Investment Team Voices Home Page

Investment Team Voices Home Page

Pole Position for a Market Powered by Earnings

July 1, 2026

Nick Niziolek, CFA

Calamos Global Equity Team

- While some investors may worry that the market’s strength has been powered by unsustainable price momentum, the data says otherwise: earnings improvements and upward earnings revisions are driving markets higher.

- Even after the strong gains we’ve seen in global equities, we believe there’s more upside to come, supported by powerful secular growth themes.

- We believe the current market environment sets up well for our approach: a proprietary process that emphasizes growth fundamentals and thematic tailwinds, implemented by a team organized around themes rather than sectors.

As global equities have continued to rally, we’re often asked if we’re in a late-cycle momentum market, where prices are climbing because investors are reflexively chasing climbing prices.

The good news is that we believe this read on the markets is wrong. We see a market driven by earnings and durable secular trends, which price momentum is confirming. Around the world, innovative companies are seizing on the unprecedented opportunities of AI and other growth themes.

This creative disruption is at the heart of what is driving prices higher. For the better part of two years, market participants have consistently underestimated how quickly earnings would need to be revised higher to keep pace with a rapidly changing global economy. By Goldman Sachs’s estimates, Wall Street entered each of the past two years expecting roughly 20% growth in hyperscaler capital spending, and actual growth more than doubled those forecasts, topping 50% growth in both 2024 and 2025.1

The Engine Is Earnings

Our constructive outlook on what’s driving markets was also echoed in recent research by Piper Sandler. In “2 Trades Are Dominating Markets … And Both Are About Earnings,” Piper notes stocks leading the market are the ones with earnings that Wall Street analysts have had to keep revising higher, and that earnings, not multiple expansion, have been “the real engine behind this market.” As shown in Figure 1, the next-12-months earnings estimates for the S&P 500 jumped 17.3% since January. Earnings have accounted for the entirety of this gain and then some, because the market’s price-to-earnings multiple has actually compressed. The report makes an important point: if valuations had held flat, the index would be higher. In contrast to many prior cycles when valuations were a tailwind, valuations today are a headwind.

Figure 1. Earnings, Not Multiples, Have Driven this Market

Change since January 2026

Source: Piper Sandler, “2 Trades Are Dominating Markets … And Both Are About Earnings,” Portfolio Strategy, Macro Research, June 17, 2026. Past performance is no guarantee of future results.

Breadth Beyond Big Tech

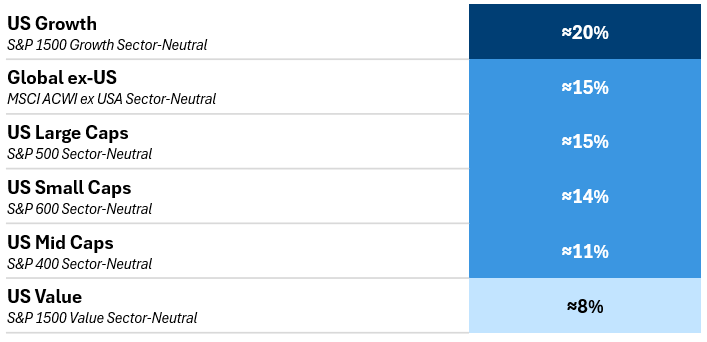

As fundamentally driven growth managers, we’re especially excited to see earnings growth rewarded across the board. As data from Piper shows (Figure 2), the earnings-momentum factor is working across investment styles, the market capitalization spectrum, and in the United States and globally.2 Although the impact of the earnings-momentum factor is most pronounced among US growth stocks, it is propelling global equities and value stocks, too.

Earnings Momentum: Rewarded Across Equity Markets

Relative Performance of Highest over Lowest Quintile, EPS Momentum

July 2025 to June 2026

The chart above shows EPS Momentum Factor; cumulative total return outperformance is approximate. Sector-neutral: Sector returns within the index are equally weighted. Source for data: Piper Sandler, “2 Trades Are Dominating Markets … And Both Are About Earnings,” Portfolio Strategy, Macro Research, June 17, 2026. Past performance is no guarantee of future results.

Our Process: An Excellent Fit for a Market Rewarding Fundamentals

With interest rates unlikely to fall materially from here and secular growth drivers positioned to fuel unprecedented upside, we expect earnings to continue to do the lifting. This is exactly the kind of environment our team welcomes because it rewards disciplined, fundamentally driven processes over ramping up risk. A market that rewards companies with strong growth fundamentals—like earnings growth momentum—sets up well for our approach.

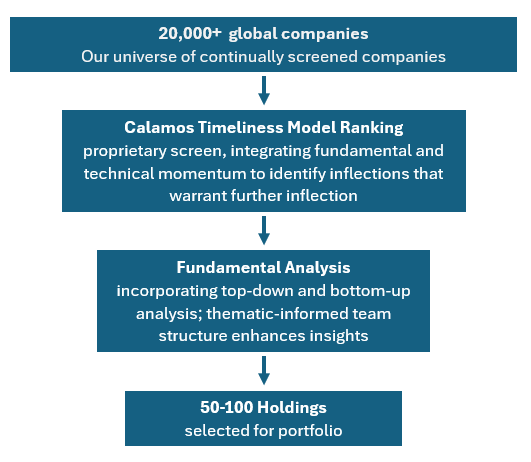

Calamos Global Equity Team Investment Process

Our proprietary process is designed to identify companies where earnings are inflecting before stock prices fully reflect the turn.

Our Team Structure: Aligned for a Market Driven by Fundamentals and Earnings Momentum

Instead of organizing coverage around GICS sectors as most managers do, the Calamos Global Equity team is structured around eight secular and three cyclical investment themes. Our thematic framework is designed to anticipate inflection points, providing a critical advantage over a sector-driven framework that is more likely to recognize opportunities only after the fact.

The growth themes driving earnings—most notably, capital expenditures for the AI buildout, the restructuring of global supply chains, and the need to power and electrify a digitizing world—cut straight across sector lines. As we argued in our recent paper, “The AI Inflection: Investing Beyond Sectors in a Thematic World,” a theme-driven framework gives us the ability to make the connections and see the opportunities that sector-driven frameworks could easily miss, or significantly underestimate.

The Opportunity Is Broadening

As growth investors, we’ve been excited by the opportunities AI disruption has already brought but are even more excited about what’s to come. For two years, the leadership has been narrow and concentrated in the most direct beneficiaries of the AI capex cycle, but this is changing. With the energy and inflation outlook improving and geopolitical tensions moderating in the Middle East, our process is leading us to a widening set of opportunities in more cyclical corners of the market that did not screen well when the recovery was narrow.

With the opportunity set wider, the competition for inclusion in our portfolios is stiffer—every potential investment has to clear a higher bar to earn a place. For an active manager, that is about as good a problem as there is. Over the past several weeks, we have rotated a portion of our AI exposure into emerging cyclical opportunities. To be clear, this is not a loss of conviction in the AI capex buildout, which is a theme that remains very much intact.

In contrast, while this is a great environment for our active approach, index funds and static, quasi-passive managers are poorly equipped to navigate it. A portfolio anchored to last cycle’s winners is a bet that the world has stopped changing. What matters most over the next twelve months is where earnings inflect next, and whether our process can identify it before the crowd does. We are confident that this is a market that plays to the strengths of our thematic and fundamentally driven approach.

1 Goldman Sachs Research, “Why AI Companies May Invest More than $500 Billion in 2026,” December 2025.

2 Piper Sandler, “2 Trades Are Dominating Markets … And Both Are About Earnings,” Portfolio Strategy, Macro Research, June 17, 2026.

This material is provided for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any security. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions and are subject to change without notice. References to specific securities, asset classes, and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. Past performance is no guarantee of future results.

Indexes are unmanaged, do not include fees or expenses and are not available for direct investment. The S&P 500 Index measures the performance of large-cap US equities. The S&P Small Cap 600 Index measures the performance of small-cap US equities. The S&P MidCap 400 measures the performance of mid-cap equities. The S&P 1500 Value Index measures the performance of small-, mid-, and large-cap stocks with value attributes based on book value, sales-to-price, and earnings ratios. The S&P 1500 Growth Index measures the performance of small-, mid-, and large-cap stocks with growth attributes based on sales growth, earnings change-to-price, and momentum. (Source: S&P Global). The MSCI ACWI ex USA index measures the performance of mid- and large-cap companies outside the United States (Source: MSCI.)

026052 0626