Convertible securities may be less well known than stocks and bonds, but they offer many potential benefits. Convertibles combine characteristics of stocks and bonds; and with active management, they can enhance overall portfolio diversification and support multiple asset allocation goals. For example, convertibles can be used for lower-volatility equity participation and enhanced fixed income exposure. They can also be used within alternative strategies. (To learn more about how convertibles work, read our in-depth guide.)

Because of their versatility, we believe convertibles are best thought of as a strategic allocation to be held over full and multiple market cycles. However, the case for actively managed convertibles is especially strong today:

-

During the second half of the year, convertibles should benefit in advancing but volatile equity markets. The U.S. economic expansion continues, supported by an upbeat consumer, strong corporate earnings, contained inflation, deregulation and tax reform. Against this backdrop, there is more room for stocks to advance. At this point of the economic cycle, the prospects may be especially strong for growth-oriented and smaller-cap names, which are well represented in the convertible universe.

However, with mid-term elections, trade concerns, more normalized interest rates, and a higher level of global economic uncertainty, markets will be volatile in the short term. During downturns, convertibles can be more resilient than stocks because bond attributes (including coupon income) provide a floor. Alternatively, when equity markets rise, the convertible typically becomes more valuable (its embedded option can participate in equity upside).

-

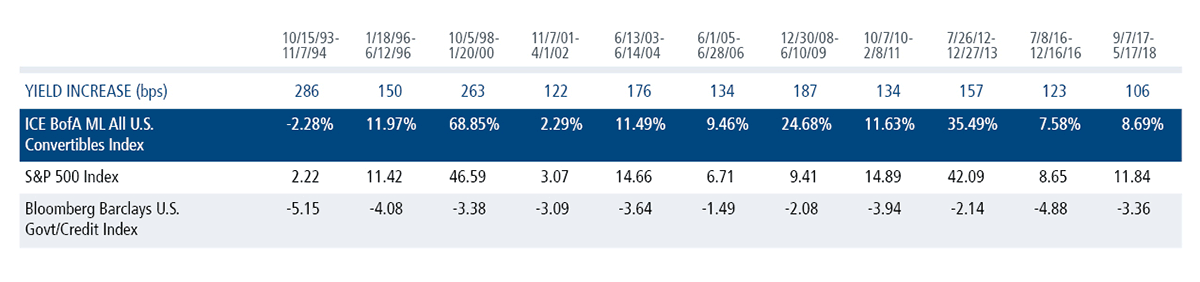

Convertibles have outperformed bonds during rising rate environments. Thanks to their equity characteristics, convertible securities have performed well versus bonds during periods of rising interest rates—including this most recent period. Although we don’t expect interest rates to soar, we do expect the Federal Reserve to maintain its gradual tightening as the U.S. economy extends its growth phase. Over the past 25 years, there have been 11 periods when the yield of the 10-year U.S. Treasury rose more than 100 basis points. During every one of these periods, convertibles outperformed bonds.

Figure 1. Convertibles Have Outperformed Traditional Bonds When Interest Rates Rise

Returns in Rising Rate Environments

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

-

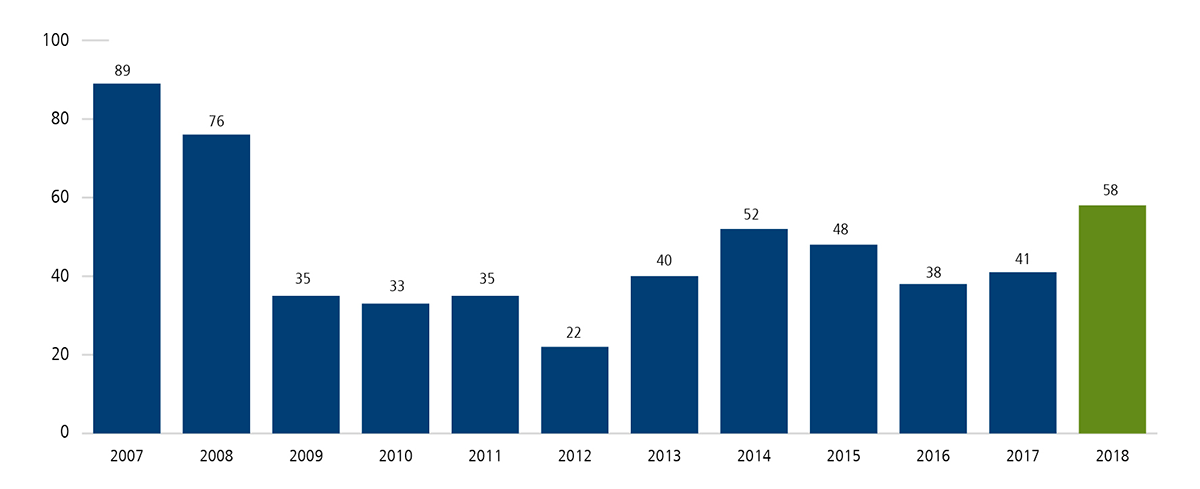

The robust convertible issuance we’ve seen so far this year is likely to continue. During the first half of 2018, global issuance topped $57 billion, the fastest pace since 2008. The U.S. led the way, with $34 billion. There was a dramatic upswing in Asia ex-Japan issuance, where companies issued $12 billion. Rounding out global issuance, European and Japanese companies brought $10 billion and $2 billion of paper to market, respectively. BofA Merrill Lynch estimates that full-year global issuance could be the highest in 12 years; this seems reasonable based on the many tailwinds I see for the asset class.

Figure 2. Favorable Tailwinds Drive Convertible Security Issuance

1H Global Convertible Issuance, 2007-2018 ($bil)

Source: BofA Merrill Lynch Global Research.

Several factors are contributing to this increase in new convertible securities. Most importantly, convertible issuance is about capital market access, and capital market access is tied to economic growth. In this climate, we expect companies to seek capital to forge ahead with mergers, acquisitions, R&D and capital spending.

Higher interest rates in the U.S. make convertibles more attractive to issuers than non-convertible debt. This is because convertibles issuers can typically offer a lower coupon in exchange for providing investors with the opportunity to participate in the upside of the convertible’s underlying equity. Also, recent changes to U.S. tax codes have limited interest deductibility for corporations, strengthening the relative appeal of issuing a convertible security instead of a non-convertible one.

-

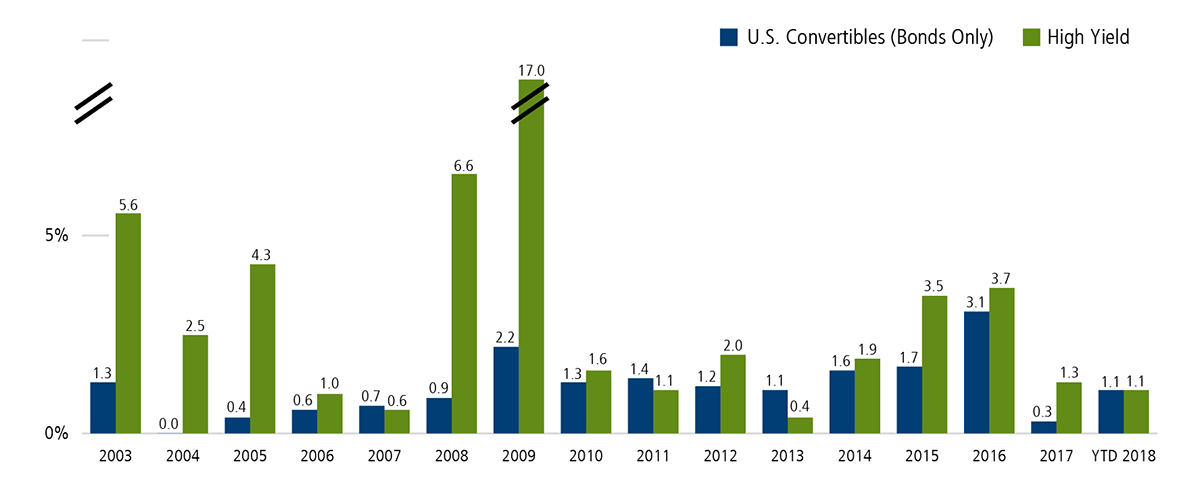

Convertible default rates have been low. The following graph, based on data provided by Barclays Research, highlights the low levels of defaults in convertible bonds over time. The average convertible default rate from 2003 to April 2018 was 1.2% versus 3.4% for high yield. One reason for this is that compared with high yield issuers, there are fewer convertible issuers with distressed balance sheets.

Figure 3. Historically, Convertible Bonds Have Seen Low Defaults

Default Rate, 2003-April 2018

Past performance is no guarantee of future results. Source: Barclays Equity Research, April 30, 2018; using data from Barclays Research and Moody’s, as of April 25,2018. *Based on defaulted positions in the Bloomberg Barclays High Yield Index which is a subset of the defaulted U.S. Senior Unsecured positions by Moody’s.

-

The opportunity set is growing for risk-conscious approaches like ours. Issuers structure convertibles in many ways, which is why active management is essential. For example, convertibles vary in their levels of equity and fixed-income sensitivity. Convertibles with very high levels of equity sensitivity may fall short in terms of providing downside protection. Conversely, convertibles with disproportionately high levels of fixed income sensitivity can be sidelined in rising stock markets. In recent years, convertibles with mandatory conversion features became increasingly popular among issuers, but these structures often entailed a degree of equity exposure that gave us pause. This year, the tide has shifted in a positive direction for our approach. We’re seeing companies with attractive growth characteristics issue convertibles with more balanced stock and bond attributes—and these are the securities we generally emphasize in our long-term, risk-managed strategies.