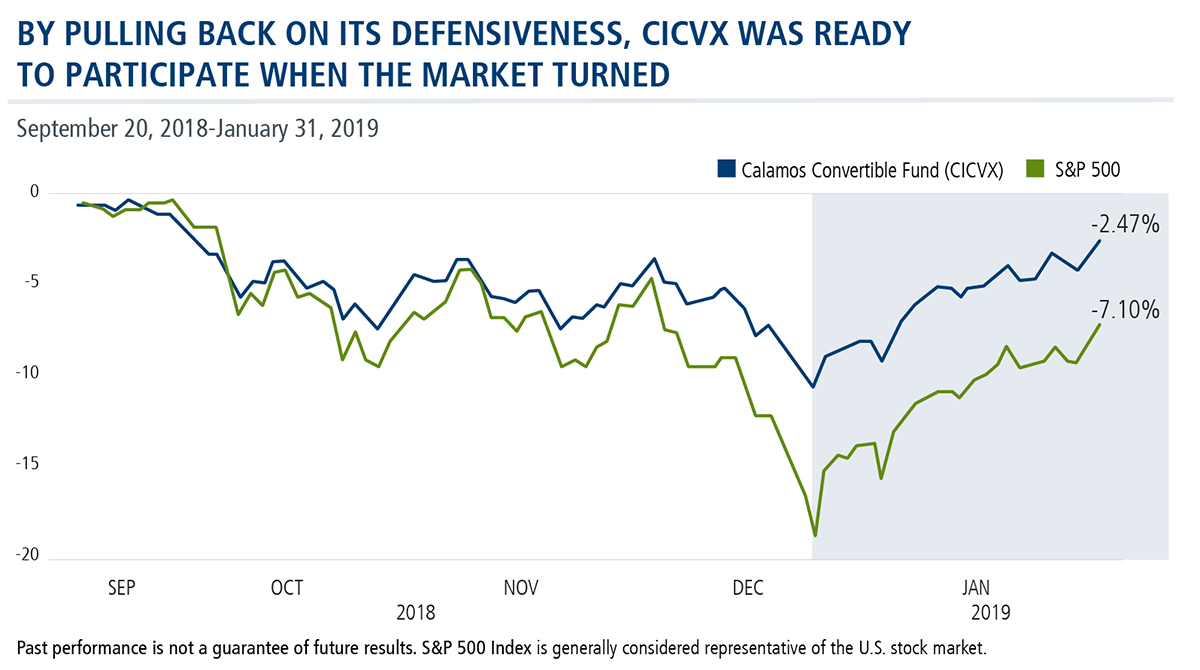

Easing Back on the Defensiveness Ahead of January’s Recovery

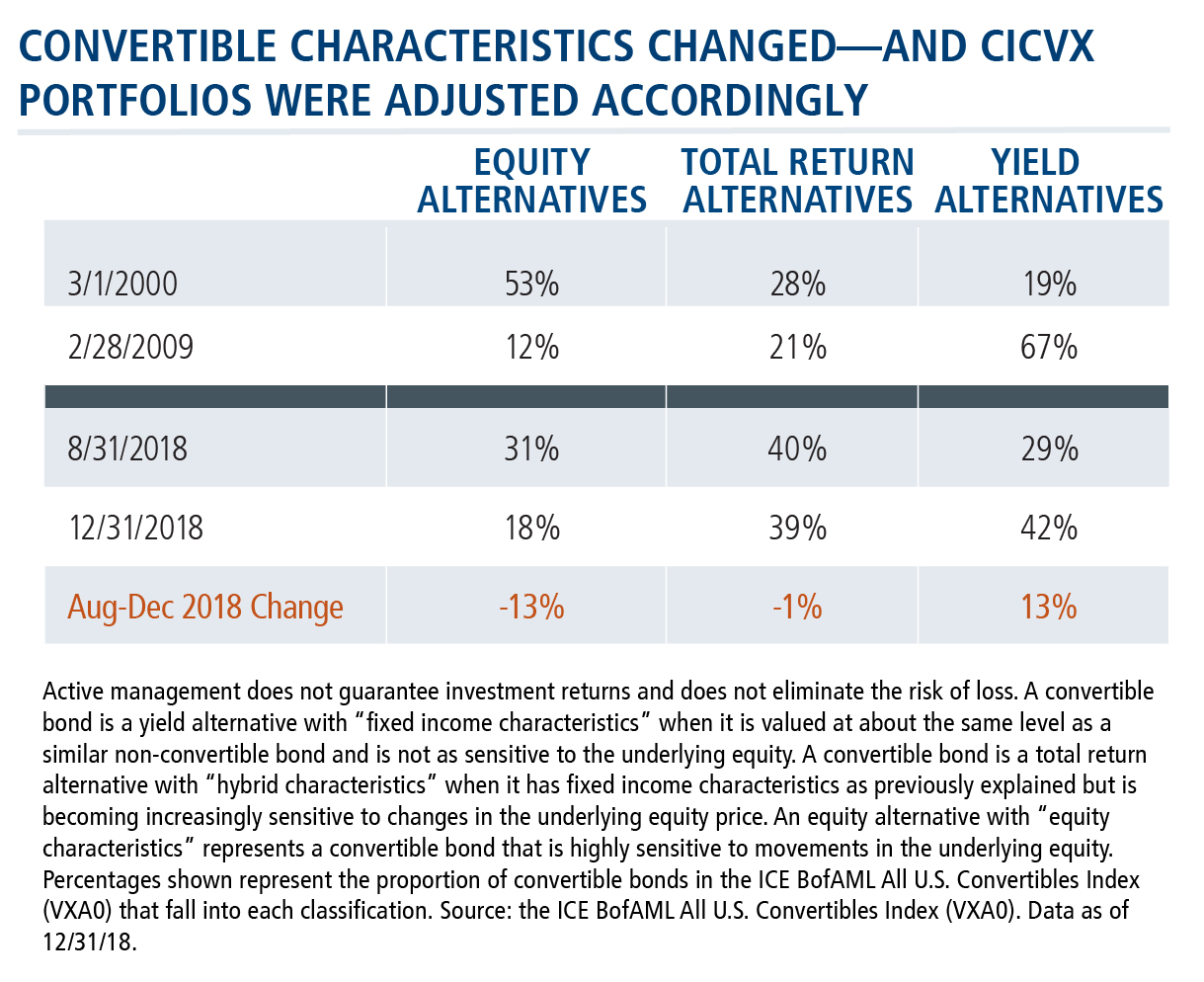

Conditions flipped quickly, though, during the fourth quarter and this time we were facing an alternative scenario. Many convertibles had held up well relative to their underlying equities, but a new risk presented itself: Now the risk was that many convertibles had become more bond-like and potentially too defensive to generate a reasonable total return going forward.

One way to view this is by breaking down the convertible market as represented by the ICE BofAML All U.S. Convertibles Index (VXA0) into buckets based on the convertible characteristics.

As you can see, our sweet spot—the “total return” portion that provides the optimal combination of upside participation as well as downside protection—was still significant. But note how Yield Alternatives, the portion of the market that’s the most bond-like and has the least equity sensitivity, went from the least at 8/31/18 to the largest on 12/31/18. While still below the ~67% it represented during the depths of the financial crisis, this segment has rarely been above 40% over the past decade.

The volatility provided an opportunity for us to rebalance again. This time we were looking to exit more defensive or busted positions in favor of adding back more balanced convertibles at attractive prices that would provide more compelling total return profiles going forward.

Our ability to manage these tradeoffs and add to more favored names proved to be beneficial as the equity market subsequently rebounded 15% through January. The S&P posted a remarkable turnaround in just 38 days, but investors were still 7% below the September high.

CICVX was a mere 2.5% off September’s high—a much better outcome than most investors would have envisioned if they were only paying attention to the headlines during the volatility. The fund’s performance during this stretch, however, exemplifies what financial advisors look for when including CICVX in clients’ portfolios.

Convertibles Can Provide What Market Timing Can’t

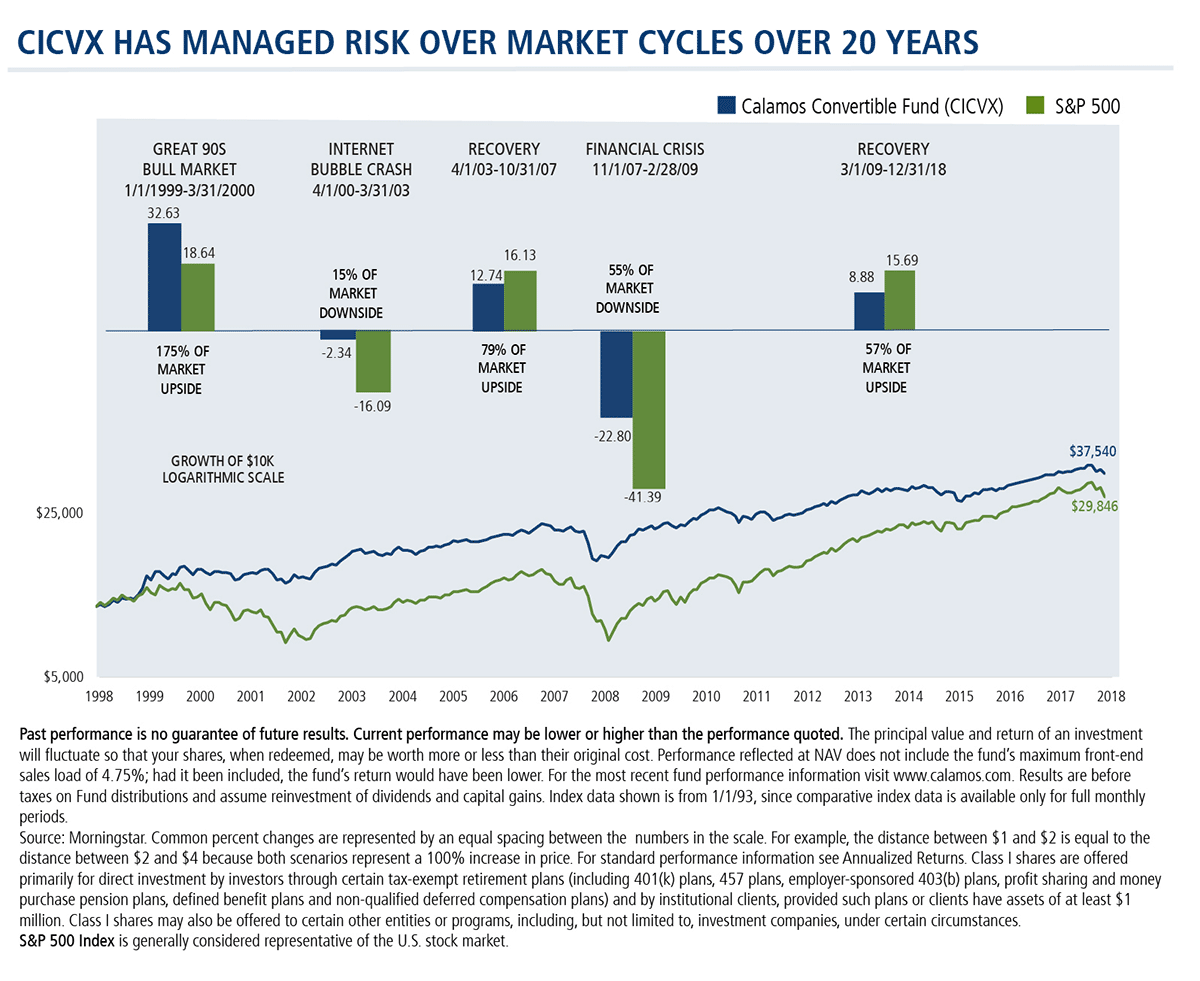

In our experience in managing through many of these market cycles, our team has learned that one of the keys to success is to participate on the upside, but always have an eye toward protecting the downside. The larger the drawdown, the more is required to get back to break even, as we’ve discussed before (see Could Calamos Convertible Fund Help Reduce Your Retirees’ Worries?).

Convertible bonds have both equity and fixed income attributes, and this hybrid nature has historically proven to be a valuable tool in periods of volatility. Converts are able to participate in equity market upside while continuing to manage the downside. This is far preferred to trying to time market entrances and exits.

The two markets provide us with a fresh illustration of the case for including convertibles as a core part of any asset allocation. While we may not experience the same level of volatility in such a short period anytime soon, volatility is an ever-present risk—and opportunity.

Click here to view CICVX's standardized performance.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS (agency fixed rate and hybrid ARM pass-throughs), ABS, and CMBS sectors.

The ICE BofAML All U.S. Convertibles Index (VXA0) comprises approximately 700 issues of only convertible bonds and preferreds of all qualities. Source ICE Data Indices, LLC, used with permission. ICE permits use of the ICE BofAML indices and related data on an ‘as is’ basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofAML Indices or data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing and does not sponsor, endorse or recommend Calamos Advisors LLC or any of its products or services.

The S&P 500 Index is a market-value weighted index consisting of 500 stocks chosen for market size, liquidity, and industry group representation. It is widely regarded as the standard for measuring U.S. stock-market performance.

The Value Line Convertible Index is an equally weighted index of the largest convertibles. Unmanaged index returns assume reinvestment of any and all distributions and, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index.

Morningstar Convertibles Category funds are designed to offer some of the capital appreciation potential of stock portfolios while also supplying some of the safety and yield of bond portfolios. To do so, they focus on convertible bonds and convertible preferred stocks. Convertible bonds allow investors to convert the bonds into shares of stock, usually at a preset price. These securities thus act a bit like stocks and a bit like bonds.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Convertible Fund include: convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk consisting of fluctuations inconsistent with a convertible security and the risk of components expiring worthless, foreign securities risk, equity securities risk, interest rate risk, credit risk, high yield risk, portfolio selection risk and liquidity risk. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

801479 2/19

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end performance information, please CLICK HERE. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower. For the most recent month-end fund performance information visit www.calamos.com.

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived on February 13, 2020