In March, we published a post discussing the upside we saw for convertible securities. While convertibles had struggled along with other risk assets during the turmoil of early 2016, we identified three factors—a trifecta—that could provide a tailwind to convertible securities. We wrote:

Credit spreads have widened dramatically, equities have declined significantly, and convertible valuations have cheapened. A reversal in any one of these factors could provide a tailwind to convertibles, and if all three reverse, convertibles may be poised for a potentially powerful “trifecta.”

Since then, the U.S. convertible securities market has come back strong. The BofA Merrill Lynch All U.S. Convertibles Index (VXA0) is up 20.31% since the February 11 low through August 15, performing much in line with the S&P 500 Index, up 21.08%. Revisiting each of the three factors of our trifecta, what we expected to see has begun to occur:

- Credit spreads have tightened. High yield credit spreads have narrowed to 617 bps as of July 31, down from 782 basis points at the end of February. High yield bonds, as reflected by the BofA Merrill Lynch High Yield Index are up 20.11% since the February 11 low through August 15.

- Equities have rebounded. In March, we noted that the “level of decline in the underlying stocks of the VXA0 has also been a precursor to healthy rebounds.” The equities underlying the convertible index are now up 33.03% since February 11 through August 15, outpacing the S&P 500’s gain of 21.08%.

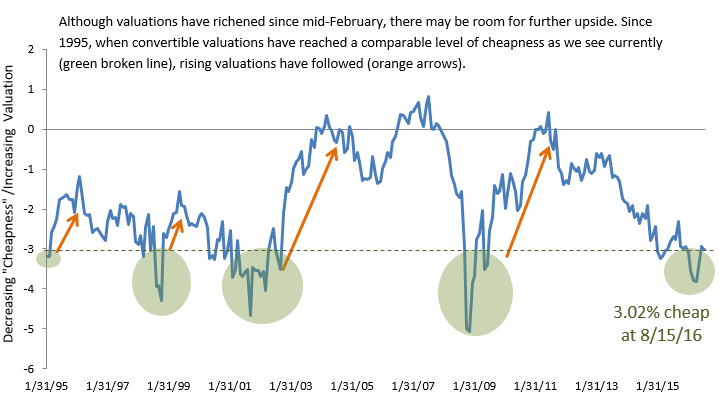

- Convertible valuations have risen. As shown in Figure 1, valuations have strengthened.

Figure 1: BofA Merrill Lynch: Convertible % Cheap (January 31, 1995 through August 15, 2016)

Past performance is no guarantee of future results. Source: BofA Merrill Lynch. The % cheap measure is based on constituents in the VXA0.

Although the convertible market has improved from February lows, we see continued opportunities for active and selective managers. In regard to our trifecta:

- While spreads are more normal, company-specific catalysts may result in further credit spread improvements.

- Many convertible issuers are growth-oriented companies. As our investment committee noted in its recent outlook, we believe the case for growth-oriented equities remains strong. This should bode well for convertibles, as many issuers are from growth areas of the market.

- Although convertible valuations have recovered slightly from February’s levels, we believe they can continue to improve.

In a slowly growing economy where financial markets are likely to remain volatile, we believe convertible securities can provide the opportunity to capture equity upside with potentially less downside. However, given the appreciation that we have seen over recent months in the asset class—and the economic and market choppiness we expect to continue—we could well see greater disparity in returns, highlighting the need for an active approach to security selection and portfolio construction.