CMNIX Awarded Morningstar Medalist Rating

July 21, 2020

Morningstar this month upgraded its analyst rating for Calamos Market Neutral Income Fund (CMNIX) to Bronze. As described by Morningstar in a post last November, “the Analyst Rating is a forward-looking, qualitative rating that sets forth Morningstar’s fundamental assessment of a fund’s merits. It takes the form of Gold, Silver, Bronze, Neutral, and Negative, with the highest ratings going to funds the analysts’ research leads them to conclude will outperform over a market cycle, and Neutral and Negative ratings to those they lack conviction in.”

The evaluation is based on five key pillars—process, performance, people, parent and price—that the analysts believe “lead to funds that are more likely to outperform over the long term on a risk-adjusted basis.”

Process. The Analyst commentary comments on the fund’s investment process, which “combines an effective convertible arbitrage strategy and a dynamic, yet conservatively-managed options strategy, resulting in a risk-aware approach.”

“…Although the team manages the options dynamically, it’s thoughtful about risk management with strict limits in place, bolstering our confidence and resulting in an upgrade to the Process Pillar. Since the strategy benefits from rising and falling volatility, it should provide steady returns in most market environments.”

The assessment, which is behind the Morningstar.com paywall, also includes the following notes about CMNIX:

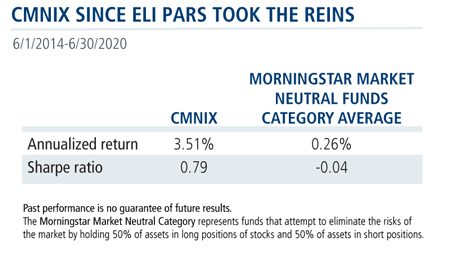

Performance. “Calamos Market Neutral Income has generated modest but steady returns since Eli Pars took the reins in June 2014, resulting in strong risk-adjusted performance and returns that placed in the best decile of the Market Neutral Morningstar Category under his watch. From June 2014 through June 2020, the fund’s institutional shares returned 3.5% annualized compared with the Market Neutral Category average of 0.3%. It achieved those results with muted volatility, resulting in an attractive Sharpe ratio of 0.8.”

People. “The close-knit team managing this strategy is led by an experienced pair of hands. Pars is supported by Co-managers Jason Hill, David O'Donohue, and Jimmy Young, who also bring dedicated convertible-arbitrage and options-trading experience to the table. The team works together to determine asset allocation and pick individual securities while also utilizing a dedicated analyst and another nine sector specialists to bolster its fundamental research across convertible bonds and equities.”

Price. “The share class on this report levies a fee that ranks in its Morningstar category’s cheapest quintile. Based on our assessment of the fund’s People, Process and Parent pillars in the context of these fees, we think this share class will be able to deliver positive alpha relative to the category benchmark index.”

Investment professionals, for more information on CMNIX or the rest of our liquid alternatives suite, contact your Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

The Morningstar Analyst RatingTM is not a credit or risk rating. It is a subjective evaluation performed by Morningstar’s manager research group, which consists of various Morningstar, Inc. subsidiaries (“Manager Research Group”). In the United States, that subsidiary is Morningstar Research Services LLC, which is registered with and governed by the U.S. Securities and Exchange Commission. The Manager Research Group evaluates funds based on five key pillars, which are process, performance, people, parent, and price. The Manager Research Group uses this five-pillar evaluation to determine how they believe funds are likely to perform relative to a benchmark over the long term on a risk adjusted basis. They consider quantitative and qualitative factors in their research. For actively managed strategies, people and process each receive a 45% weighting in their analysis, while parent receives a 10% weighting. For passive strategies, process receives an 80% weighting, while people and parent each receive a 10% weighting. For both active and passive strategies, performance has no explicit weight as it is incorporated into the analysis of people and process; price at the share-class level (where applicable) is directly subtracted from anexpected gross alpha estimate derived from the analysis of the other pillars. The impact of the weighted pillar scores for people, process and parent on the final Analyst Rating is furthermodified by a measure of the dispersion of historical alphas among relevant peers. For certain peer groups where standard benchmarking is not applicable, primarily peer groups of funds using alternative investment strategies, the modification by alpha dispersion is not used.

The Analyst Rating scale is Gold, Silver, Bronze, Neutral, and Negative. For active funds, a Morningstar Analyst Rating of Gold, Silver, or Bronze reflects the Manager Research Group’s expectation that an active fund will be able to deliver positive alpha net of fees relative to the standard benchmark index assigned to the Morningstar category. The level of the rating relates to the level of expected positive net alpha relative to Morningstar category peers for active funds. For passive funds, a Morningstar Analyst Rating of Gold, Silver, or Bronze reflects the Manager Research Group’s expectation that a fund will be able to deliver a higher alpha net of fees than the lesser of the relevant Morningstar category median or 0. The level of the rating relates to the level of expected net alpha relative to Morningstar category peers for passive funds. For certain peer groups where standard benchmarking is not applicable, primarily peer groups of funds using alternative investment strategies, a Morningstar Analyst Rating of Gold, Silver, or Bronze reflects the Manager Research Group’s expectation that a fund will deliver a weighted pillar score above a predetermined threshold within its peer group. Analyst Ratings ultimately reflect the Manager Research Group’s overall assessment, are overseen by an Analyst Rating Committee, and are continuously monitored and reevaluated at least every 14 months.

For more detailed information about Morningstar’s Analyst Rating, including its methodology, please go to https://shareholders.morningstar.com/investor-relations/governance/Compliance--Disclosure/default.aspx.

The Morningstar Analyst Rating (i) should not be used as the sole basis in evaluating a fund, (ii) involves unknown risks and uncertainties which may cause the Manager Research Group’s expectations not to occur or to differ significantly from what they expected, and (iii) should not be considered an offer or solicitation to buy or sell the fund.

Morningstar RatingsTM are based on risk-adjusted returns for Class I shares and will differ for other share classes. Morningstar ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly historical performance (reflecting sales charges), placing more emphasis on downward variations and rewarding consistent performance. Within each asset class, the top 10%, the next 22.5%, 35%, 22.5%, and the bottom 10% receive 5, 4, 3, 2 or 1 star, respectively. Each fund is rated exclusively against U.S. domiciled funds. The information contained herein is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Source: ©2020 Morningstar, Inc. All rights reserved.

The principal risks of investing in Calamos Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

The Bloomberg Barclays US Government/Credit Index comprises long-term government and investment grade corporate debt securities and is generally considered representative of the performance of the broad U.S. bond market. Unlike convertible bonds, U.S. Treasury bills are backed by the full faith and credit of the U.S. government and offer a guarantee as to the timely repayment of principal and interest.

The FTSE 30-Day T-Bill Index is generally considered representative of the performance of short-term money market instruments.

The Morningstar Market Neutral Category represents funds that attempt to eliminate the risks of the market by holding 50% of assets in long positions of stocks and 50% of assets in short positions.

Sharpe ratio is a calculation that reflects the reward per each unit of risk in a portfolio. The higher the ratio, the netter the portfolio's risk-adjusted return is.

802087 720

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived material may contain dated performance, risk and other information. Current performance may be lower or higher than the performance quoted in the archived material. For the most recent month-end fund performance information visit www.calamos.com. Archived material may contain dated opinions and estimates based on our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions at the time of publishing. We believed the information provided here was reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load. Had it been included, the Fund’s return would have been lower.

Archived on July 21, 2021