Narrowing Spreads Prompt a Shift Away from High Yield and Toward Convertibles

June 23, 2017

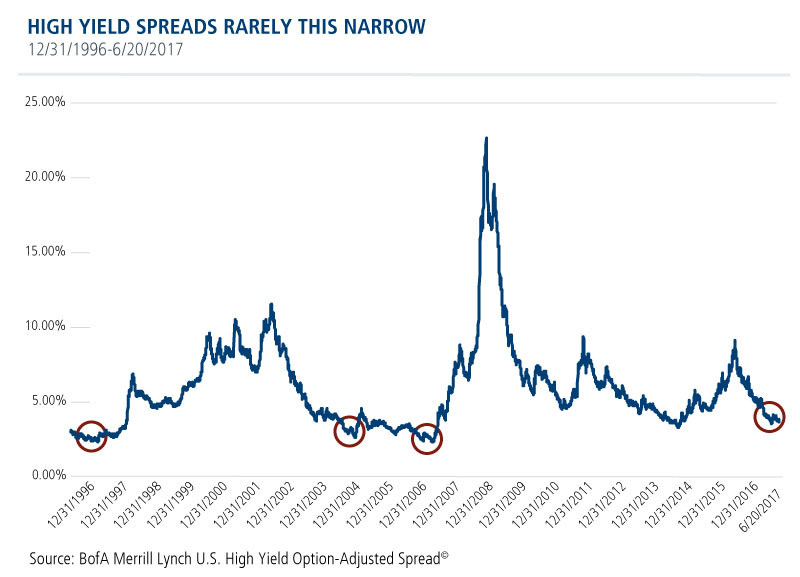

Since 1996 there have been just four periods when high yield credit spreads were as narrow as they are today.

The tightening is prompting many advisors to consider their high yield allocations. After a strong run, what’s the potential for the way forward?

Your next move may depend upon your expectations of the overall economy. If you think that conditions will continue to improve, high yield’s upside from here may be limited.

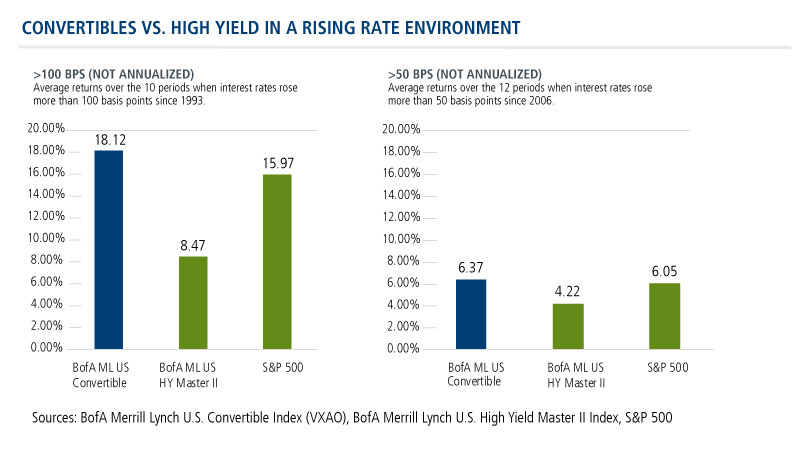

It’s in such a period—when rates are rising and spreads are narrowing—when convertible securities perform well (also see Readying Your Clients’ Portfolios for Rising Interest Rates).

Because a convertible bond includes the option to be converted into stock, a rising price of the underlying stock increases the value of the convertible security. The upside is unlimited. By comparison, high yield is capped at the yield.

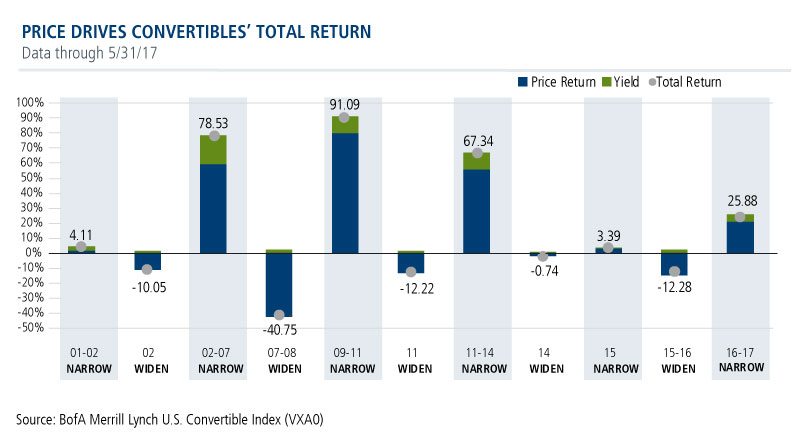

Note in the chart below that price gains drive convertibles’ total return during periods of narrowing spreads.

For More Information about Convertible Securities

Advisors, could you use additional information about convertible securities and how they’re used? We can help. Our firm’s Founder, Chairman and Global CIO John P. Calamos, Sr. is an acknowledged pioneer, and our Investment Consultants are experts on the subject. For more information, please talk to your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Also see:

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee against a loss. This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Convertible securities entail interest rate risk and default risk.

Total return assumes reinvestment of dividends and capital gains distributions and reflects the deduction of any sales charges, where applicable. Performance may reflect the waiver of a portion of the Fund's advisory or administrative fees for certain periods since the inception date. If fees had not been waived, performance would have been less favorable.

The S&P 500 Index is considered generally representative of the U.S. equity market.

The BofA Merrill Lynch U.S. Convertible Index (VXA0) is considered generally representative of the U.S. convertible market.

The BofA Merrill Lynch U.S. High Yield Master II Index tracks the performance of U.S. dollar-denominated below investment grade rated corporate debt publicly issued in the U.S. domestic market.

The BofA Merrill Lynch Option-Adjusted Spreads (OASs) are the calculated spreads between a computed OAS index of all bonds in a given rating category and a spot Treasury curve. An OAS index is constructed using each constituent bond’s OAS, weighted by market capitalization.

A convertible bond is at a “distressed” valuation when it is worth significantly less than the theoretical value of a similar non-convertible bond and is highly sensitive to changes in the underlying equity price. A convertible bond has “fixed income characteristics” when it is valued at about the same level as a similar non-convertible bond and is not as sensitive to the underlying equity. A convertible bond has “hybrid characteristics” when it has fixed income characteristics as previously explained but is becoming increasingly sensitive to changes in the underlying equity price. “Equity characteristics” represents a convertible bond that is highly sensitive to movements in the underlying equity.

Active management does not guarantee investment returns and does no eliminate the risk of loss.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

800213 0617