What a fascinating year for liquid alts!

U.S. equities started 2017 high and just climbed higher, undeterred by volatility that was at an all-time low.

Nonetheless—as demonstrated by the flows and performance tracked by our weekly Calamos Alternatives Snapshot—financial advisors and investors found a use for alternative mutual funds in 2017.

The 2017 year-end issue of our weekly Calamos Alternatives Snapshot shows:

- In flows-gathering, it was the Energy Limited Partnerships category—one of just two categories that produced negative returns for the year—that led the most number of weeks (13).

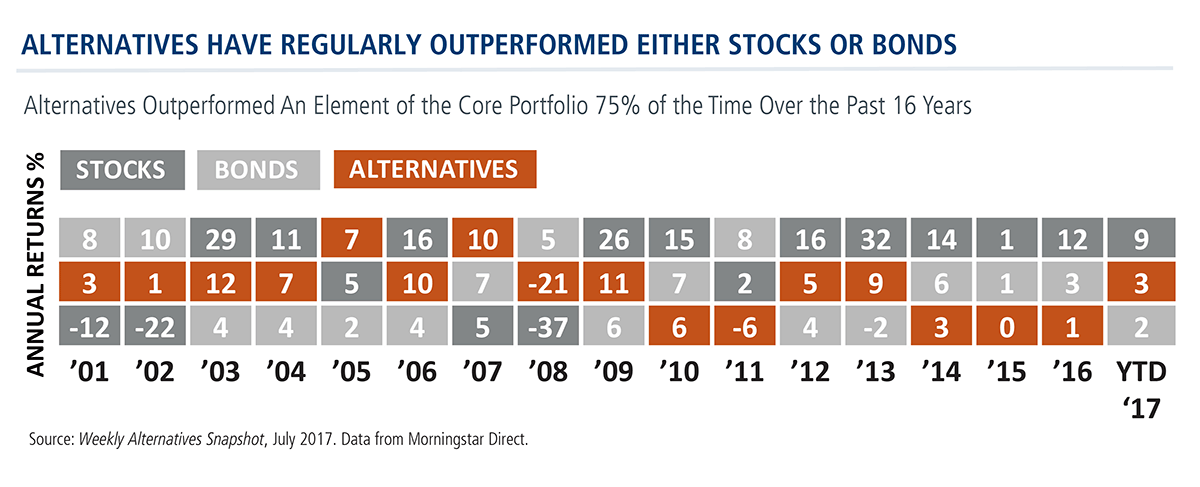

- In terms of performance, the Precious Metals category led half of the year (26 weeks), followed by Convertibles (17 weeks). However, Convertibles finished 2017 on top with a return of 12.50%, followed by Precious Metals whose return was 11.20%. Compare these to the S&P 500 return of 21.83% and the 3.54% return of the Bloomberg Barclays Capital U.S. Aggregate Bond Index.

Subscribe here to start your own weekly subscription.

Before we close the door once and for all on 2017, here’s a look at some themes the Snapshot followed throughout the year

Alts as an Alternative to the 60/40 Portfolio

We covered Alts vs. 60/40 every which way:

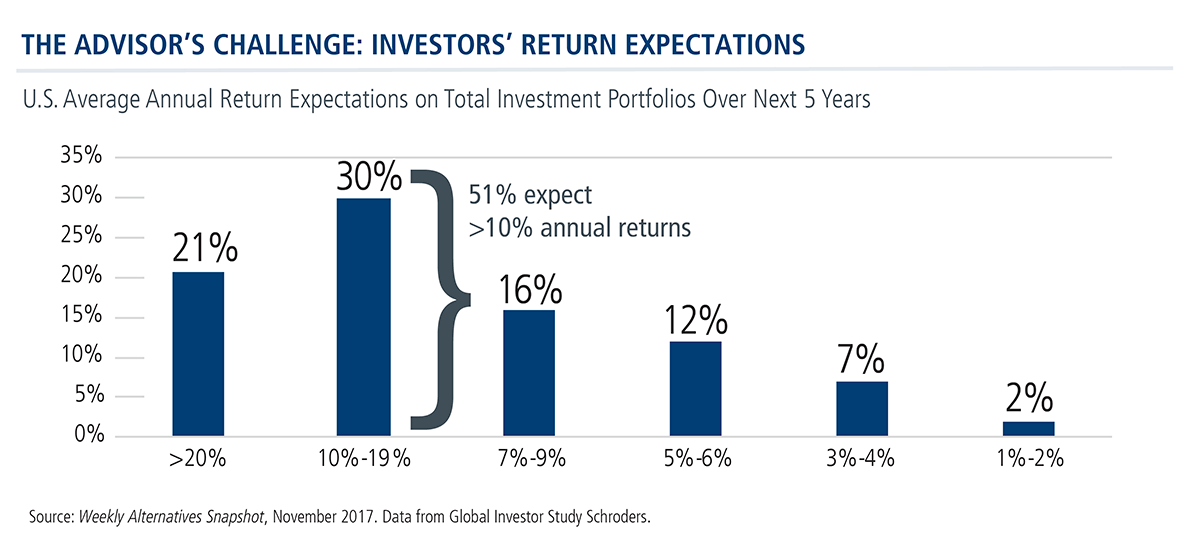

- Starting on January 16, there was the warning: “Investors looking at returns of a passive, traditional portfolio over the past 35 years [from a starting point when assets were cheap] as a benchmark for expectations going forward should adjust for ‘multiple expansion.’”

- “60/40 has been subject to distinct cycles, linked as it is to investment cycles,” our March 6 Snapshot reported. Peaks of value such as has recently been experienced are followed by “troughs of disappointment.”

- “One out of two financial advisors lacks confidence that the traditional 60/40 stocks/bonds portfolio can provide the returns it has historically. More than one in three (36%) have doubts that it will and 14% are neutral,” was our June 5 report on Financial Planning Association survey results.

- Recency bias is favoring the 60/40 portfolio, we reported on November 20—however, the combination has worked just 16 of the last 44 years, or 36% of the time. This is according to a Disciplined Systematic Global Macro Views blog post.

The Case for Alts in a Low Vol Year

Alternatives, of course, seek to provide diversification and minimize drawdowns that result from volatility—a solution that had no immediate problem to solve in 2017. Volatility was a favorite Snapshot topic, nevertheless:

- Long-only mutual funds trying to keep up with their benchmarks “are sitting on some of the most aggressive bets in three years,” according to a Bloomberg story we reported on August 14. Mutual fund exposure to the S&P 500 the past three months was higher than 90% of the time since 2014, according to the Morgan Stanley data. Net leverage at long/short funds, on the other hand, was near historic lows—in the 17th percentile since 2005.

- “Too much equity risk too soon could burn young investors” was the headline on our September 11 report. While younger investors may have a higher capacity to take on risk, they generally don’t have the appetite for it. The default 90% stocks/10% fixed income retirement plan allocation is at odds with the stated preference of the vast majority of younger investors, according to Cerulli Associates research.

- There’s a distinction between the impact of index volatility (missing in action in 2017) and sector and individual stock volatility, we reported on June 26. “Because convertible arbitrage strategy relies on the volatility of individual stocks—some of which have continued to experience large moves—trading opportunities and price dislocations are still available.” But, as explained in a Calamos post about the Calamos market neutral strategy, lower index volatility has prompted a shift in covered call (collared) strategy.

Awareness/Usage of Liquid Alts

Are liquid alts mainstream yet? Alternative funds are still novel enough that surveys continued to be conducted to test awareness, and we reported on many of them:

- Six out of 10 investors (62%) surveyed by Natixis think it’s essential to invest in alternatives to reduce investment risk. However, seven out of 10 (71%) say alternatives are risky and two-thirds (63%) say alts are “too complicated.” This is from our October 23 report.

- Clients’ lack of understanding continues to be a “key impediment” to an alternatives allocation, advisors said in an InvestmentNews/Blackstone survey we reported on March 20.

- Wirehouse advisor average allocations to alternatives overall hover around 5%. That’s far less than firm-set targets ranging from 10% to 20% of high net worth investor portfolios (our May 22 report). Two-thirds (68%) of endowments and foundations have more than 10% of their portfolios allocated to alts, per our August 28 news item.

Consolidation of Liquid Alts

The composition of the liquid alts industry evolved over the year. Fund providers continued to innovate, with launches (92 in the year) edging out closures (88). Also:

- A January 23 news item noted that the top 25 alternative mutual funds make up more than half (58%) of the overall assets under management of the 395 alternative funds tracked by Morningstar Direct.

- Alternatives dominated the list of Lipper categories with the greatest number of funds liquidated or merged, we reported July 10.

- Our November 27 item reported that “A good three-year track record is the minimum expectation of a liquid alternative fund—and funds that lacked them in recent years were liquidated or merged shortly after their third birthday.”

- One announcement made in April had yet to materialize by the year’s end: Morningstar’s intention to launch its own alternative fund.

The Weekly Alternatives Snapshot reflects Calamos’ commitment to the alts space. Calamos is the eighth largest alternatives manager by assets under management (Morningstar data, 9/30/17). Financial advisors, to learn more about our alternative funds, please talk to your Calamos Investment Consultant at 888-571-2567 or email caminfo@calamos.com.