Investment Team Voices Home Page

Investment Team Voices Home Page

The AI Capex Boom Has an International Address

Where US AI spending actually lands

May 19, 2026

Nick Niziolek, CFA

Co-CIO, Head of Global Strategies, Senior Co-Portfolio Manager

We believe:

- The impact of the US capex boom provides another proof point that a “Great Global Rebalancing” is underway, supporting international equity market outperformance and significant opportunities for many non-US companies at the forefront of AI growth themes.

- Chip manufacturers in emerging Asia, Japan-based companies in optical networking and European industrial companies are riding powerful US-driven demand curves.

The narrative around the AI capital spending cycle has been almost entirely a US story: Capex for the top five US hyperscalers is on track to exceed $750 billion in 2026, S&P 500 profit margins are at record highs, and the bulk of investor attention has been focused on a handful of US mega-caps.1 However, these US-centric headlines could easily lead investors to overlook a key point: international companies could well be the biggest beneficiaries of US AI spending.

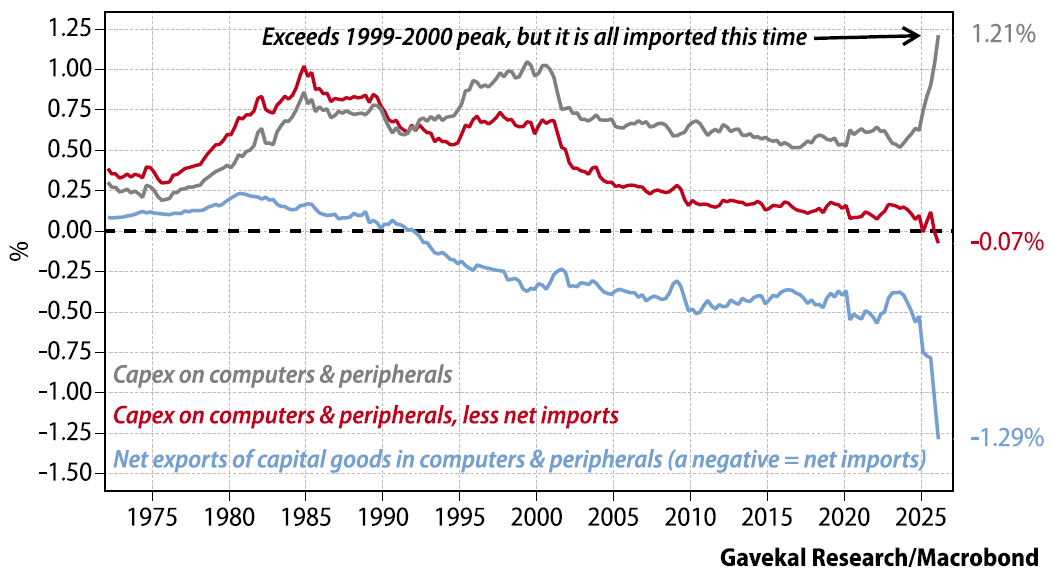

In fact, we believe that the US capex boom supports our thesis that a Great Global Rebalancing is gaining traction, with a long runway ahead. A recent paper from Gavekal Research, “Navigating the AI Bubble: An Update,” provides plenty of ammunition for our outlook. Gavekal’s Will Denyer notes that US capital spending on computers and peripherals just hit a share of nominal GDP higher than the late 1990s peak, but that almost none of it is produced in the US.2

As Gavekal shows (Figure 1), capex on computing equipment (the gray line) is at all-time highs. But once you net out imports, US-produced capex (the red line) is roughly flat to slightly negative. Net exports (the blue line) have fallen to a record low of -1.29% of GDP.

Every additional dollar spent in the US on GPUs, servers, networking, and cooling is, on the margin, a dollar of revenue for a foreign supplier.2 We believe this is one of the most important structural reasons select international companies have outperformed so dramatically over the past year, and why we believe this rotation has staying power.

Figure 1. The US imports most of the equipment that goes into its AI data centers

Share of nominal GDP

Source: Gavekal Research, Macrobond. "Navigating The AI Bubble: An Update," May 7, 2026.

Where the Capex Actually Lands

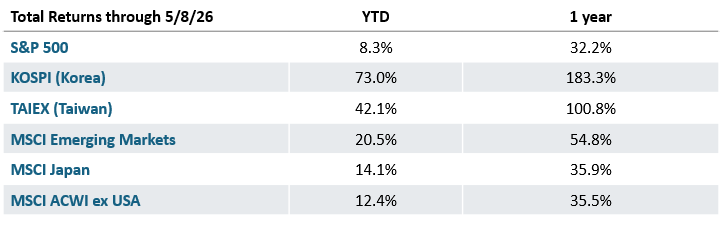

As long as US hyperscalers keep spending, we believe leading Asia-based memory-chip companies (e.g., SK Hynix and Samsung, Korea) and logic-chip companies (Taiwan Semiconductor Manufacturing Company, Taiwan) are well positioned. According to UBS, we are in the midst of the strongest run of earnings upgrades in emerging markets in 20 years, driven by Korean and Taiwanese chipmakers benefiting from a memory chip shortage that UBS expects to last into 2027.3

The math driving Korea’s equity market is especially striking. Although the KOSPI has rallied dramatically, earnings are growing faster than prices, and the market is cheaper today than when the rally began. The KOSPI's forward P/E has compressed year-to-date.4 Meanwhile, KOSPI net profit estimates for 2026 have been revised higher by more than 100% over the past year, with semiconductors alone accounting for more than 80% of the upgrade, according to CLSA data.5

The US AI capex surge is also a boon to Japanese companies across the AI supply chain, including optical networking (Fujikura), electronic components (Murata), and semiconductor manufacturing equipment (Tokyo Electron). (Our white paper, "The AI Inflection: Investing Beyond Sectors in a Thematic World" takes a closer look at the optical networking layer.)

Figure 2. Who stands to gain from US AI Capex?

Much of the equipment for the US AI buildout is being built internationally, and companies in Asia are reaping some of the most significant rewards.

Past performance is no guarantee of future results. Source: Bloomberg. Indexes are unmanaged, do not include fees or expenses and are not available for direct investment.

European Companies: Powering the US Grid Buildout

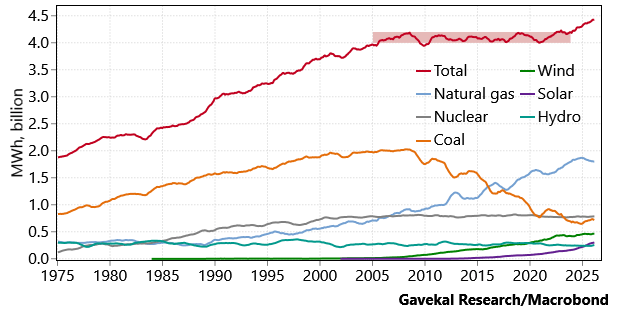

As Figure 3 from Gavekal shows, US net electricity generation is finally growing again, with natural gas, nuclear, solar, and wind all contributing.2 Supply needs to make up a lot of ground to meet the explosive growth in power demand driven by AI data centers. Closing the gap will require massive US investment in machinery and industrial innovations that power the grid. Here again, US companies won’t be the only winners. The supply chain is global, and many European companies are especially well-positioned.

Figure 3. US electricity generation is starting to grow after two flat decades

Net electricity generation, annualized, 12-month average, EIA

Source: Gavekal Research, Macrobond, US Energy Information Administration. "Navigating The AI Bubble: An Update," May 7, 2026.

Siemens Energy in Germany has become one of the most direct beneficiaries of US data center power demand, with a multi-year backlog for gas turbines and grid equipment. Iberdrola in Spain is a key driver of grid expansion and modernization across both Europe and the Americas. Schneider Electric (France) and ABB (Switzerland) supply the medium- and low-voltage equipment that goes inside every hyperscale facility.

US AI Capex: A continued boon to international companies

We have been writing about a multi-year rotation into overseas markets since early 2025, and a year later, the speed of the move has surprised even us. We are happy to have been positioned for the turn. We believe that the US AI capex cycle has plenty of fuel left, and international companies will continue to benefit as billions of dollars of US data center spend flow into orders for memory and logic chips (emerging Asia), optical technology (Japan), and power equipment (Europe). Our thematically driven approach has been key to identifying opportunities across geographies as the Great Global Rebalancing gains traction, and we’re confident that it will continue to drive our results.

1Source for hyperscaler capex: CreditSights, "Tech: Raising Hyperscaler Capex 2026 Estimates," February 2026.

2Gavekal, “Navigating the AI Bubble: An Update,” Will Denyer, May 7, 2026

3UBS, “The case for extended EM outperformance — 30 key charts,” February 23, 2026. Emerging markets as measured by the MSCI Emerging Markets Index.

4Bloomberg, as of May 15, 2026.

5CLSA, “Korea strategy: More to go,” Jongmin Shim, February 2026.

As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to the potential for greater economic and political instability in less developed countries.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors.

References to specific companies, securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to buy or sell.

The S&P 500 Index is considered generally representative of the US large-cap equity market. The Korea Composite Stock Price Index (KOSPI) is a market capitalization-weighted index of all common stocks listed on the Stock Market Division of the Korea Exchange. It is the primary benchmark of the South Korean equity market. The Taiwan Stock Exchange Capitalization Weighted Stock Index (TAIEX) is a market capitalization-weighted index that measures the aggregate performance of all common stocks listed on the Taiwan Stock Exchange, excluding preferred stocks, full-delivery stocks, and newly listed stocks. It is the primary benchmark of the Taiwanese equity market. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Japan Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of the large- and mid-cap segments of the Japanese market. The MSCI ACWI ex USA Index measures global equity performance, excluding the US.

As of 3/31/2026, the most recently available date for which a complete list of holdings is published to www.calamos.com, Calamos International Growth Fund held the following as a percent of net investments: SK Hynix, Inc., 2.14%; Samsung Electronics Company, Ltd., 2.26%; Taiwan Semiconductor Manufacturing Company, Ltd., 6.45%; Fujikura, Ltd., 1.99%; Tokyo Electron, Ltd., 1.57%; Siemens Energy, AG, 3.06%; Iberdrola, SA, 1.04%.

As of 3/31/2026, the largest positions as a percent of net assets in Calamos International Growth Fund were as follows: Taiwan Semiconductor Manufacturing Company, Ltd., 6.38%; ASML Holding, NV, 3.21%; Siemens Energy, AG, 3.02%; Hyundai Motor Company, 2.94%; Rolls-Royce Holdings, PLC, 2.85%; UniCredit S.p.A., 2.48%; Samsung Electronics Company, Ltd., 2.25%; SK Hynix, Inc., 2.13%; Mitsubishi Heavy Industries, Ltd., 2.02%; Fujikura, Ltd., 1.96%.

As of 3/31/2026, the most recently available date for which a complete list of holdings is published to www.calamos.com, Calamos Global Equity Fund held the following as a percent of net investments: Samsung Electronics Company, Ltd., 2.96%; Taiwan Semiconductor Manufacturing Company, Ltd., 4.79%; Tokyo Electron, Ltd., 1.14%; Iberdrola, SA, 1.36%.

As of 3/31/2026, the largest positions as a percent of net assets in Calamos Global Equity Fund were as follows: NVIDIA Corp., 7.11%; Taiwan Semiconductor Manufacturing Company, Ltd., 4.64%; Alphabet, Inc. – Class A, 4.42%; GE Vernova, Inc., 2.91%; Samsung Electronics Company, Ltd., 2.89%; Eli Lilly & Company, 2.69%; TechnipFMC, PLC, 2.45%; Rolls-Royce Holdings, PLC, 2.41%; ASML Holding, NV, 2.28%; Amazon.com, Inc., 2.22%.

As of 3/31/2026, the most recently available date for which a complete list of holdings is published to www.calamos.com, Calamos Global Opportunities Fund held the following as a percent of net investments: Samsung Electronics Company, Ltd., 2.75%; Taiwan Semiconductor Manufacturing Company, Ltd., 4.21%; Tokyo Electron, Ltd., 0.82%; Iberdrola Finanzas, SA, 2.42%.

As of 3/31/2026, the largest positions as a percent of net assets in Calamos Global Opportunities Fund were as follows: NVIDIA Corp., 5.30%; Alphabet, Inc. – Class A, 4.24%; Taiwan Semiconductor Manufacturing Company, Ltd., 4.08%; Boeing Company 6.00% Cv Pfd, 3.03%; Samsung Electronics Company, Ltd., 2.68%; Iberdrola Finanzas, SA 1.50% Cv Due 2030, 2.34%; GE Vernova, Inc., 1.88%; Alibaba Group Holding, Ltd. 0% Cv Due 2032, 1.85%; Amazon.com, Inc., 1.76%; Eli Lilly & Company, 1.75%.

All Calamos Global Equity Team Funds: As of 3/31/2026, the funds held 0.0% in Murata, ABB, and Schneider Electric.

026041 0526