Investment Team Voices Home Page

Investment Team Voices Home Page

Picking Our Spots in a Record Convertible Market

July 1, 2026

Jon Vacko, CFA, and Joe Wysocki, CFA

Summary Points:

- We’re finding many opportunities to invest in exciting growth companies with quality fundamentals and less exposure to downside.

- We believe that convertibles can be extremely compelling in an environment characterized by transformative secular trends and economic expansion, but also fast-moving, volatile market conditions.

- We believe active management is the key to unlocking the benefits of the asset class: our focus remains on selecting securities with favorable risk-reward asymmetry and on continuously rebalancing our positions to capitalize on short-term volatility.

Equity markets delivered solid gains in the second quarter, with convertible securities participating meaningfully in the advance. The fund’s returns have been strong this year, a result that we believe reflects both the quality of the opportunity set and the benefits of our active management, which has positioned the fund well to navigate a complex and rapidly evolving environment.

Active Management Maximizes a Compelling Opportunity Set

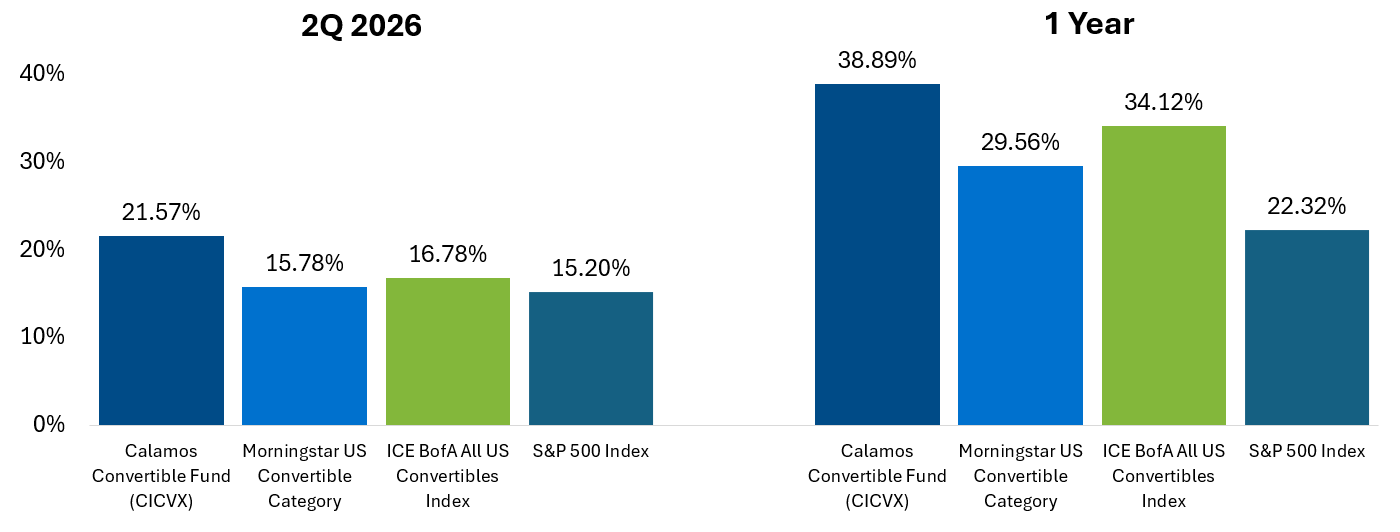

Calamos Convertible Fund outperformed its peers and benchmarks

Data of 6/30/2026. Source: Morningstar. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The fund’s gross expense ratio as of the prospectus dated 2/27/2026 is as follows: I Shares 0.89%.

The geopolitical backdrop remains unsettled, but there are reasons for measured optimism. Although the Middle East conflict wears on, both sides continue to search for an acceptable resolution. A successful de-escalation could lower the geopolitical risk premium, ease oil prices, and provide a meaningful tailwind for consumers and the economy overall. Beneath the geopolitical noise, broader market conditions are constructive: economic growth is solid, overall credit quality is sound, bankruptcy risk is low, and access to capital remains plentiful across IPOs, equity, and debt markets.

Calamos Convertible Fund (CICVX)

Morningstar Overall RatingTM Among 73 Convertibles funds. The Fund's risk-adjusted returns based on load-waived Class I Shares had 4 stars for 3 years, 4 stars for 5 years and 4 stars for 10 years out of 73, 69 and 62 Convertibles Funds, respectively, for the period ended 6/30/2026.

Within Calamos Convertible Fund (CICVX), our overall focus remains on thematic convictions, bottom-up company selection, and active management of security-specific risk-reward tradeoffs across the portfolio. Our portfolio construction reflects both the durability of the AI theme and our readiness to capture a wider opportunity set should conditions warrant.

Information technology and industrials remain the fund’s largest sector overweights, reflecting our view that the AI infrastructure buildout is a structural, multiyear investment cycle. The buildout spans data center construction, power delivery, and connectivity infrastructure. While the debate around AI durability persists, the fundamentals for beneficiaries of the capex infrastructure trend remain exceptional, and the convertible market offers ample opportunities to participate in this theme with favorable asymmetric payoff profiles.

Additionally, if geopolitical tensions ease, inflation cools, and economic growth accelerates, we see a potential case for a broadening of market leadership with cyclical companies benefiting from an improved backdrop. New issuance volume has been remarkable, with $137.5 billion coming to market in the first half of the year, well on pace to shatter last year’s record total. As we detailed in our recent post, “Leaders of Today, Leaders of Tomorrow: Convertible Opportunity in Focus,” convertibles have historically served as growth capital for growth companies, and the AI buildout provides an ideal backdrop for that dynamic to continue. The recent entry of Alphabet into the convertible market reinforces our view that the asset class offers a unique opportunity to invest in the leaders of today and tomorrow in risk-managed structures.

Looking toward the back half of the year, we expect volatility to remain a feature of markets. While midterm elections, geopolitical developments, the ongoing debate over AI’s durability, and Fed policy uncertainty are among the more foreseeable sources of volatility, we expect markets to remain sensitive to a range of developments.

We maintain the fund’s emphasis on companies with improving margins and free cash flow, accelerating returns on invested capital, and attractive equity valuations. Owning these companies through convertible structures allows us to pursue that growth with the added benefit of downside mitigation, a combination we believe is particularly valuable when the range of potential outcomes remains wide.

Total Returns as of 6/30/26

| 2Q26 | 1 Year | 3 Year | 5 Year | 10 Year | |

|---|---|---|---|---|---|

| Calamos Convertible Fund (CICVX) | 21.57% | 38.89% | 19.37% | 7.84% | 12.69% |

| Morningstar US Convertible Funds | 15.78% | 29.56% | 15.78% | 6.34% | 11.52% |

| ICE BofA All US Convertibles Index | 16.78% | 34.12% | 18.19% | 7.71% | 13.15% |

| S&P 500 Index | 15.20% | 22.32% | 20.61% | 13.41% | 15.51% |

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee a profit or protect against a loss. Indexes are unmanaged, not available for direct investment, and do not include fees and expenses. The ICE BofA All US Convertibles Index measures the performance of US convertibles. The S&P 500 Index measures the performance of large-cap US stocks.

Morningstar Convertibles Category funds are designed to offer some of the capital appreciation potential of stock portfolios while also supplying some of the safety and yield of bond portfolios. To do so, they focus on convertible bonds and convertible preferred stocks. Convertible bonds allow investors to convert the bonds into shares of stock, usually at a preset price. These securities thus act a bit like stocks and a bit like bonds. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Morningstar Ratings™ are based on risk-adjusted returns and are through 5/31/26 for the share class listed and will differ for other share classes. Morningstar ratings are based on a risk-adjusted return measure that accounts for variation in a fund's monthly historical performance (reflecting sales charges), placing more emphasis on downward variations and rewarding consistent performance. Within each asset class, the top 10%, the next 22.5%, 35%, 22.5%, and the bottom 10% receive 5, 4, 3, 2 or 1 star, respectively. Each fund is rated exclusively against US domiciled funds. The information contained herein is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Source: ©2026 Morningstar, Inc.

Source for convertible market data: BofA Global Research. Indexes are unmanaged, do not include fees or expenses, and are not available for direct investment.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Convertible Fund include a potential decline in the value of convertible securities during periods of rising interest rates and the possibility of the borrower missing payments. The credit standing of the issuer and other factors may also affect a convertible security’s investment value. Synthetic convertible instruments may fluctuate and perform inconsistently with an actual convertible security, and components of a synthetic convertible can expire worthless. The Fund may also be subject to foreign securities risk, equity securities risk, credit risk, high-yield risk, portfolio selection risk and liquidity risk.

As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility, and difficulty obtaining information. In addition, emerging markets may present additional risk due to the potential for greater economic and political instability in less developed countries.

026054c