For the Fence Straddlers: Making Sense of Valuations, Volatility and Interest Rates

August 8, 2017

Here’s what was happening as hundreds of financial advisors signed in for last week’s webcast “Designing an Alternative Asset Allocation: Our Best Ideas for H2 2017:” (Available now to listen on-demand.)

- The Dow Jones Industrial Average was a day away from crossing the 22,000 mark.

- The Standard & Poor’s 500 was up almost 12% for the year (11.59% as of July 31).

- The best earning season in seven years for positive surprises was drawing to an end, with 77% of reporting S&P 500 firms beating estimates.

- U.S. stock funds marked their seventh straight week of redemptions.

- Former Federal Reserve Chairman Alan Greenspan warned of a coming bubble not in stock prices but in bond prices, one he said is not being discounted in the marketplace.

- Market volatility was low—troublingly so for some commentators who reported, “since 1990 when the VIX was first created, the index has closed below 10 on only 16 days; seven of those days have been since May 1, 2017.”

These can be ambiguous times, or as one Calamos investment consultant puts it, “The Fear of Missing Out (FOMO) on the market is being offset by clients’ Fear of Jumping In (FOJI).”

Add Value That the Robot Can’t

It’s this kind of environment—when advisors are seeking fresh ideas to help advance clients’ investment objectives, regardless—that is conducive to a discussion about a few alternatives.

“We’re asking you to look beyond the traditional 60% equity/40% fixed income allocation to a concept that potentially enhances that 60/40,” said Calamos President and Head of Global Distribution Robert Behan by way of introducing the webcast on the effect of using an equity and income alternative.

“It’s forward-thinking. We’ve had a lot of positive feedback from advisors about it and the results. And perhaps your challenge may be also to challenge the 60/40 in a way that the robot can’t,” said Behan.

For those who are worried about the end of the three-decade bull market in bonds, Calamos Market Neutral Income Fund (CMNIX) is a time-tested fixed income replacement option. For those concerned about the late nature of the equity bull market, Calamos Phineus Long/Short Fund (CPLIX) is a proven equity replacement option.

Combining the two (as was done in a detailed blog post and discussed during the webcast) contributed to an investment portfolio by producing a better return with less volatility. We call it the Half Caff because it provides jump with less jolt.

Last week’s session was a full 60 minutes, with outlook and comments from portfolio managers Michael Grant (CPLIX) and Eli Pars (CMNIX) followed by an attendee Q&A moderated by Behan.

In this post we’ll report on Michael Grant’s global outlook for equities, including his responses to questions posed by advisor attendees. We’ll share Eli Pars’ current perspectives on volatility in a subsequent post.

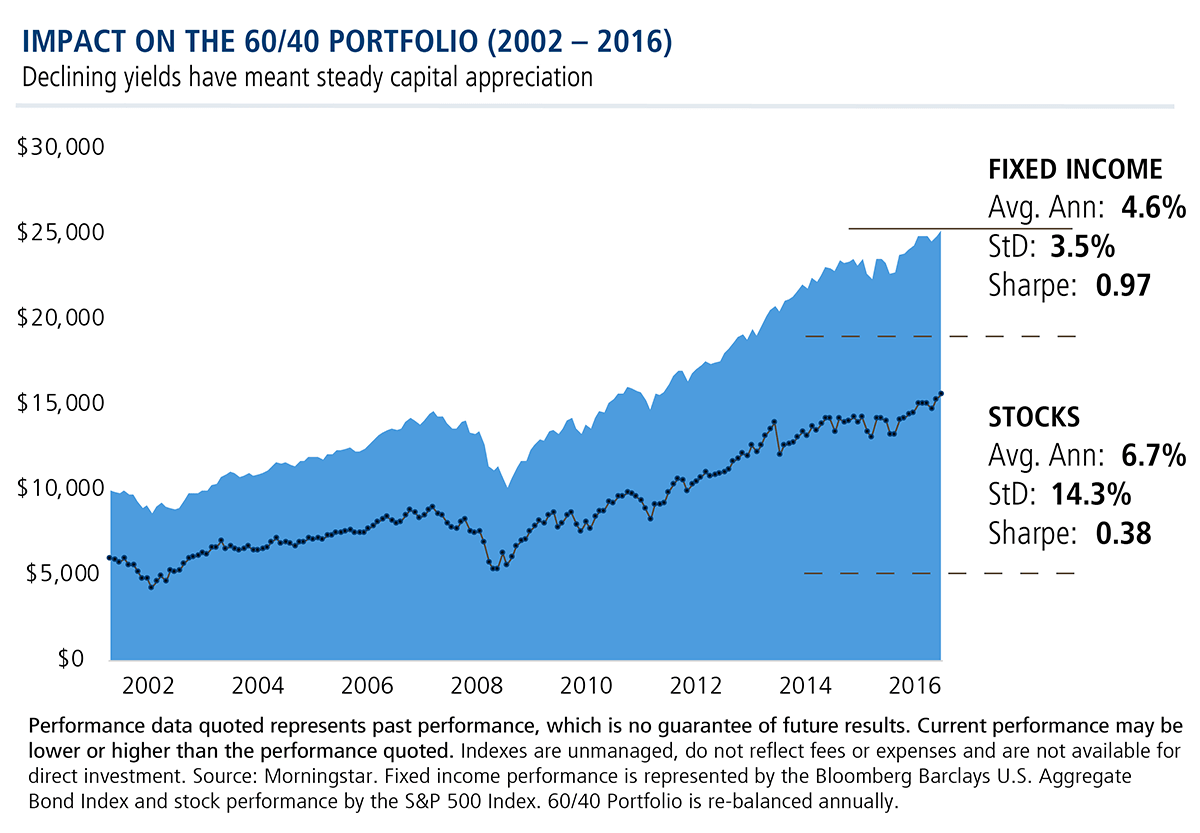

60/40 Portfolio in Jeopardy

Click image to enlarge

Click image to enlarge

Calamos President and Head of Global Distribution Robert Behan opened the webcast with a challenge to advisors: “Over the last several years portfolios of a 60/40 mix have had a tremendous tailwind with the steady decline of interest rates. That has provided on the one hand excellent total return opportunity in the bond side, on the other hand fairly low yields.

“After years of a tremendous bull market, the risk reward is definitely skewed toward the potential of not having those type of returns or that tailwind in the future. It may be at best neutral and at worst a headwind,” Behan said.

“What’s your outlook on the interest rate environment or the total return prospects of fixed income over the next three to five years? And what’s your view of equity prospects?”

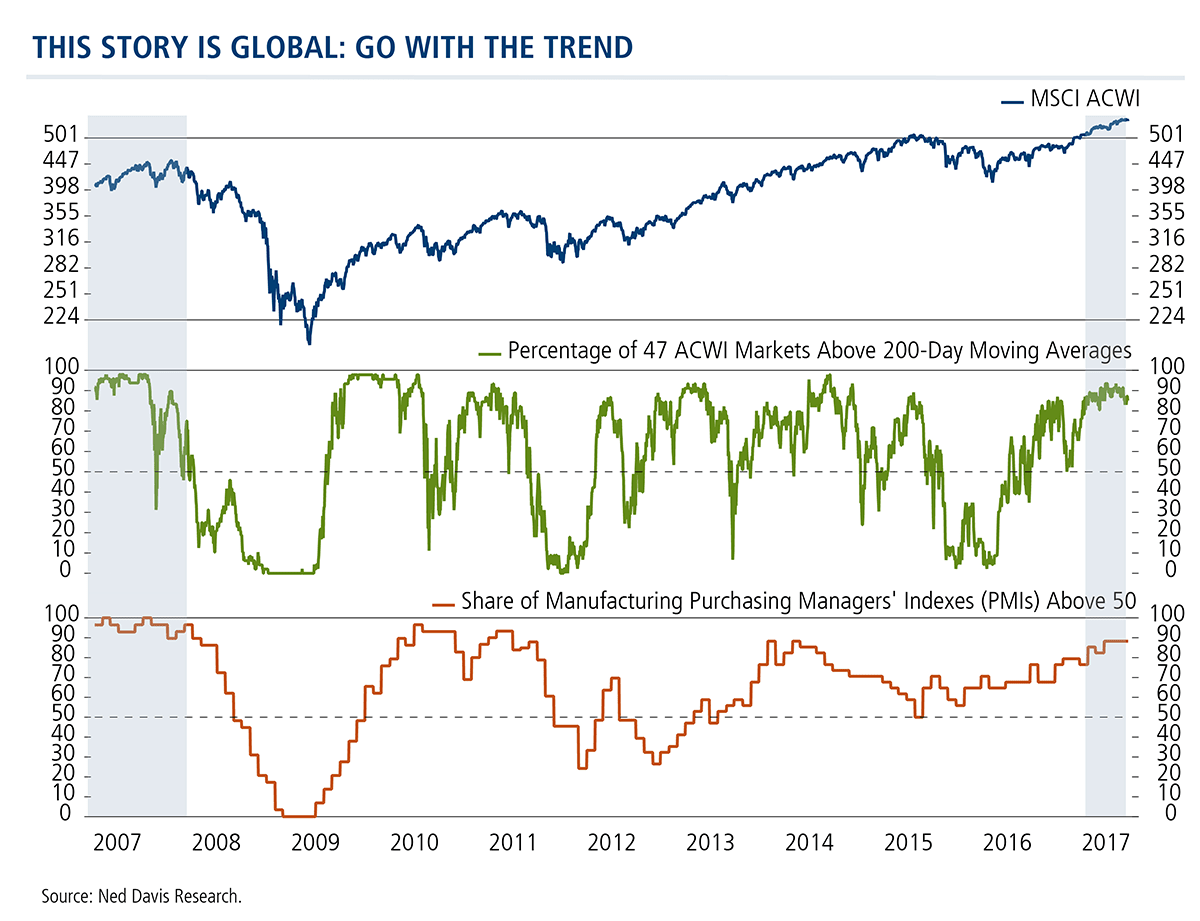

Go with the Trend

According to Grant, if there was a single idea that explains the changed nature in equity performance since last autumn, it’s the emergence of stable, sustained and synchronous global GDP growth. It’s “the game changer,” he said.

“Post-2008 through 2016, whenever one part of the world economy was doing well, another part of the world was near or in depression-like circumstances. This is the first year where all of the major GDP blocs are pulling in the same direction."

The recommendation from Grant: Go with the trend through 2017 and believe in global growth.

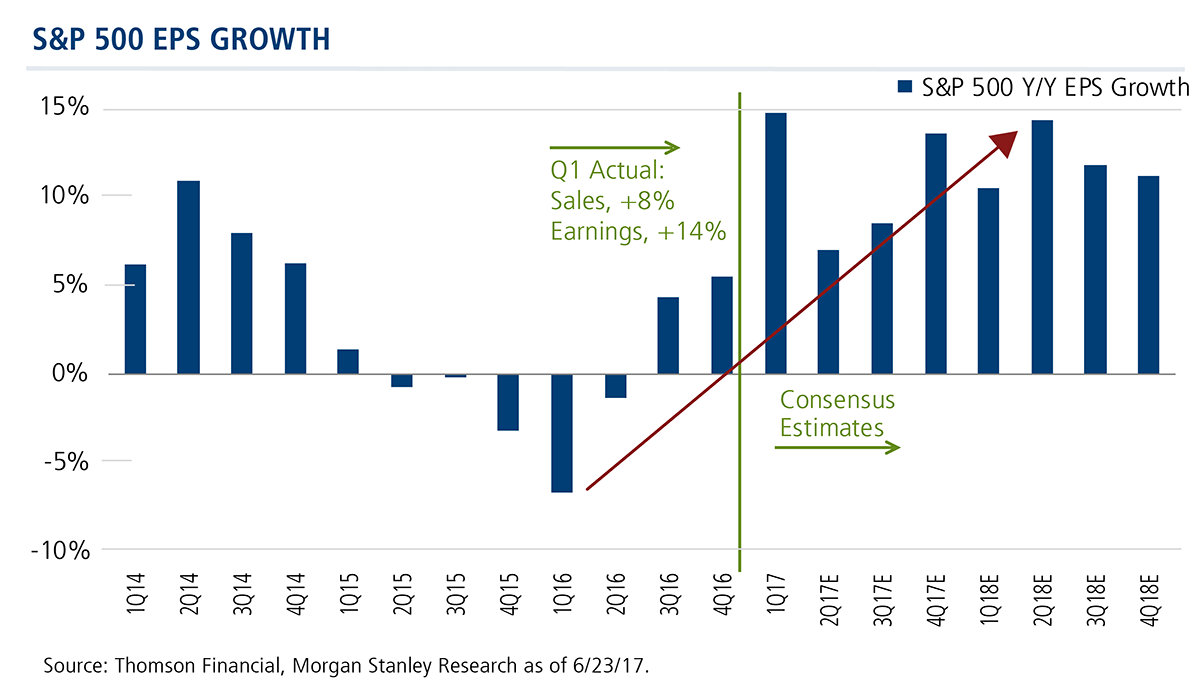

Equities Head Higher

As long as the year-over-year growth rate in sales and profits is accelerating, equities typically head higher, Grant believes.

“It’s not until we see a peak in that growth rate either late this year or early in 2018 that we have to consider the possibility of a topping process in the market itself,” he said.

Volatility this year, Grant expects, will be confined to sector rotation rather than any meaningful pullback in the broader market.

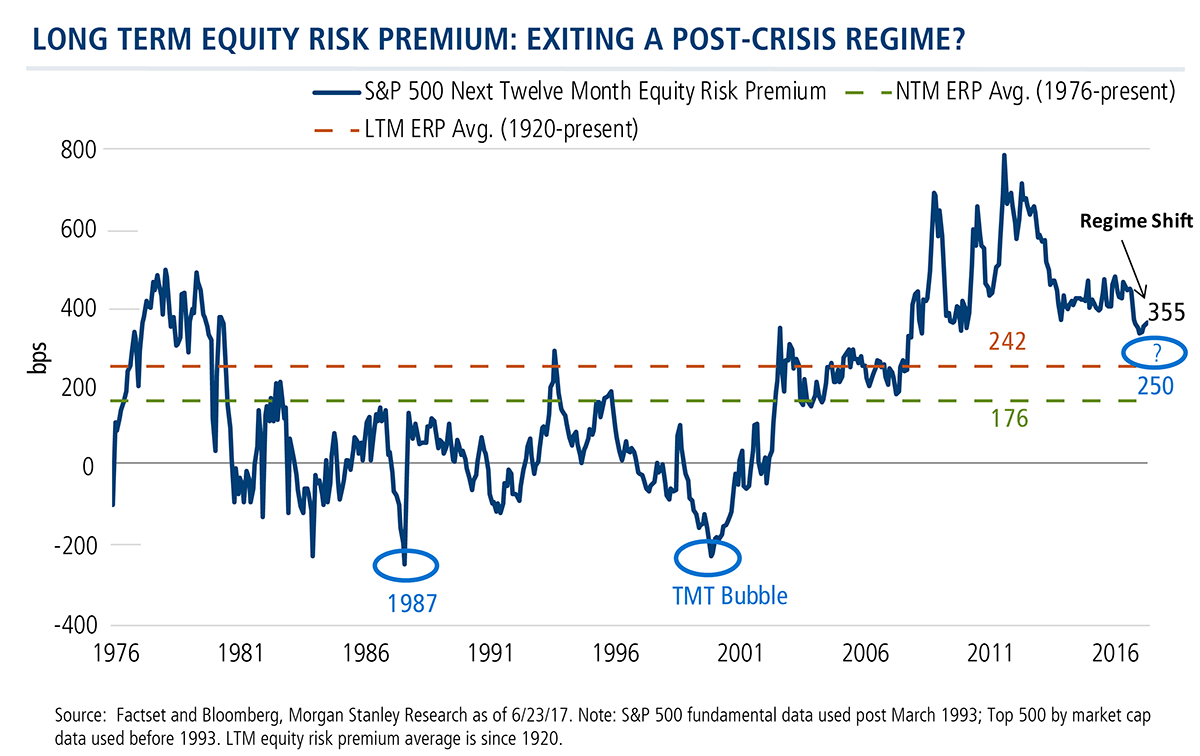

Valuations

Grant acknowledged advisors’ and clients’ concerns that the stock market is overpriced. Valuation, according to Grant, is “subjective and volatile but the most important call to get right.”

But in a low interest rate world, equity valuations are actually undemanding.”

Grant’s call: That valuations will remain elevated. “Normally, as investors shake off their deflation fears, the transition from deflation to reflation is the period when valuations remain typically high,” he said.

The chart below tracks the Equity Risk Premium, which is the excess return that investing in the stock market provides over a risk-free rate, such as the return from government Treasury bonds. On this basis, the real bubbles in equities occurred in 1987 and the late 1990s. After 2008, equities became cheap relative to interest rates because of pervasive skepticism over the sustainability of the economic system itself.

“The intriguing question,” Grant said, “is whether this relationship between interest rates and equities can normalize toward the red and green lines on this slide, which are the historical averages.

“If we assume, for example, an Equity Risk Premium of 250 basis points with the U.S. 10-year yield rising gently to 2.75%, we can get an S&P 500 target of 2700,” Grant said. “If the economy in 2018 is in fact stronger and investors can begin to discount $150 in earnings for the S&P 500, there’s upside beyond that.”

The important point, in Grant’s view, is that the nonconsensus upside for equities depends heavily upon these valuation assumptions.

Bull to Bear

Could the bull market turn bear, another advisor concern?

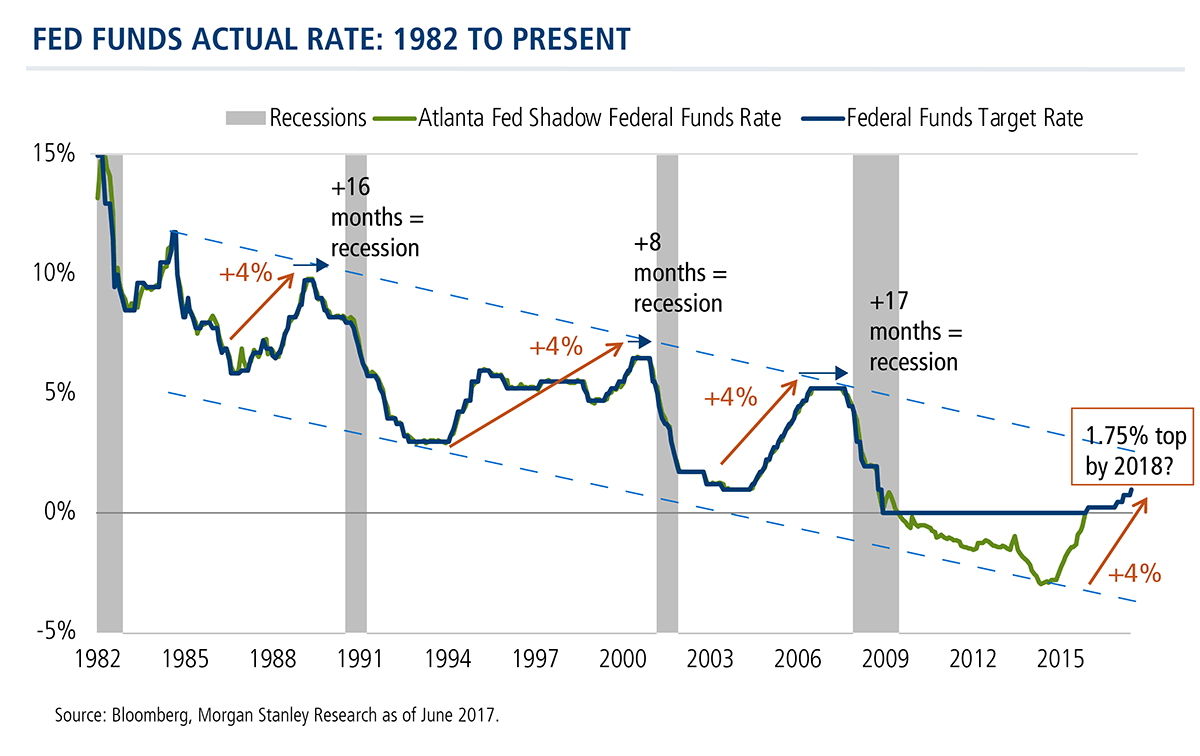

Grant believes Fed policy can avoid “a recession-induced bear market.” Shown below is the typical Fed rate cycle over the last several decades. According to Grant, rates haven’t yet reached levels that induce recession but that “pinch point” could be reached in H12018.

Citing historical patterns, Grant said the second year prior to recession (2017) is usually a healthy year for equities, followed by a “topping process” (2018).

The Political Environment

Some have marveled at both the strong performance of the equity markets and lack of volatility, given the start of the Trump administration.

Grant’s take: “I would argue that what we’re seeing is more about the global business cycle and less about Trump because many of these trends actually emerged in the middle of last year, prior to the November presidential election.”

The political “noise,” he suggested, may be obscuring the strength of the global upturn, as well as its underlying causes.

“It’s true that actual reform under the new administration has disappointed. That said, the reduction in industry-specific risk feels real to me. The risk of operating in certain industries like finance or media, telecom and energy has definitely fallen,” said Grant.

According to Grant, tax reform would be a positive catalyst for equities, one that’s not priced in today. He believes that tax reform would raise the likelihood that 2018 is a healthy or healthier economy than 2017.

The Most Undervalued Idea

Asked for the most undervalued asset, Grant preferred to discuss the most undervalued idea, which he proffered is the possibility that secular stagnation is truly behind us.

“There’s still a pervasive belief in the permanence of today’s slow growth world. I suspect investors are underestimating the upside optionality for global GDP growth.

“Almost any bond investor would tell you that nominal yields are anchored by nominal GDP growth. That relationship broke down in the last five years when investors everywhere moved into the deflation camp,” Grant continued.

Nominal GDP growth here in the U.S. is slightly more than 4%. If Trump is “even modestly successful,” it may get to 5%, said Grant, noting that interest rates remain in the middle 2s range.

“There’s a big, big gap between where interest rates are and where they could be in a different global GDP setting. My perspective,” Grant said, “is that even a small shift toward a more benign secular view, together with positive earnings revisions, could be meaningful for equities.”

For more information about CPLIX or our income alt CMNIX, please talk to your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. For the most recent month-end fund performance information visit www.calamos.com.

Alternative investments may not be suitable for all investors, and the risks of alternative investments vary based on the underlying strategies used. Many alternative investments are highly illiquid, meaning that you may not be able to sell your investment when you wish to. Unmanaged index returns assume reinvestment of any and all distributions and, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Phineus Long/Short Fund include: equity securities risk consisting of market prices declining in general, short sale risk consisting of potential for unlimited losses, foreign securities risk, currency risk, geographic concentration risk, other investment companies (including ETFs) risk, derivatives risk, options risk, and leverage risk.

The principal risks of investing in the Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

The MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of developed market countries in North America, Europe and Asia/Pacific region.

The S&P 500 Index – generally considered representative of the U.S. stock market.

The VIX (CBOE volatility index) is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options.

Earnings per share (EPS) is a company's profit divided by its number of common outstanding shares.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

800401 0817

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end performance information, please CLICK HERE. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower. For the most recent month-end fund performance information visit www.calamos.com.

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived on August 08, 2018