Investment Team Voices Home Page

Investment Team Voices Home Page

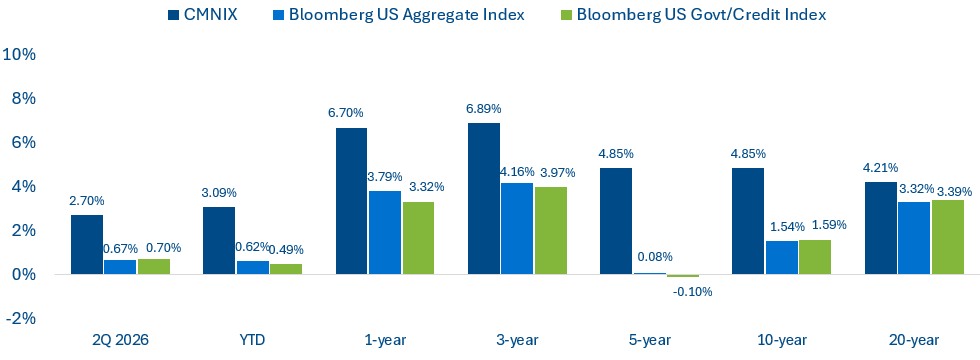

Running at a Steady Pace as Bonds Limp Along

July 1, 2026

Summary Points:

- Calamos Market Neutral Income Fund (CMNIX) is designed to be an all-weather fixed-income alternative, seeking to deliver consistent absolute returns with little exposure to interest-rate risk.

- 2026 has demonstrated the value of our approach: While the bond market generated meager gains, CMNIX posted a steady advance for the second quarter and year to date, as it has for longer periods.

- The fund’s core strategies, convertible arbitrage and hedged equity, were both additive over the quarter, as were the allocations to merger arbitrage and SPAC arbitrage.

Fund Performance and Positioning

We manage CMNIX to provide stable performance regardless of interest rates. The fund has outperformed the bond market over the quarter and year to date, as it has over longer periods.

CMNIX’s Recent Performance Extends a Longer Pattern of Consistent Outperformance

Data as of 6/30/2026. Source: Morningstar. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. All performance shown assumes reinvestment of dividends and capital gains distributions. The fund’s gross expense ratio as of the prospectus dated 2/27/2026 is 1.01% for Class I shares.

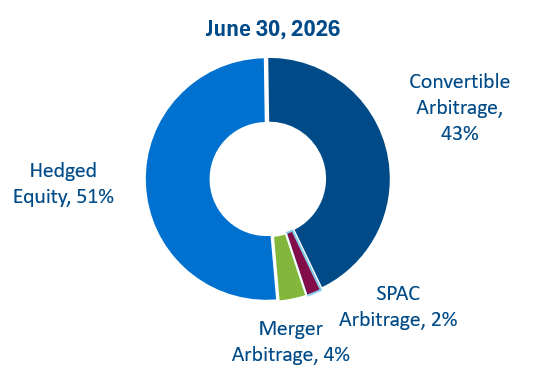

Hedged Equity Strategy

CMNIX: Strategy Allocation

The hedged equity strategy was the most significant contributor to returns for both the second quarter and year to date through June 30, 2026. Although our decision to run a heavier-than-average, more defensive hedge meant that we gave up some equity market upside participation, the increased income we earned from our hedge offset it. Higher interest rates make the calls we write more expensive and the puts we buy cheaper, and when combined with current moderate volatility levels, we believe that a more defensive, income-focused hedge remains ideal for our investors.

We were also active at the margin during the quarter. The core of the hedge stayed in place, but we traded around a small piece of our end-of-June 7500 short calls as volatility moved, covering and re-selling that slice repeatedly to monetize the intra-quarter swings. We ultimately rolled a large portion of the hedge out to August. The structure of the book pays us to be hedged and patient—a posture we believe is most favorable as equities press higher and as policy and geopolitical uncertainty persist.

Convertible Arbitrage Strategy

Convertible arbitrage posted gains broadly in line with hedged equity for both the quarter and year to date. We’re taking advantage of record-breaking new issuance in the convertible market. US convertible issuance reached $62.7 billion in the quarter and $90.0 billion year to date, a pace that annualizes to approximately $180 billion, which would easily surpass last year’s record $119.5 billion to set an all-time high.

The headline deal was Alphabet’s (GOOG/GOOGL) entry into the market. Its two-tranche mandatory convertible totaled more than $19 billion, making it the largest US convertible ever issued. The fact that a mega-cap, Mag Seven issuer chose the convertible structure is also important. Companies are often reluctant to access the capital market in a way that differs from what their market cap or sector peers typically do, so Alphabet’s decision to enter the market could open the door for other mega-cap names to follow.

Alphabet’s issuance was part of a deep roster of large transactions. The issuer mix continues to skew toward capital-intensive growth sectors: AI compute, datacenter and networking infrastructure, semiconductors, crypto-adjacent names, and fintech.

Terms have stayed broadly in line with last year, and investors have continued to step up to meet the supply. That said, a handful of issuers have begun to push terms: We have seen deals priced with zero coupons and conversion premiums north of 60% that not only get done but trade well out of the gate. However, the more telling and encouraging signal is that the secondary market took down record supply without existing paper trading down. This points to structural demand, rather than a temporary bid, and this backdrop sets up well for our unlevered arb approach.

Merger Arbitrage and SPAC Arbitrage

Merger arbitrage and SPAC arbitrage both gained ground for the quarter and year to date. In the merger arb space, deal flow is healthy, and financing is wide open. Federal antitrust regulation has become less of a burden, with vertical and complementary combinations clearing Washington quickly. There are higher regulatory risks on the state and international levels, but we’re still seeing the environment improve overall.

In SPAC arbitrage, we remain focused on structures with positive yield-to-expiration, where short-term rates allow attractive carry on cash held in trust. We continue to deploy the strategy opportunistically and do not anticipate materially increasing the allocation absent a more compelling valuation environment.

Outlook

In CMNIX, we’re not focused on making directional calls on the market. Instead, we want to position the fund to be prepared for as many potential outcomes as possible. In an environment where there’s uncertainty on multiple fronts, we believe this approach will continue to drive steady performance, providing a powerful alternative for investors worried about interest rates and Fed policy direction, equity valuations, and the potential for sharp rotations in a narrow market.

We see many tailwinds for CMNIX’s multi-strategy approach. Convertible issuance should stay robust, benefiting our convertible arbitrage strategy. The rate and volatility environment should provide tailwinds for our hedged equity strategy, and the regulatory backdrop for merger activity remains supportive.

Total Return (%) as of 6/30/26

| 2Q26 | 1 Year | 3 Year | 5 Year | 10 Year | |

|---|---|---|---|---|---|

| Calamos Market Neutral Income Fund (CMNIX) | 2.70% | 6.70% | 6.89% | 4.85% | 4.85% |

| Bloomberg US Govt/Credit Bond Index | 0.70% | 3.32% | 3.97% | -0.10% | 1.59% |

Source: Morningstar. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The fund’s gross expense ratio as of the prospectus dated 2/27/2026 is 1.01% for Class I Shares. You can obtain performance data current to the most recent month end by visiting https://www.calamos.com/funds/mutual/market-neutral-income-cmnix/#_performance.

Average annual returns measure net investment income and capital gain or loss from portfolio investments as an annualized average, assuming reinvestment of income and capital gain distributions. In calculating net investment income, all applicable fees and expenses are deducted from the returns. Calendar year returns measure net investment income and capital gain or loss from portfolio investments for each period specified. The fund also offers Class C shares, the performance of which may vary. Class I shares are offered primarily for direct investment by investors through certain tax-exempt retirement plans and by institutional clients, provided such plans or clients have assets of at least $1 million. For eligibility requirements and other available share classes see the prospectus and other Fund documents at www.calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee a profit or protect against a loss. Alternative strategies entail added risks and may not be appropriate for all investors.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Indexes are unmanaged, do not include fees or expenses, and are not available for direct investment. The Bloomberg US Aggregate Index measures the performance of investment-grade bonds. The Bloomberg US Government/Credit Bond Index includes Treasuries and agencies that represent the government portion of the index and includes publicly issued US corporate and foreign debentures and secured notes that meet specified maturity, liquidity, and quality requirements to represent credit interests.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

Foreign security risk. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility, and difficulty obtaining information. In addition, emerging markets may present additional risk due to the potential for greater economic and political instability in less developed countries.

026054d 0726