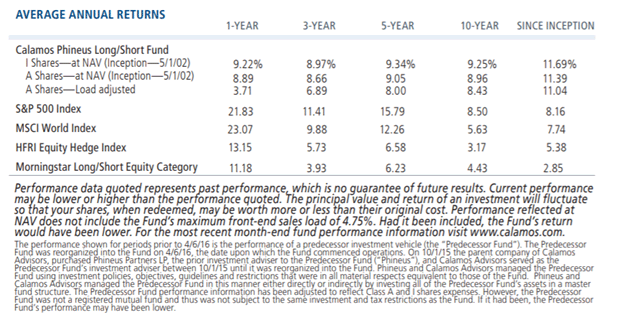

“If the message of 2017 was ‘growth without inflation,’ 2018 looks vulnerable as this favorable tradeoff is bound to deteriorate through 2018...We forecast a 5% to 10% drawdown in the major markets in the next six months, largely driven by concern over higher interest rates.”

These lines in the Q4 2017 commentary of Calamos Phineus Long/Short Fund (CPLIX) explain how the fund was positioned at the start of the year—and the fund’s performance over the last week.

(While the time period is too short for us to cite here, we encourage advisors to research CPLIX on your favorite data provider site. The actively managed long/short equity fund is doing what advisors need it to do for their clients. For additional insight, see the difference in CPLIX’s correlation to the S&P 500 versus other funds in the Morningstar Long/Short Equity Funds category.)

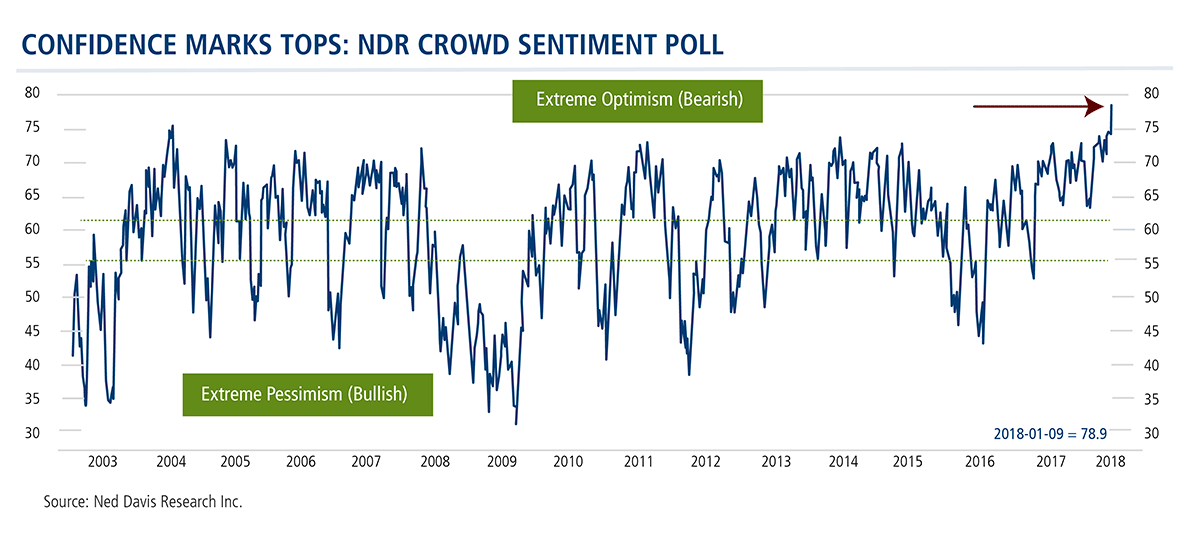

January was a month when investors shouted “just get me in,” says Co-CIO and Senior Portfolio Manager Michael Grant. “These types of over-excited price moves rarely end quietly. Part of our role, as hedged managers, is to lean against this kind of risk, which is why our net exposures moved to the lower end of our range.”

Grant presented the below chart at a meeting in January, saying, “This is a sentiment measure slide that I’ve followed for 30+ years. Whenever it gets to an extreme, you want to lean against the wind.” He specifically pointed to momentum-driven passive money as responsible for extending the euphoria. The reversal of passive flows adds additional uncertainty to the outlook.

A Turning Point

With the market of the last few days validating his earlier concerns, Grant says, “It’s no longer just about earnings, but earnings and interest rates.” This is a new paradigm for investors because prior market stress since 2008 has always been led by deflation.

“The bond proxies will no longer work as defensive havens,” he says.

Last year marked the climax for financial conditions in the U.S., according to Grant. Equities can still “win” this year but not as easily as in 2017. He continues to think of 2018 as “a topping year” and one likely to frequently test its major moving averages. While not necessarily a negative, “it certainly changes the character of the progression of equities.”

The portfolio manager believes that price multiples for leading U.S. equity indices may have peaked, due to a higher cost of debt. Grant calls the yield breakout of long-dated Treasuries a leading indicator of a major turning point for the volatility of all major financial assets. For the first time since 2008, he says, “the return of genuinely normal monetary conditions is a credible prospect.”

Because the cost of debt has been more influential in this investment cycle than the cost of equity, equities will be highly sensitive to changes in the Federal Reserve outlook. Watch the March Fed meeting for signs of an inflection, suggests Grant.

Ultimately A Buyer

Grant expects this extended consolidation with rising volatility to dominate markets in coming months. “Our ultimate objective is to buy this move once the passive excesses have run their course,” he says, because this is not yet “end of cycle.” As Grant highlighted in early January, 2018 can be described as late-cycle for equities, but that is not the same as “end of cycle.”

The key is what to buy once the dust settles. Grant believes that early 2018 is as good as it gets for a range of cyclical sectors. “It is time to shift away from the industrial part of the economy, back to the consumer,” he notes. Grant remains positive on the financials sector as the fund’s primary cyclical play.

Many still want to buy the defensive and consumer staples stocks after periods of uncertainty, but this will be a mistake, according to Grant.

“There is no new deflation risk on the horizon,” he says. Profit growth will continue into 2019, which is why this is not yet “end of cycle.” In the short term, he says “capital preservation is our focus, but investors should not assume that defensive stocks will outperform if deflation is no longer the enemy.”

Grant remains negative on China, which he views as more vulnerable to the return-to-normal of U.S. monetary policy. The symptoms of credit stress continue to rise in China.

For more on how CPLIX is being actively managed, watch these videos with Michael Grant. Financial advisors, for more information about CPLIX or Grant, talk to a Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.