Investment Ideas Home Page

An Institutional-Style Private Credit Portfolio

September 26, 2023

Calamos Aksia Alternative Credit and Income Fund (CAPIX)

The CAPIX team has constructed a private credit portfolio with broad, diverse representation across the private credit spectrum, putting investor capital to work in what we consider an opportune environment.

Through this carefully sourced and selected portfolio we have achieved:

- Critical mass and growing

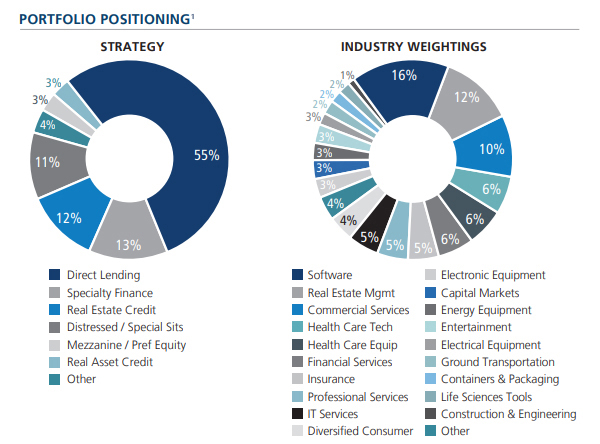

Currently net assets are $33.1M1.

- Diversification across private credit types

Invested across the full range of private credit strategies, deal types and collateral.

- Exposure across industries

Broad representation across multiple, noncorrelated sectors, deal types and collateral.

- High quality deal sourcing

Sourced and committed to opportunities from 20+ leading private credit partners and private equity sponsors.

- Focus on new vintage loans

Rather than accelerating investment through purchasing syndicated loans in the secondary market, emphasis on directly orginated, new vintage loans.

1Data as of 8/31/23. Percentages are based on invested portfolio and are subject to change. Other includes investments that do not have a strategy or industry classification.

Deal Highlights

- Closed Deal: Bilateral “Regulatory Capital” Transaction (Strategy Type: Specialty Finance)

$120 million private credit-linked note issued to a multinational investment grade bank with $500+ billion of assets and secured by a $2 billion portfolio of private fund subscription facilities. This note yields approximately 12% and was sourced by Aksia from a leading structured credit manager with over $7.5 billion in AUM. Aksia has extensive knowledge of and experience with this manager, enabling an early look at this opportunity.

- Closed Deal: Bilateral “Regulatory Capital” Transaction (Strategy Type: Specialty Finance)

$275 million 1st lien term loan (less than 25% LTV) to support the acquisition of a provider of healthcare software. The acquired business generates more than $60 million adjusted EBITDA and has more than 42,000 healthcare clients. Aksia sourced the investment directly from the private equity sponsor.

- Closed Deal: Private equity “NAV Loan” (Strategy Type: Specialty Finance)

$70 million NAV loan backed by $170 million in commitments to prominent global investment firm with more than $10 billion in AUM seeking balance sheet liquidity. Aksia sourced the deal from a specialist private credit manager active in the NAV lending market.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

The Fund has been organized as a closed-end management investment company. Closed-end funds differ from open-end management investment companies (commonly known as mutual funds) because investors in a closed-end fund do not have the right to redeem their shares on a daily basis. Unlike most closed-end funds, which typically list their shares on a securities exchange, the Fund does not currently intend to list the shares for trading on any securities exchange, and the Fund does not expect any secondary market to develop for the shares in the foreseeable future. Therefore, an investment in the Fund, unlike an investment in a typical closed-end fund, is not a liquid investment.

The Fund is designed primarily for long-term investors and not as a trading vehicle. The Fund is an “interval fund” pursuant to which it, subject to applicable law, will conduct quarterly repurchase offers for between 5% and 25% of the Fund’s outstanding shares at net asset value (NAV). Under normal market conditions, the Fund currently intends to offer to repurchase 5% of its outstanding shares at NAV on a quarterly basis. In connection with any given repurchase offer, it is possible that a repurchase offer may be oversubscribed, with the result that Fund shareholders (“Shareholders”) may only be able to have a portion of their shares repurchased. Even though the Fund will make quarterly repurchase offers to repurchase a portion of the shares to try to provide liquidity to Shareholders, you should consider the shares to have limited liquidity.

Risk Factors: General Economic Conditions and Recent Events. Difficult global credit market conditions have adversely affected the market values of equity, fixed-income, hard assets, and other securities and these circumstances may continue or even deteriorate further. The short- and longer-term impact of these events is uncertain, but could have a material effect on general economic conditions, consumer and business confidence and market liquidity. Investments made by the Fund are expected to be sensitive to the performance of the overall economy.

Direct Lending. The Fund will invest in directly originated senior secured loans, including unitranche loans, of performing middle market companies. The value of the Fund’s assets

is volatile and may fluctuate due to a variety of factors that are inherently difficult to predict and are outside the control of the Advisor and Sub-Advisors, including prevailing credit spreads, general economic conditions, financial market conditions, domestic or international economic or political events, developments or trends in any particular industry, changes in interest rates, or the financial condition of the obligors of the Fund’s assets.

Direct Origination. A significant portion of the Fund’s investments may be originated. The results of the Fund’s operations depend on several factors, including the availability of opportunities for the origination or acquisition of target investments, the level and volatility of interest rates, the availability of adequate short and long-term financing, conditions in the financial markets and economic conditions. Further, the Fund’s inability to raise capital and the risk of portfolio company defaults may materially and adversely affect the Fund’s investment originations, business, liquidity, financial condition, results of operations and its ability to make distributions to its Shareholders.

Loans. Loan interests generally are subject to restrictions on transfer, and the Fund may be unable to sell loan interests at a time when it may otherwise be desirable to do so or may be able to sell them only at prices that are less than what the Fund regards as their fair market value. Accordingly, loan interests may at times be illiquid. Loan interests may be difficult to value and may have extended settlement periods, which expose the Fund to the risk that the receipt of principal and interest payments may be delayed until the loan interest settles.

Secured Debt. Secured debt holds the most senior position in the capital structure of a borrower. Secured debt in most circumstances is fully collateralized by assets of the borrower. However, there is a risk that the collateral securing the Fund’s loans may decrease in value over time, may be difficult to sell in a timely manner, may be difficult to appraise, and may fluctuate in value based upon the success of the business and market conditions, including as a result of the inability of the borrower to raise additional capital. Also, substantial increases in interest rates may cause an increase in loan defaults as borrowers may lack resources to meet higher debt service requirements.

High Yield, Low-Rated or Unrated Securities. Debt securities (including bonds) and preferred stock in which the Fund invests may or may not be rated by credit rating agencies. The values of lower-rated securities (including unrated securities of comparable quality) fluctuate more than those of higher-rated securities because investors generally believe that there are greater risks associated with them. The inability (or perceived inability) of issuers to make timely payment of interest and principal would likely make the values of the securities more volatile and could limit the purchaser’s ability to sell the securities at prices approximating the values it had placed on the securities. In general, the market for lower-rated or unrated securities is smaller and less active than that for higher-rated securities, which can adversely affect the ability to sell these securities at favorable prices. In addition, the market prices of lower-rated securities are likely to be more volatile because: (i) an economic downturn or increased interest rates may have a more significant effect on the yield, price and potential for default; (ii) past legislation has limited (and future legislation may further limit) investment by certain institutions in lower-rated securities or the tax deductibility of the interest by the issuer, which may adversely affect the value of the securities; and (iii) it may be difficult to obtain information about financially or operationally troubled issuers. The Fund will not necessarily dispose of a security when its rating is reduced below its rating at the time of purchase.

Unsecured Loans. The Fund may make unsecured loans to borrowers, meaning that such loans will not benefit from any interest in collateral of such borrowers. Liens on such a borrower’s collateral, if any, will secure the borrower’s obligations under its outstanding secured debt and may secure certain future debt that is permitted to be incurred by the borrower under its secured loan agreements. The holders of obligations secured by such liens will generally control the liquidation of, and be entitled to receive proceeds from, any realization of such collateral to repay their obligations in full before the Fund. In addition, the value of such collateral in the event of liquidation will depend on market and economic conditions, the availability of buyers and other factors. There can be no assurance that the proceeds, if any, from sales of such collateral would be sufficient to satisfy the Fund’s unsecured loan obligations after payment in full of all secured loan obligations. If such proceeds were not sufficient to repay the outstanding secured loan obligations, then the Fund’s unsecured claims generally would rank equally with the unpaid portion of such secured creditors’ claims against the borrower’s remaining assets, if any.

822133 0823