Since late 2014, we’ve held a positive view on core European and Japanese equity markets, while taking a selective approach in regard to emerging market equities. This served us well in 2015, as did our exposure in reflationary and weak currency beneficiaries. As we look forward to the rest of the year, we’re maintaining constructive view on core Europe and Japan and have become incrementally more positive on emerging markets.

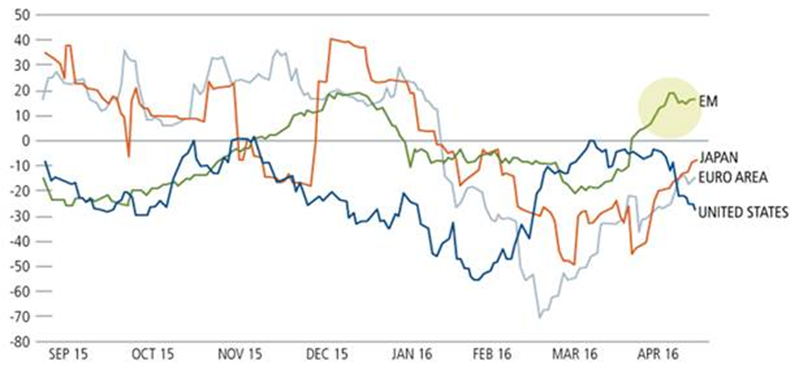

Since the February bottom, we’ve seen a steady tick higher in economic surprises across Japan and Europe, and the surprise indicator for emerging markets has moved into positive territory (Figure 1). With significant stimulus in China beginning during 4Q15 and very accommodative monetary policy in Europe and Japan, we’ve seen a stabilization and improvement in data which has the potential to continue over the next few quarters. These improvements, combined with more dovish U.S. monetary policy, have contributed to the global rally we’ve seen in commodities and cyclicals.

Figure 1. Positive Surprises on the Upswing in EMs, Japan and Euro Area

Citi Economic Surprise Index

Source: Macrobond

When we look at valuations globally, Europe, Japan, and emerging markets continue to look relatively more attractive, while expectations for earnings and revenue growth are similar and/or better when compared to the United States. Within Europe, we’ve favored select real estate opportunities because we believe a low interest rate environment and reflationary policies should continue to benefit sentiment. Many European companies that were unloved for their Chinese exposure have more recently benefited from China’s stimulus measures. We remain cautious on the sustainability of this cyclical pick-up, but valuations are attractive and companies are beating expectations (albeit lowered ones), which may continue for the next few quarters.

Year to date, Japanese equities have underperformed due in part to concerns about the efficacy of monetary policy and poor communication from the Bank of Japan. As we look toward the second half of 2016, we see several catalysts that could reverse sentiment. We believe it is likely that an increase to the value-added tax will be postponed and the BOJ will ramp up asset purchases. Also, there is greater potential for additional reforms as we move past this election cycle.

Figure 2. Attractive Relative Valuations and Fundamentals in Japan, Europe, and EMs

Past performance is no guarantee of future results. Source: Bloomberg

Many headwinds that emerging markets have faced over the past few years have reversed and are providing near-term tailwinds. A weaker dollar, rising/stabilizing commodity prices, and stabilizing/improving economic conditions in many countries have contributed to the increased market interest in many emerging markets. The initial stages of this rally have been driven by cyclicals/value equities and more commodity-dependent economies, but as this recovery builds we expect this re-rating to extend to companies and countries with stronger fundamentals and more sustainable medium-term growth profiles. We maintain an emphasis on countries such as the Philippines, India, and China, where improving economic freedoms and the implementation of needed reforms provide a sustainable basis for growth.

Given this more favorable backdrop we’ve seen for emerging markets, we’ve also seen a rally in companies based in developed markets that have significant EM exposure. As investor sentiment has improved for EM, so has sentiment towards these companies with significant EM exposure. We’ve seen some positive surprises from the emerging market portions of many of businesses, which has supported the rebound we’ve seen in valuations. This trend has been favorable to our emerging market strategies where we invest not only in emerging market based companies, but also developed market companies with significant revenue exposure to emerging markets.