When Volatility Attacked, CMNIX and CIHEX Were Ready

January 24, 2019

As of March 1, Calamos Hedged Equity Income Fund’s name has been changed to Calamos Hedged Equity Fund.

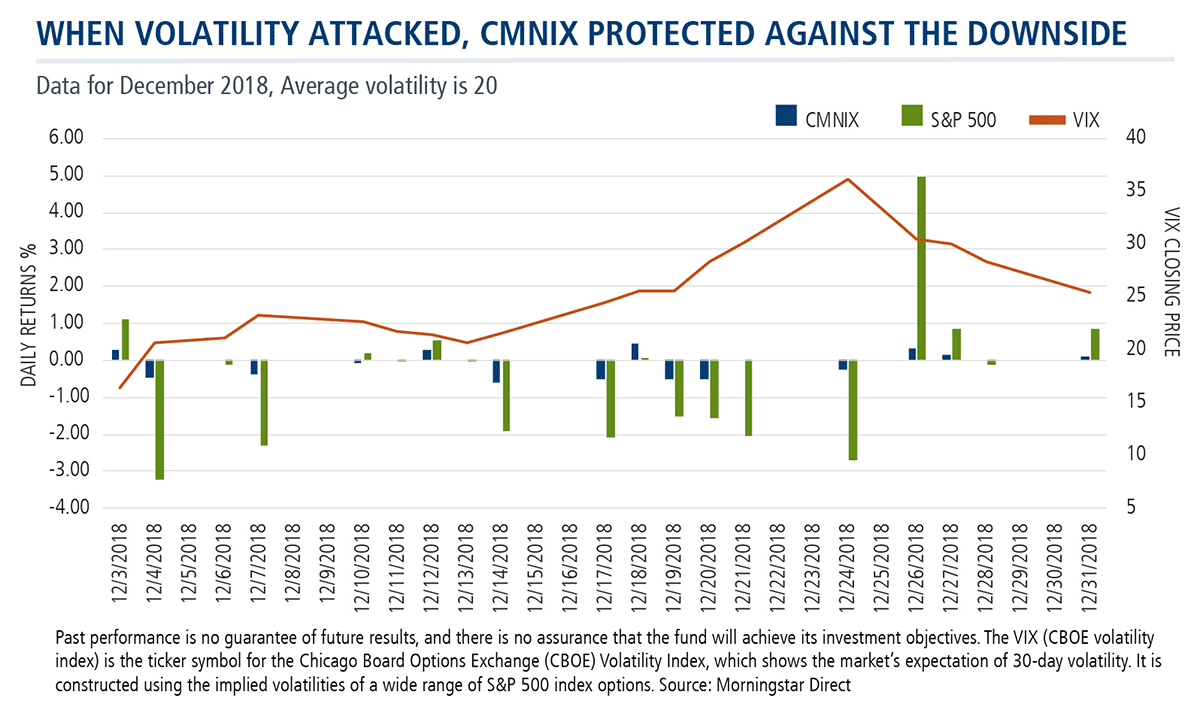

December’s market volatility was what most investors would expect to see only in a stress test scenario. The VIX jumped from 16 to 36 and back down to 25 all in the span of one month. We talked to Dave O’Donohue, Senior Vice President and Co-Portfolio Manager, about how he and the Calamos Market Neutral Income Fund (CMNIX) and Calamos Hedged Equity Income Fund (CIHEX) team view volatility and how they reacted to the big swings in volatility during December.

Q. Dave, would you step us through what you saw in December?

A. It was a wild month, but we tend to get excited when we have increases in volatility because it can present opportunity for the funds. When there’s too much volatility, though, we need to shift our focus from the opportunity to the risk.

As part of our standard risk management practices, we continually stress-test our portfolios—we run “shocks” for different extreme scenarios. That’s what we had in December: a real-life example of a downside stress test.

In one month’s time the S&P 500 dropped 15%, the VIX more than doubled, and there was a 200-basis point widening of credit spreads from their October tights.

Those are the ingredients for a classic, but extreme, downside shock scenario. Any one of those components is a stressor that can expose weaknesses in a process and in a portfolio, and we saw all three at the same time.

Q. Do extreme shocks present a challenge for your active approach?

A. It’s a challenge.

We believe one of the strengths to our process is our dynamic approach. Ideally, we can take advantage of market movements to monetize and readjust our hedges. In falling markets we can cover calls we have written or roll down/readjust our puts, and in rising markets we can add puts or roll up/readjust our strikes.

This becomes challenging, though, with an aggressive shock like what we saw in December. While we like to be opportunistic, it’s always important as a portfolio manager to stay true to your approach and your risk profile. Everyone likes higher returns, but the core investor in the Market Neutral Income Fund is risk-averse. In fact, many people rely on it as an alternative to traditional or core fixed income.

So, while we are looking to be opportunistic, at the end of the day we need to make sure that first and foremost we focus on preservation of capital. Our goal is to capitalize on the volatility, we just need to make sure we do it responsibly with one eye always focused on the downside tail.

It’s a little different for our Hedged Equity Fund. The core investor, while defensive, is still looking for equity-like returns. In this strategy, we are trying to outperform in down markets but we can be more opportunistic when it comes to monetizing our puts and setting ourselves up for a potential bounce (and see CIHEX Beats Back 3 Equity Market Drawdowns to Finish 2018 Positive).

Q. All things considered, are you satisfied with how the funds held up during the “shock”?

A. Yes. For Market Neutral Income, we prefer to be closer to flat in down periods. But realistically, flat would have been difficult to achieve in December, given that there is some equity sensitivity in the hedged equity sleeve.

We like that sensitivity—we think it blends well with our convertible arbitrage strategy and provides us the opportunity to capture some extra return during rising equity markets. Our challenge is to make sure that our equity sensitivity is non-linear—by that I mean that our response to a decline in the equity market is not proportional to that decline.

We like the upside but we don’t want too much downside equity participation. That’s why we layer in puts and put spreads and have an opportunistic—as opposed to formulaic—approach.

In a market move like what we saw in December we know there will be some participation in the initial sell-off. But we can sleep easier at night knowing that the fund’s additional put protection will kick in and our participation will decrease should the equity market fall further—and before we get to levels we aren’t comfortable with.

Our Hedged Equity strategy is a similar approach. But since it’s positioned as a defensive equity fund, it can be a bit more opportunistic and rebalance quicker.

Q. Dave, what should financial advisors take away from the funds’ performance vis-à-vis other market neutral or options-based funds?

A. Some of the funds’ peers, and occasionally the categories as a whole, can tend to be simply long leaning or short leaning. While they may perform well in one-directional markets, they don’t provide the opportunities to reset their market exposures like we attempt to. Rather than focus solely on long or short leaning, we try to position our funds to be both, and the value of a dynamic approach shows in a year like 2018.

We’d obviously like better absolute performance out of the equity and fixed income markets, with equity markets negative and core fixed income flat, but the funds’ positive calendar-year returns for 2018 show what our opportunistic approach can provide.

Advisors, for more information, contact your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Calamos is the fourth largest alternatives manager by assets under management and #1 in alternative flows for 2018 (Morningstar data, 12/31/18).

Click here to view CMNIX's standardized performance.

Click here to view CIHEX's standardized performance.

Click here to view CPLIX's standardized performance.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Alternative investments may not be suitable for all investors.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in Calamos Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

Covered Call Writing: As the writer of a covered call option on a security, the fund foregoes, during the option’s life, the opportunity to profit from increases in the market value of the security, covering the call option above the sum of the premium and the exercise price of the call.

Convertible Securities Risk: The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors also may have an effect on the convertible security’s investment value.

Convertible Arbitrage Risk: If the market price of the underlying common stock increases above the conversion price on a convertible security, the price of the convertible security will increase. The fund’s increased liability on any outstanding short position would, in whole or in part, reduce this gain.

The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, options risk, and leverage risk.

The principal risks of investing in the Calamos Hedged Equity Income Fund include: covered call writing risk, options risk, equity securities risk, correlation risk, mid-sized company risk, interest rate risk, credit risk, liquidity risk, portfolio turnover risk, portfolio selection risk, foreign securities risk, American depository receipts, and REITs risks.

S&P 500 Index is generally considered representative of the U.S. stock market.

MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of 21 developed market countries in North America, Europe, and the Asia/Pacific region.

Unmanaged index returns assume reinvestment of any and all distributions and do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index.

Citigroup 30-Day T-Bill Index is generally considered representative of the performance of short-term money market instruments.

Bloomberg Barclays U.S. Government/Credit Index comprises long-term government and investment grade corporate debt securities and is generally considered representative of the performance of the broad U.S. bond market. Unlike convertible bonds, U.S. Treasury bills are backed by the full faith and credit of the U.S. government and offer a guarantee as to the timely repayment of principal and interest.

Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

Morningstar Market Neutral Category represent funds that attempt to eliminate the risks of the market by holding 50% of assets in long positions in stocks and 50% of assets in short positions.

Morningstar Long/Short Equity Category funds take a net long stock position, meaning the total market risk from the long positions is not completely offset by the market risk of the short positions. Total return, therefore, is a combination of the return from market exposure (beta) plus any value-added from stock-picking or market-timing (alpha).

Morningstar Options-based Category funds use options as a significant and consistent part of their overall investment strategy. Trading options may introduce asymmetric return properties to an equity investment portfolio. These investments may use a variety of strategies, including but not limited to: put writing, covered call writing, option spread, options-based hedged equity, and collar strategies. In addition, option writing funds may seek to generate a portion of their returns, either indirectly or directly, from the volatility risk premium associated with options trading strategies.

Calamos Market Neutral Income Fund’s load-waived Class I shares received 4 stars for 3 years, 4 stars for 5 years, and 5 stars for 10 years out of 122, 98 and 31 Market Neutral funds, respectively, for the period ended 12/31/18.

Calamos Hedged Equity Income Fund’s load-waived Class I shares received 5 stars for 3 years out of 94 Options-based funds for the period ended 12/31/18.

Morningstar Ratings™ are based on risk-adjusted returns and are through 12/31/18 for Class I shares and will differ for other share classes. Morningstar ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly historical performance (reflecting sales charges), placing more emphasis on downward variations and rewarding consistent performance. Within each asset class, the top 10%, the next 22.5%, 35%, 22.5%, and the bottom 10% receive 5, 4, 3, 2 or 1 star, respectively. Each fund is rated exclusively against U.S. domiciled funds. The information contained herein is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Source: ©2019 Morningstar, Inc.

801451 1/19

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end performance information, please CLICK HERE. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower. For the most recent month-end fund performance information visit www.calamos.com.

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived on January 24, 2020