Investment Team Voices Home Page

Investment Team Voices Home Page

In a Tightrope Market, Discipline Is the Balancing Pole

July 1, 2026

Jim Madden, CFA, Tony Tursich, CFA, and Beth Williamson

Summary Points:

- Robust corporate earnings and profit margins mask the risks of a narrow market.

- Historically, when momentum-driven markets unwind, quality disciplines have been rewarded.

- Calamos Antetokounmpo Sustainable Equities Fund (SROIX) has been positioned for the turn, and we believe our well-diversified portfolio of quality core growth names will enjoy strong tailwinds in a more risk-aware environment.

- Calamos Antetokounmpo Sustainable Equities Fund emphasizes reasonably valued companies across sectors and geographies, which we believe will support long-term performance and provide resilience as markets rotate.

Markets have spent much of 2026 on a tightrope. Corporate earnings have proven more resilient than expected, and profit margins have reached record levels, yet the rally remains mostly clustered in a band of data-center-linked stocks, and the quarter-end Shiller CAPE ratio for the S&P 500 Index is hovering above 40, just below the all-time high of 44 set during the dot-com peak. Staying invested has been rewarded; complacency has not.

As we have written in prior quarters, the conditions that reward diversification and quality tend to build quietly before they matter. We believe those conditions are now in place.

Earnings Resilience: Better than Expected

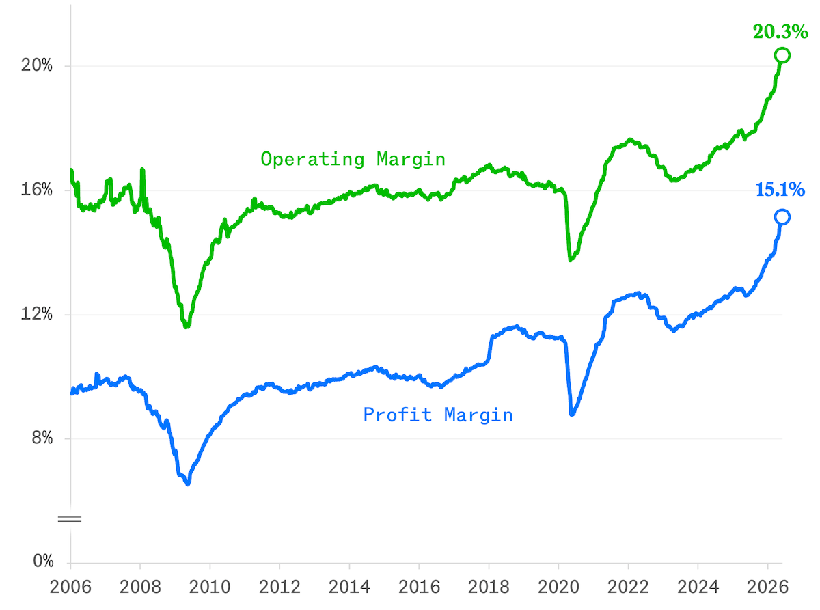

Companies are beating estimates, and profits are at a record level. First-quarter earnings for S&P 500 companies came in roughly double what analysts had forecast. All 11 economic sectors posted positive earnings growth in the same quarter for the first time in four years—including healthcare and consumer discretionary, which many had written off on tariff and inflation concerns. Furthermore, the trailing 12-month profit margin reached a high not seen since 1990.

Figure 1. S&P 500 Companies are Keeping a Record Share of Sales as Profit

Past performance is no guarantee of future results. Source: Chartr using Bloomberg, data as of June 4, 2026.

Still, much of that profit growth came from AI-related infrastructure companies. Semiconductor stocks had their best quarter ever, extending an extraordinary start to the year driven by demand for AI equipment. Technology companies overall posted first-quarter earnings growth that was well above the rest, while growth outside of tech was solid but more modest. However, the margin for error is narrower going forward as expectations continue to rise. Companies across economic sectors that are harnessing AI to improve business outcomes may well be where the alpha lies in the second half of 2026. Diversified portfolios will be better positioned.

Momentum Risk: The Danger Is Real

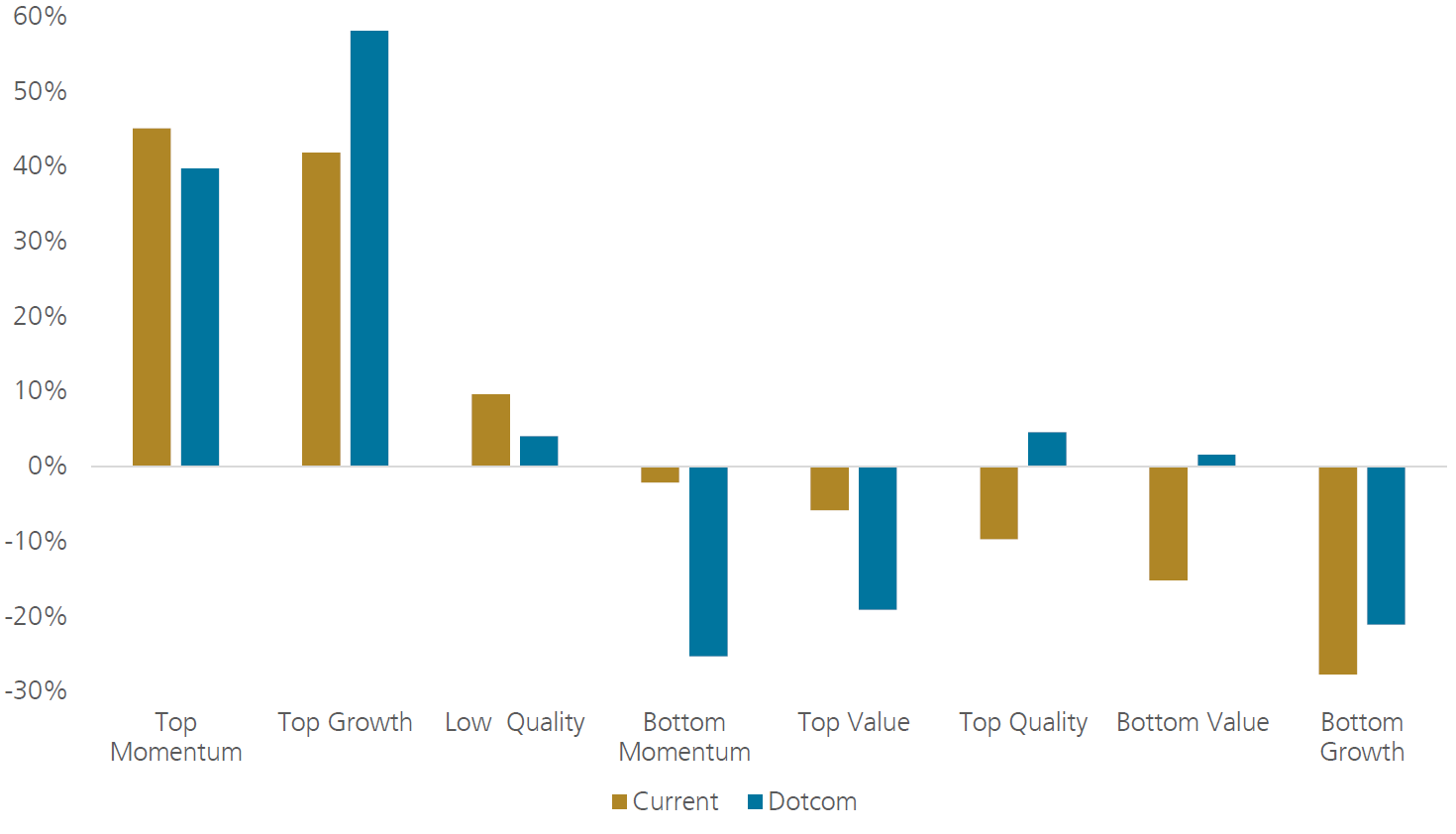

The S&P 500 Momentum Index has surged more than 30% year-to-date but has been punctuated by sharp reversals—including one of the worst two-day drawdowns since 2022. Hedge fund exposure to momentum ranks near five-year highs. When a single factor is that crowded, the unwinding tends to be disorderly.

Momentum strength and narrow breadth can persist, and they do not necessarily signal an imminent correction. But these imbalances always resolve—either through the rest of the market catching up or through the leaders giving back ground. Our emphasis on quality has historically paid off when momentum reverses, as it did following the dot-com bubble. Figure 2 shows how extreme the current cycle has been: since 2023, excess returns for US momentum stocks have exceeded those achieved during the dot-com era.

Figure 2. US Excess Returns, 1998 to March of 2003 versus 2023 to present

Past performance is no guarantee of future results. Source: “HOLT Global Viewpoint,” June 12, 2026, UBS Global Research, Michel Lerner, CFA using UBS HOLT, market-cap weighted returns, US Top 1000.

Portfolio Positioning: A Balancing Pole for the Tightrope Market

In a tightrope market, discipline matters. SROIX’s diversified portfolio emphasizes earnings quality, balance sheet strength, and reasonable valuations across sectors and geographies. Quality stocks remain attractively priced relative to history, even as the overall market trades at extended multiples. Fiscal expansion in Europe and corporate governance reform in Japan continue to support a broadening of returns beyond the US mega-cap story, and we are finding opportunities there alongside US equities.

Twenty-five-plus years of investing through different cycles has reinforced a consistent lesson: narrow, momentum-driven markets eventually give way to broader participation, and companies with durable competitive advantages and strong balance sheets tend to be the ones left standing when that rotation comes. We are well positioned for that outcome.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations.

Indexes are unmanaged, do not include fees or expenses, and are not available for direct investment. The S&P 500 Index is a measure of large-cap US equity performance. The S&P 500 Momentum Index is designed to measure the performance of securities in the S&P 500 universe that exhibit persistence in their relative performance. Shiller CAPE Ratio: The S&P 500 price divided by the 10-year average of inflation-adjusted earnings.

Environmental, social and governance (ESG) is based on the premise of investing in companies that have good environmental records, are ethically run, and have a positive social impact.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Antetokounmpo Sustainable Equities Fund include equity securities risk consisting of market prices declining in general, growth stock risk consisting of potential increased volatility due to securities trading at higher multiples, large-capitalization stock risk, consisting of the possibility that large-cap stocks as a group could fall out of favor with the market, small and mid-sized company risk, sector risk, portfolio turnover risk, and portfolio selection risk.

The Fund's ESG policy could cause it to perform differently compared to similar funds that do not have such a policy. The application of the social and environmental standards of Calamos Advisors may affect the Fund's exposure to certain issuers, industries, sectors, and factors that may impact the relative financial performance of the Fund—positively or negatively—depending on whether such investments are in or out of favor.

Calamos Antetokounmpo Asset Management LLC (“CGAM”), an investment adviser registered with the SEC under the Investment Advisers Act of 1940, serves as the Fund’s adviser (“Adviser”). CGAM is jointly owned by Calamos Advisors LLC and Original C Fund, LLC, an entity whose voting rights are wholly owned by Original PE, LLC, which, in turn, is wholly owned by Giannis Sina Ugo Antetokounmpo. Giannis Sina Ugo Antetokounmpo is the majority shareholder of Original C, with a 68% ownership interest.

Mr. Antetokounmpo serves on the Adviser’s Board of Directors and has indirect control of half of the Adviser’s Board.

Mr. Antetokounmpo is not a portfolio manager of the Fund and will not be involved in the day-to-day management of the Fund’s investments, and neither Original C nor Mr. Antetokounmpo shall provide any “investment advice” to the Fund. Mr. Antetokounmpo provided input in selecting the initial strategy for the Fund.

Mr. Antetokounmpo will be involved with marketing efforts on behalf of the Adviser.

If Mr. Antetokounmpo is no longer involved with the Fund or the Adviser, then “Antetokounmpo” will be removed from the name of the Fund and the Adviser. Further, shareholders would be notified of any change in the name of the Fund or its strategy.

The Adviser is jointly owned and controlled by Calamos Advisors LLC and, indirectly, by Mr. Antetokounmpo, a well-known professional athlete. Unanticipated events, including, without limitation, death, adverse reputational events or business disputes, could result in Mr. Antetokounmpo no longer being associated or involved with the Adviser. Any such event could adversely impact the Fund and result in shareholders experiencing substantial losses.

026054f 0726