Investment Team Voices Home Page

Investment Team Voices Home Page

Ask for a Pony, Get a Ferrari: Good Times for Global Convertibles

July 1, 2026

Eli Pars, CFA

Summary Points:

- From knockout issuance to returns, the global convertible market delivered in a quarter what we’d be happy to see in a year.

- Calamos Global Convertible Fund (CXGCX) gained 14.5% for the quarter, outperforming the FTSE Global Convertible Index, up 13.8%, as well as the MSCI World Index, up 13.9%.

- We are finding many opportunities in the new issuance market to rebalance and lock in gains.

The second quarter saw plenty of ups and downs, but investors ultimately managed to shrug off whatever came their way, from war and geopolitics to the prospect of interest rates rising rather than falling under a new Federal Reserve chair. The global convertible market soared as investors cheered continued strength in corporate earnings, particularly in the AI complex, and a ceasefire agreement between the US and Iran, which boosted expectations that inflation would fall alongside energy prices.

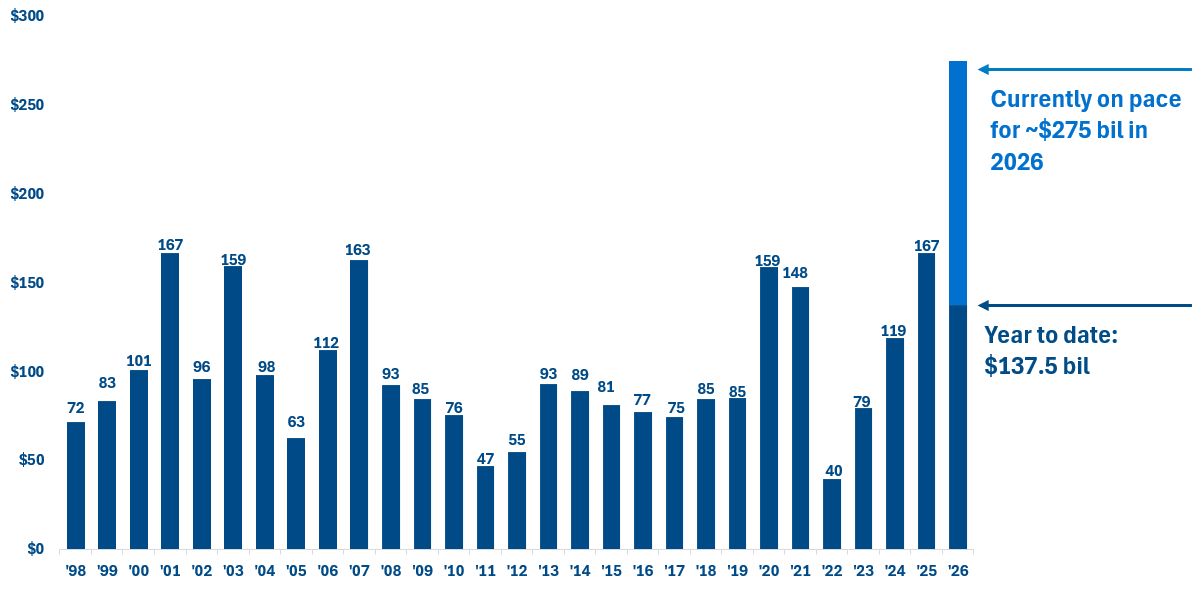

The quarter brought record-breaking levels of new convertible issuance. Alphabet—a first-time issuer—led the way with a $19.3 billion mandatory convertible issue, the largest on record. While Alphabet’s monster deal may have grabbed most of the headlines, it was just one of a flurry of companies to seek growth capital from the convertible market. When all was said and done, companies around the world issued $83.6 billion during the quarter, bringing year-to-date totals to $137.5 billion. For perspective, this half-year total already surpasses the calendar year totals of all but six of the past 28 years.

Growth Capital for Growth Companies: Booming Issuance in Global Convertibles

Global convertible new issuance ($ bil)

Source: BofA Global Research, Calamos. Year to date through 6/30/2026.

This issuance environment gave us plenty of opportunities. This included leaning into the new issuance market to sell in-the-money paper and buy at-the-money paper. But we’re also being selective about company fundamentals and conscious of position size. As we’ve discussed in the past, convertibles vary in their levels of equity sensitivity and fixed-income sensitivity. The greater the equity sensitivity, the greater the convertible’s exposure to both the upside and downside of its underlying equities. Mandatory convertibles—like Alphabet’s—are a different animal than traditional convertible bonds. They tend to be more equity-like, so we factor this into our overall portfolio construction process. But understanding these sorts of trade-offs is our bread and butter, and we believe our experience makes the difference.

Our overall allocations reflect our bottom-up focus—in other words, it’s always about finding good names with good structures. Information technology companies make up roughly one-third of the portfolio as of quarter-end (slightly less than the benchmark weight), followed by consumer discretionary at about one-fifth (a significant overweight), with industrials and health care next. Regionally, US issues make up about two-thirds of the fund, followed by Emerging Asia at about one-sixth.

Where to from here?

We see many positives on the horizon. We’re optimistic about the issuance momentum in the market; as we’ve discussed in the past, there tends to be a “follow-the-leader” theme in convertible issuance, and the decision of mega-caps like Alphabet and Oracle to issue convertibles could be a powerful catalyst for other large-cap companies to follow suit, further enhancing the diversity of the market as a whole. We’re optimistic about many of the convertible structures in the market today.

Still, we’re being prudent. The endgame of the war with Iran isn’t obvious, US midterms will contribute to investor anxiety, and we expect the newsfeed to continue whipsawing investors as it has over recent months. We’re also aware that we could already be in a late-cycle environment, and it’s essential to have the right risk-reward ahead of a turn.

Not every quarter will be like this second quarter, but as active, experienced managers, we don’t need a shoot-the-lights-out market to be optimistic about what’s ahead for Calamos Global Convertible Fund.

| Total Return % as of 6/30/26 | 2Q26 | 1 Year | 3 Year | 5 Year | 10 Year | Fund Inception |

|---|---|---|---|---|---|---|

| Calamos Global Convertible Fund (CXGCX) | 14.47 | 24.96 | 16.34 | 5.31 | 9.44 | 8.04 (12/31/14) |

| FTSE Global Convertibles Index | 13.82 | 28.75 | 17.77 | 6.70 | 9.79 | 8.30 |

Source: Morningstar. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The funds’ gross expense ratio as of the prospectus dated 2/27/2026 is 1.08% for Class I Shares.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee a profit or protect against a loss.

Indexes are unmanaged, do not include fees or expenses, and are not available for direct investment. The FTSE Global Convertible Index is designed to broadly represent the global convertible bond market. The MSCI World Index measures the performance of developed market equities.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Global Convertible Fund include equity securities risk consisting of market prices declining in general, growth stock risk consisting of potential increased volatility due to securities trading at higher multiples, foreign securities risk, emerging markets risk, currency risk, geographic concentration risk, American depository receipts, midsize company risk, small company risk, portfolio turnover risk and portfolio selection risk.

Foreign security risk. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

026054i 0726