- Surprise move to remove the majority of currency from circulation has roiled the Indian equity market.

- In our view, market selloff overlooks the long-term benefits of demonetization: weeding out corruption in the underground economy, reducing counterfeiting, improving tax collections, encouraging expansion of the banking system and stimulating credit growth in the Indian economy.

- We view demonetization as a decisive step in Prime Minister Modi’s long-term plans to strengthen the Indian economy and advance economic freedoms.

- India remains one of the most compelling stories in the emerging markets, and we are viewing the selloff as a buying opportunity.

India’s equity market has faced a fair share of headwinds in 2016. From January through the high in emerging markets in early September, India fell short of the broader emerging markets’ advance as countries with higher interest rates benefited more from the global fall in yields. Also, India was not immune from the toll that Donald Trump’s victory took on emerging markets more broadly. India’s recent decline, however, was significantly exacerbated by Prime Minister Modi’s surprise announcement on November 8 to withdraw ₹500 and ₹1000 notes from legal currency. Under the demonetization directive, holders were given two choices for their old notes: exchange notes for new ₹500 or ₹2000 notes or deposit them into a bank account.

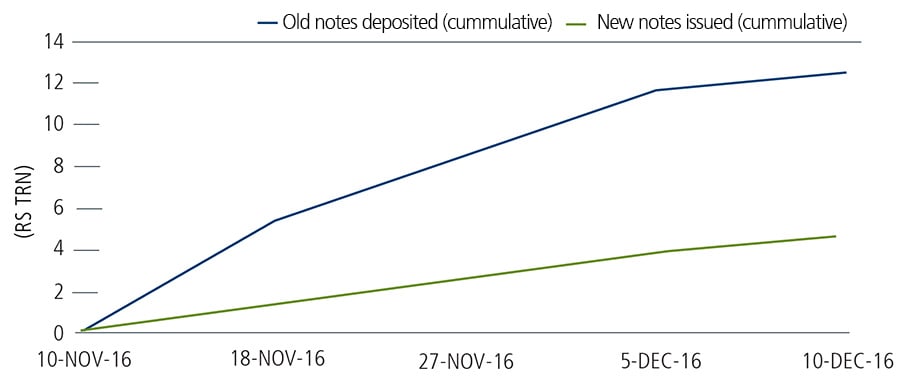

Not unexpectedly, the initial days of implementation saw considerable turmoil. These notes represented more than 85% of the currency outstanding in the largely cash-based Indian financial system. In practical terms, the notes serve a function within the commerce system similar to $10 and $20 bills in the United States.

Immediately following the announcement, the central bank was unable to print enough cash fast enough, banks were not staffed to accommodate the increased traffic, and ATMs were not fitted for the new currency. There were long lines at banks, and people waited hours to exchange notes. Due to shortages of the new currency, banks placed limits on the amount of cash that could be exchanged daily, and the process became a multi-day ordeal for many individuals. There was significant disruption to both consumer and business spending. In the initial days and weeks following the announcement, there were reports of convenience stores with no sales and commercial vehicles and two-wheelers left on roadsides because drivers did not have money for fuel.

Despite these initial hurdles, demonetization has gone better than expected. According to CLSA, 80% of the old notes were exchanged or deposited during the first four weeks of the program, with the expectation that more than 90% will be exchanged or deposited by year end. Only about 25% of old notes have been replaced with new notes; to some extent, this has been a by-product of banking and exchange limitations. However, this high level of deposits supports the government’s goal of reshaping India’s financial system into one that is increasingly digitized.

Source: CLSA.

While we believe the longer-term positives are compelling, it is clear that demonetization creates near-term headwinds for India’s economy. A decline in available currency is likely to be a drag on economic growth and to increase deflationary pressures. The duration of the impact remains to be seen—for example, if this will be a 1Q17 issue or one that stretches through 2017. One could reasonably expect a ramp-up in asset quality issues for companies with greater exposure to the cash economy, such as consumer finance, commercial vehicle finance, loans against property, small and medium sized enterprises, and housing and developer finance. We’re encouraged that India’s central bank, the Reserve Bank of India, has temporarily relaxed rules related to non-performing loans.

The majority of personal wealth in the Indian economy is held in real assets (such as real estate and gold) and offshore accounts. Even so, there will likely be some degree of wealth destruction, as unreported income and counterfeit money remains un-exchangeable. There will also be negative short-term wealth impacts for those who sell perishable goods (for example, farmers or fishermen) and haven’t been able to transact business during the cash crunch. Meanwhile, the highest income segment is likely to feel an indirect hit to wealth due to declining real estate values.

Demonetization may also lead to increased unemployment, already a problem in the Indian economy. The real estate sector, one of India’s largest employers, is widely expected to experience the strongest negative impact due to demonetization. Moreover, many small businesses that were able to operate in the cash-based economy will be less competitive in the post-demonetization environment. As jobs disappear from these small businesses, new structural employment hurdles may emerge as many people lack the skills to move into the growing formal sector.

As we have discussed in past blog posts, we believe Prime Minister Modi’s platform can provide a catalyst for the country’s long-term economic expansion. However, there is political risk associated with demonetization, particularly if Modi’s Bharatiya Janata Party cannot show that the benefits of demonetization will outweigh the negative impacts. Key elections this spring should provide a good barometer of the political environment and sentiment.

That said, the government has a number of tools it can use to combat the near-term demonetization headwinds. These include a ramp-up in government spending for affordable housing and infrastructure programs, which can help offset the near-term drop in private demand and the employment overhang, especially in the real estate sector. Additionally, a deflationary environment would provide the Reserve Bank of India with more flexibility to lower rates, and lower rates generally support increased credit growth.

Our View: Demonetization Will Benefit India Over the Long Term

Although global investors took a dim view of Modi’s surprise move, we believe demonetization is another positive step in India’s economic reform trajectory. In fact, India remains one of our favorite emerging markets and we have used the recent selloff as a buying opportunity.

Demonetization creates a more favorable environment for business and foreign investment by discouraging corruption and shrinking the underground economy. Tax evasion has long been a problem in India and demonetization should help the government enhance tax collection efforts. These revenues can be used to fund an array of much-needed infrastructure projects and programs, including affordable housing.

Further, demonetization advances Modi’s goals of strengthening India’s financial system and increasing bank penetration and credit growth. Due to a combination of high inflation rates and a large underground economy, savings have been concentrated in real assets and about of a quarter of India’s population do not have bank accounts. Demonetization provides a significant growth catalyst for the banking system, as it promotes the “financialization” of savings (depositing of money into banks). Over time, as people look for better returns, money can move throughout the financial system, from savings accounts and banks into insurance and asset management. Finally, demonetization provides a catalyst for digitalization as demand increases for mobile payment systems and e-commerce.

The Case for India is Supported by Many Factors

Expansion of a middle class. Demographics support a broad and growing opportunity set in India. The country has a large population with growing incomes, and the emergence of its middle class is in more nascent stages. GDP per capita in India is less than a third of that in China, which means that consumer activity has a relatively longer runway as the India economy expands. Members of our team recently traveled to India, where we observed strengthening consumer trends across the income spectrum, from growing demand for basic staples to “trading-up” for higher-end goods. For example, motorcycles are an especially popular form of transportation. As consumers make a little more money, they often elect to trade-up from a motorcycle that costs $1000 to a better one that costs $2000.

While there are a number of similarities among emerging market consumers, there are key differences. One nuance that we observed during our recent trip is that compared to the typical Chinese consumer, Indian consumers appear relatively less concerned with Western brands. However, Indian consumers are quite focused on getting a good value for what they spend. This means that popular local brands may be positioned particularly well as the Indian economy grows and consumers become more affluent.

“Make in India.” As we noted, demonetization is just one policy in Prime Minister Modi’s ambitious plans for sweeping economic reforms. His “Make in India” initiative, which includes expanding and modernizing the country’s manufacturing sector, has resulted in increasing government spending for infrastructure projects. As India focuses on building manufacturing capabilities and easing the movement of commerce and capital goods across the country, we see considerable opportunities for a wide range of infrastructure-related companies, such as those involved in the building of roads, bridges and railroads.

A simplified tax code. Demonetization follows on the heels of the introduction of a new and simplified goods and services tax (GST) policy, which is presently making its way through the legislative approval process. Although the pace of implementation has slowed a bit, we still expect the bill to pass next year. As noted in a recent blog post, we view the GST as an important step in improving the ease of transacting business, cross-state commerce, while also supporting increased tax collections. While initially inflationary, the GST should provide a long-term tailwind to an array of Indian companies, especially those focused on the domestic market.

Conclusion

Demonetization may create short-term headwinds for the Indian economy. However, we believe many market participants are overlooking the longer-term benefits. As we look out to the medium and longer-term, our thesis for India remains quite constructive. Our readers are familiar with the emphasis we place on economic reforms as a catalyst for growth, and we continue to be encouraged by the direction of Modi’s policies. Together with secular growth opportunities tied to the consumer, these economic reforms provide a favorable backdrop for a variety of companies in India.