Decumulation and Volatility: Advisors’ Focus as Clients Approach Retirement

April 18, 2017

Volatility can be the investor’s friend in the accumulation phase, and drawdowns can be the price of long-term appreciation. In the withdrawal phase, however, large drawdowns can permanently impair the portfolio’s ability to generate income as shares are liquidated to deliver that income are removed.

Reducing portfolio variance and drawdowns can be more critical than ever in the withdrawal phase even while your clients need growth potential from equities.

And so it’s in the decumulation stage where consultant Keith Van Etten of Van Etten Consulting, Inc. sees financial advisors increasingly turn to liquid alternative mutual funds.

“After having focused on the accumulation stage for so many years, advisors are realizing that decumulation involves a set of different considerations—sequencing of returns and managing drawdowns just to name two. They’re turning to alternatives to better manage the risks of running out of money in retirement,” says Van Etten.

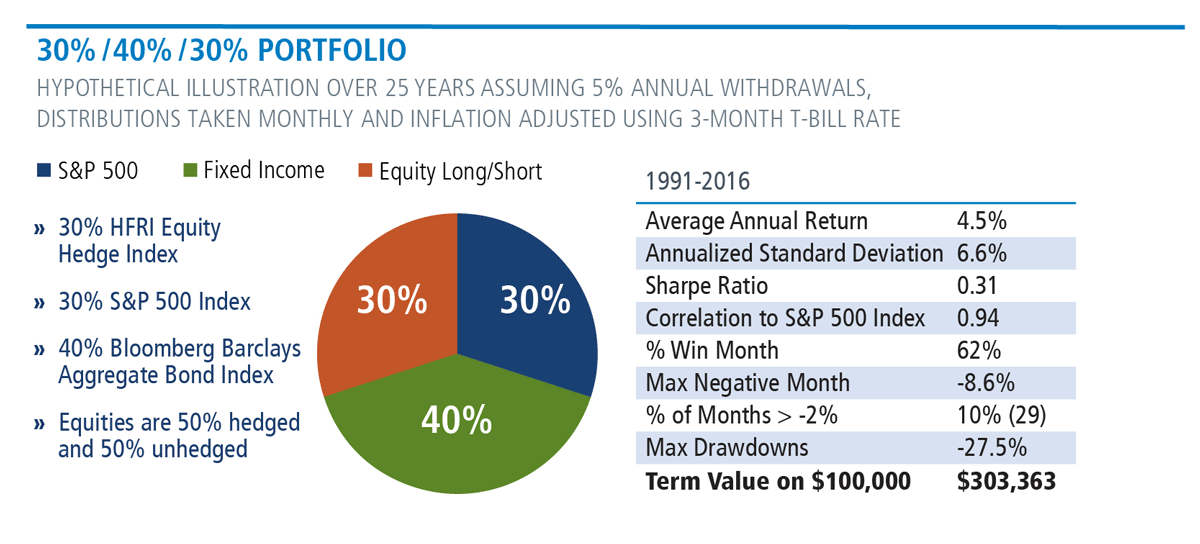

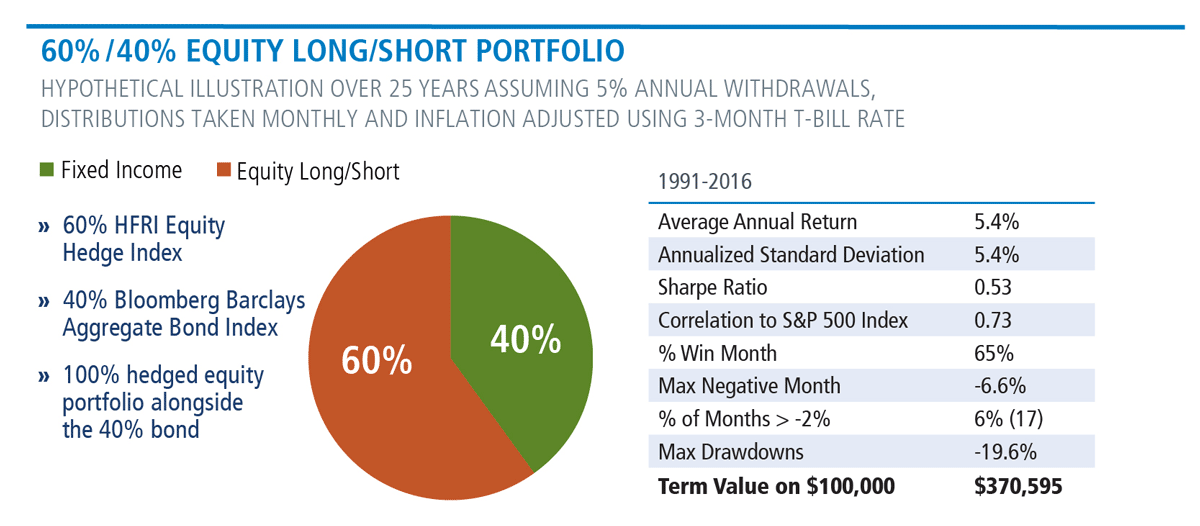

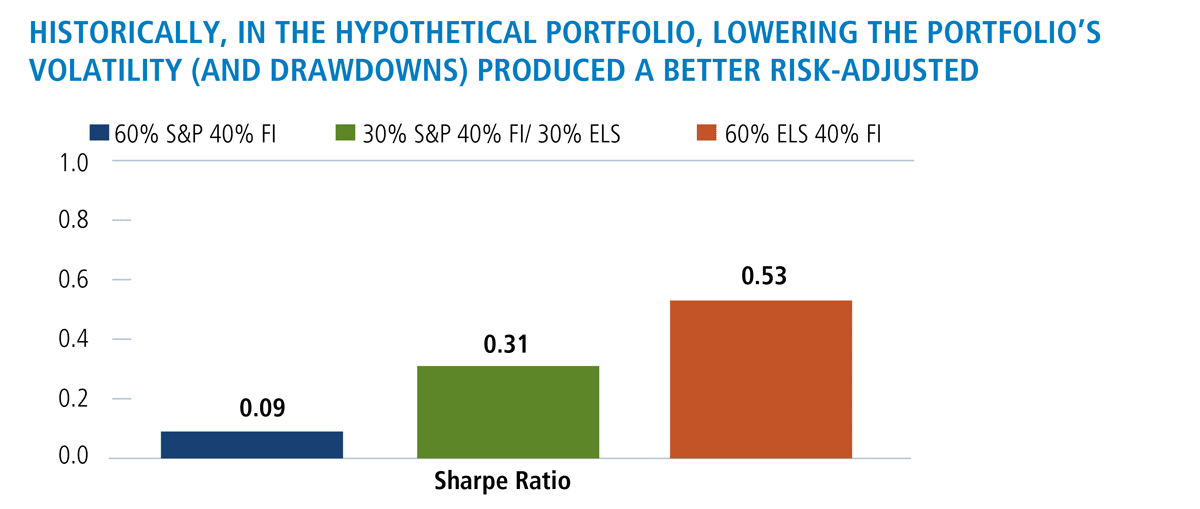

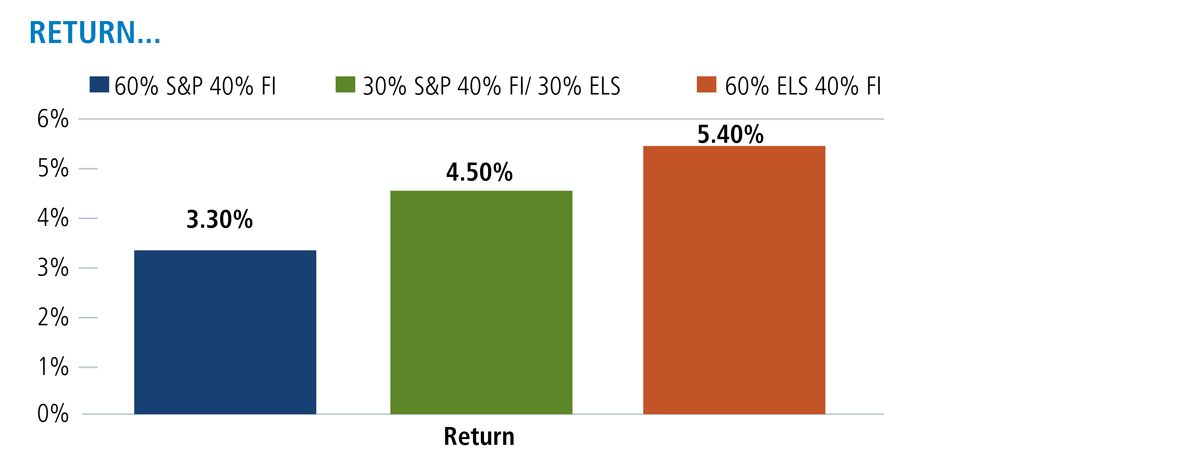

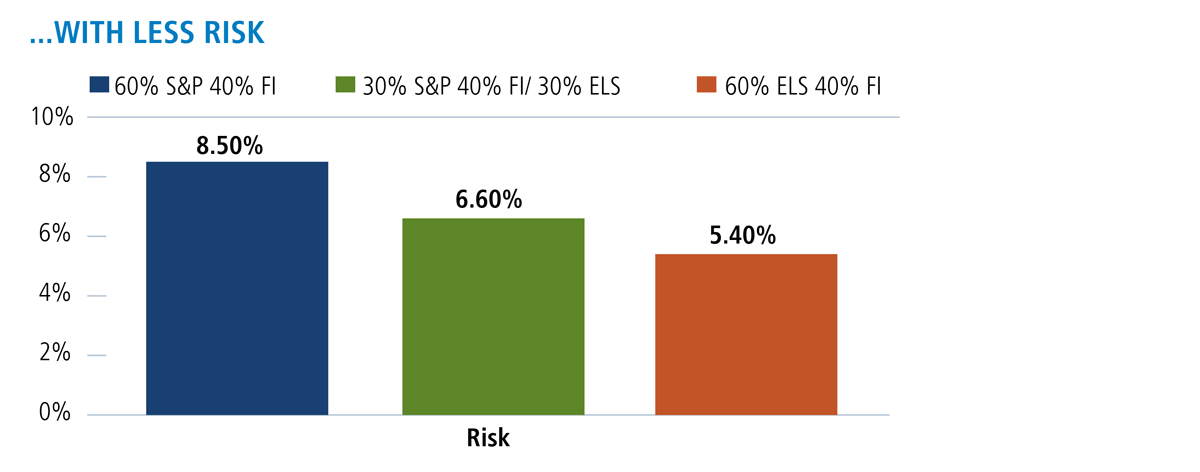

The following hypothetical illustration shows how the adjustment of a traditional 60%/40% portfolio to include an equity long/short strategy may play a role in a distribution portfolio. Higher risk-adjusted returns versus the market over a full market cycle can mitigate the market’s more extreme returns (both high and low). And, lower overall volatility in an equity portfolio may reduce the prospect of emotional reactions during market pullbacks.

All three of these sample portfolios were successful at sustaining income over the full period and all had a positive ending term value.

However, reducing the portfolio’s volatility, including drawdowns, had a significant impact during the withdrawal phase. The risk metrics improved proportionately and the Sharpe ratio also improved.

Financial advisors, for more information about using a long/short equity strategy to minimize drawdowns in the distribution stage, talk to your Calamos Investment Consultant about Calamos Phineus Long/Short Fund. He or she can be reached at 888-571-2567 or caminfo@calamos.com.

For more on Calamos’ approach to volatility, see our just-updated Volatility Opportunity Guide.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee against a loss. This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. Alternative investments may not be suitable for all investors. This information is provided for informational purposes only and nothing presented herein is or is intended to constitute investment advice, and no investment decision should be made based on any information provided herein.

Some of the risks associated with investing in alternatives may include hedging risk, derivative risk, short sale risk, interest rate risk, credit risk, liquidity risk, non-U.S. government obligation risk and portfolio selection risk.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

Indexes are unmanaged, do not reflect fees or expenses and are not available for direct investment.

The S&P 500 Index is considered generally representative of the U.S. stock market.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years. Formerly known as the Lehman Brothers Aggregate Bond Index.

The HFRI Equity Hedge Index consists of funds where portfolio managers maintain long and short positions in primarily equity and derivative securities.

Source: Data from Morningstar, Federal Reserve and Hedge Fund Research, Inc. (www.hedgefundresearch.com). Equity Long-Short index is based on the HFRI Equity Hedge Index.

The 60/40 combination is based on the S&P 500 Index and Bloomberg Barclays U.S. Aggregate Bond Index.

The 30/40/30 Portfolio is based on the S&P 500 Index, Bloomberg Barclays U.S. Aggregate Bond Index and the HFRI Equity Hedge Index.

The 40/60 Portfolio is based on the Bloomberg Barclays U.S. Aggregate Bond Index and the HFRI Equity Hedge Index.

*Annual withdrawals began at 5% and are increased each month by the T-Bill rate. Withdrawals are taken proportional each month from each investment based on initial allocation.

©2017 Van Etten Consulting, Inc. All Rights Reserved.

Correlation: Correlation is a statistical relationship between two variables. A positive correlation occurs when two variables move in tandem–one variable increases as the other increases and vice versa. Negative correlation occurs when they move in opposite directions–one variable increases as the other decreases and vice versa.

Portfolio Variance: The measurement of how the actual returns of a group of securities making up a portfolio fluctuate. Portfolio variance looks at the standard deviation of each security in the portfolio as well as how those individual securities correlate with the others in the portfolio.

Sharpe Ratio: Sharpe ratio is a calculation that reflects the reward per each unit of risk in a portfolio. The higher the ratio, the better the portfolio’s risk-adjusted return is.

Standard Deviation: Standard deviation is a measure of volatility.

Portfolios are managed according to their respective strategies which may differ significantly in terms of security holdings, industry weightings, and asset allocation from those of the benchmark(s). Portfolio performance, characteristics and volatility may differ from the benchmark(s) shown. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

800102 0317