This post was written by Joseph Wysocki, CFA, Senior Vice President, Co-Portfolio Manager.

The convertible bond market finished a solid 1Q18 (up 2.5% vs. a down S&P 500 and bond market). This performance, following a strong 2017, has led to many conversations about what drives the returns of the asset class.

Below we’ll review performance over both the short- and long-term. As you’ll see, it’s the composition of convertible issuers that drives short-term returns. But active management of multiple variables unique to converts is what results in long-term performance—and the value that the asset class can provide to an investment portfolio.

A Short-Term Review

In our 40 years of investing we have often said that it is not a “stock market,” but a market of stocks. The implication: There are many individual companies or sectors that can perform differently at different times.

The same is true for the convertible bond market—in the short term the most dominant factor is the performance of the underlying company. Let’s examine two separate periods: the first quarter of 2018 and the fourth quarter of 2015.

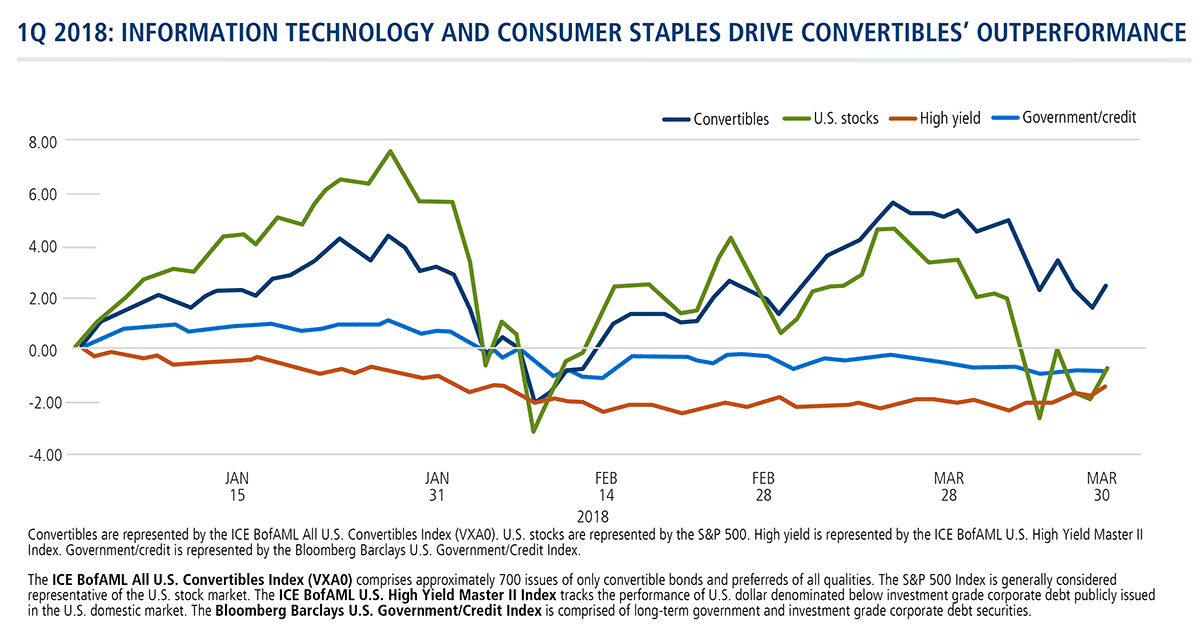

1Q18: Converts Beat S&P

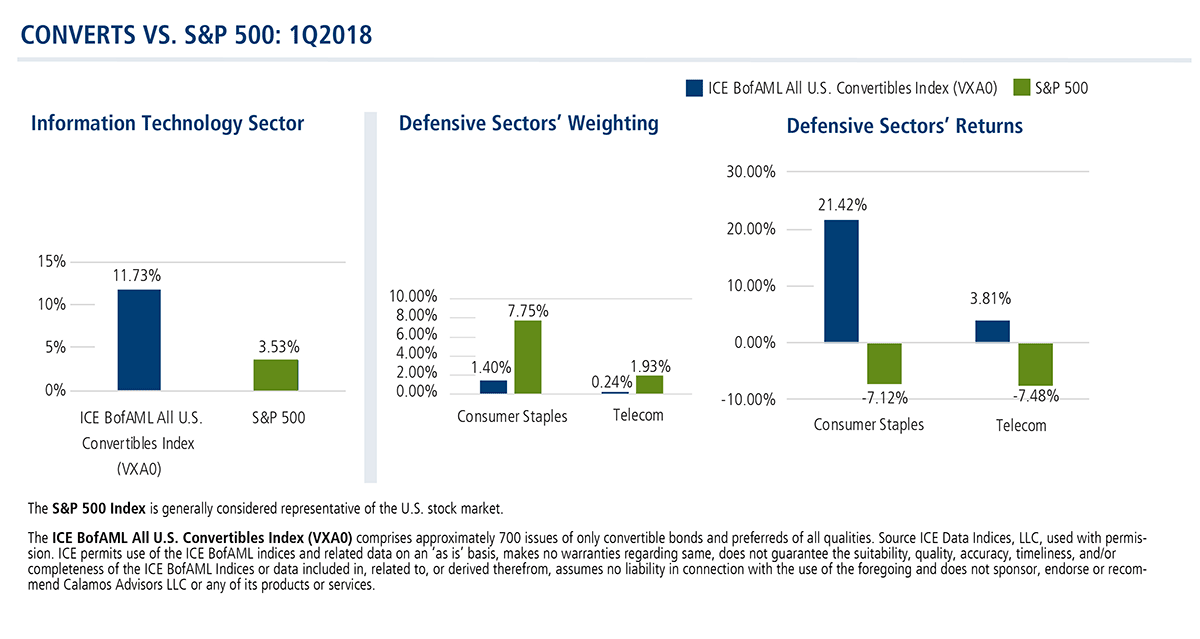

In this period, convertibles’ strong outperformance (as measured by the ICE BofAML All U.S. Convertibles Index [VXA0]) compared to the U.S. equity market ([S&P 500]) can be traced largely to two individual sectors: Information Technology and Consumer Staples.

Within the convert market, the issuers in the Technology sector saw an 11% gain in their equity price while the broader S&P tech sector was up only 3.5%. This was driven by convert issuers being more focused in the mid-cap growth area while the larger cap exposure was more heavily skewed toward semiconductor companies rather than the large internet names that comprised the S&P.

On the defensive front, the convertible market benefited from having a much smaller allocation to the Consumer Staples and Telecom sectors. This is typical as convertibles tend to be a source of “growth capital” not often used in these more mature sectors. But the sizeable underperformance of these defensive sectors in the broader S&P magnified the impact and drove a significant deviation in returns during the quarter.

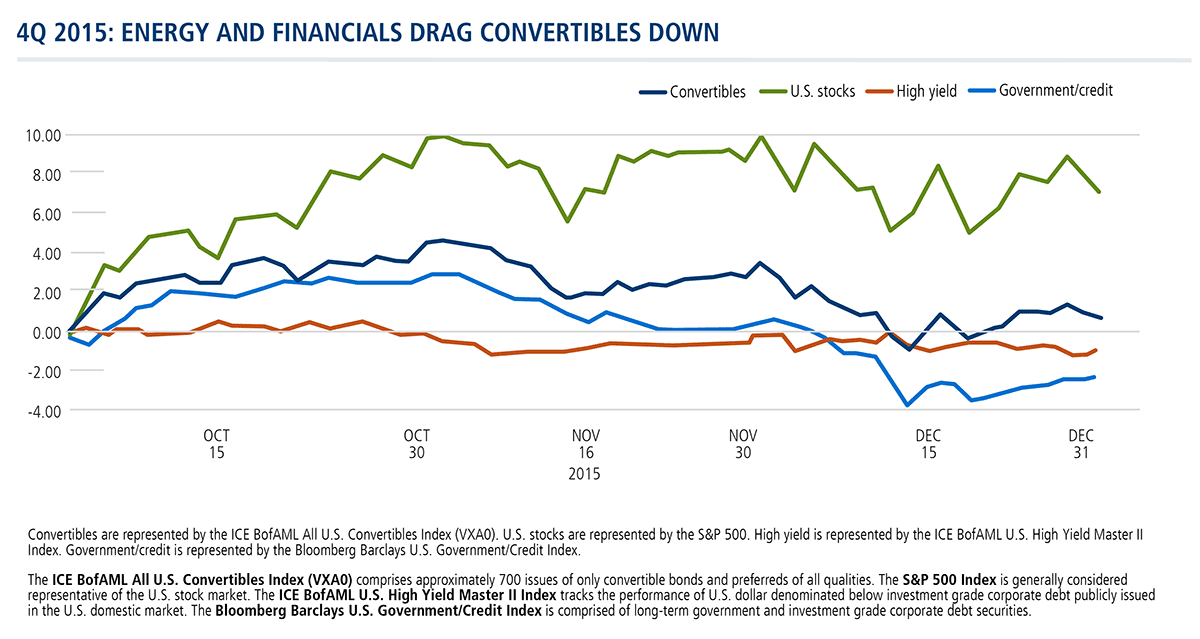

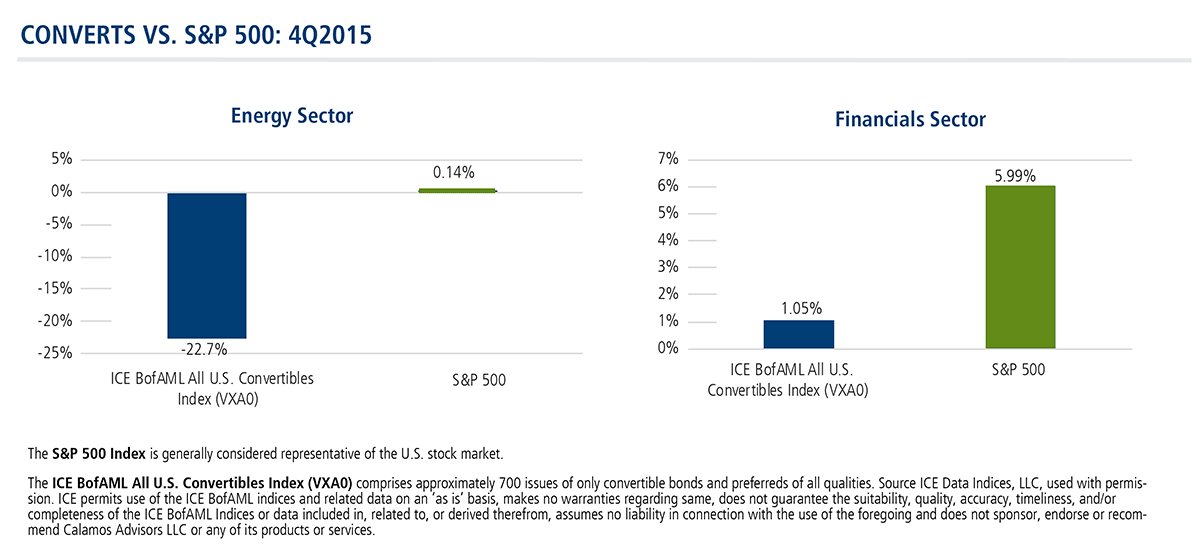

4Q2015: S&P Beats Converts

Such outperformance by converts doesn’t always happen. For example, let’s review an alternative scenario—4Q 2015.

In this period, the S&P outperformed convertibles due mostly to differences in some of the cyclical areas. The convertible Energy sector was -22% vs. a flat S&P Energy sector in part due to higher exposure to smaller cap, more highly levered companies. At the same time, the Financials sector in the convert market didn’t participate in a strong bank equity rally, largely due to the lower equity sensitivity of the convertible structures.

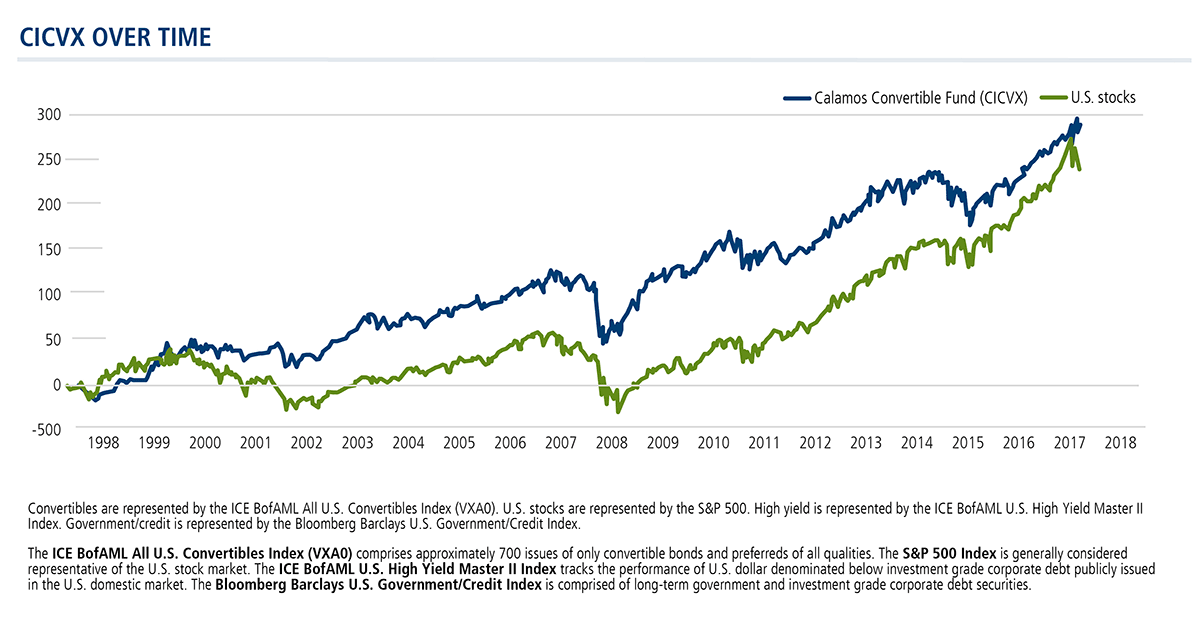

A Long-term Review

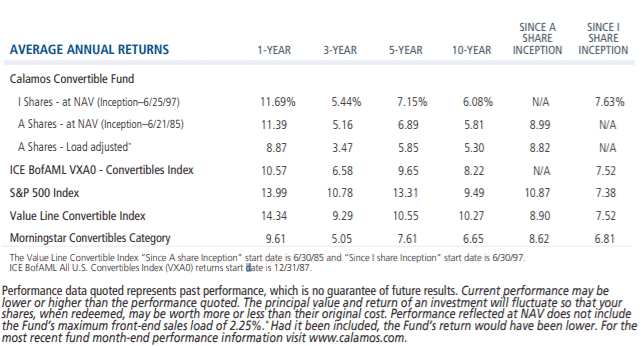

As you can see, the shorter term, quarter-to-quarter returns will vary but when one looks at the longer term performance, the potential benefits that the convertible asset class has historically provided are clear—outperformance of fixed-income in rising rate environments while also delivering equity market returns with lower volatility. Below you’ll see the long-term performance of Calamos Convertible Fund (CICVX) vs. the S&P 500.

One aspect of the convertible market that helps deliver these types of returns is the fact that convertibles have both equity and straight bond characteristics. This unique feature means that as the underlying equity appreciates, the convertibles delta—or equity sensitivity—increases along with it. But if the underlying equity declines, the convertible performs much more like a standard straight bond providing principal protection. Therefore, it is imperative that investors are fully versed in both equity and fixed income analysis as these characteristics can dramatically impact how a convertible performs.

As an example: financial advisors, would you have wanted your clients to own an all-equity portfolio right before the tech bubble burst? Did your clients belong in a pure bond portfolio at the depths of the recession? If you had bought just the convert market that is exactly what you would have owned at some of the most significant turning points in the market.

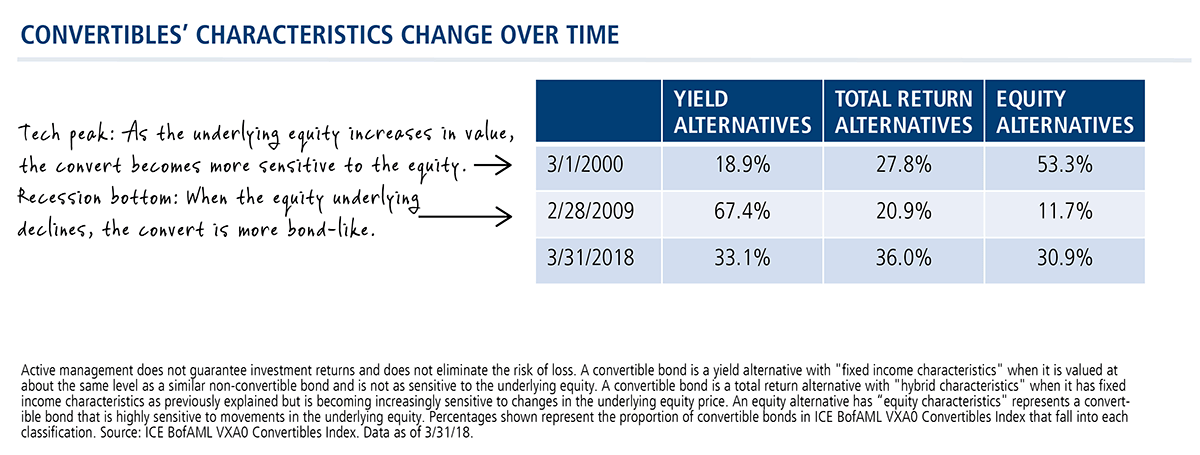

Another unique aspect of the convertible market is that the composition changes much more frequently than the broader equity market. The typical convertible bond is issued with a five-year life by a company in the early to mid-stages of their corporate life cycle, seeking capital to grow. Once this time has passed, the issuer often has matured to the point where it does not need convertibles in its capital structure as it can self-fund growth or access other lower cost alternatives.

This has the effect of keeping the convertible market in some of the freshest growth opportunities, but it also means that investors must have the expertise to evaluate the underlying economic exposures and allocate risk across a constantly changing opportunity set. For example, nearly two-thirds of the current convert issuers were not in the convert market 10 years ago while two-thirds of the S&P members remain unchanged.

Calamos Can Help

To achieve the long-term performance advantage of convertible securities—to participate in the majority of equity upside while building resilience against unforeseen downturns—requires active management capable of understanding the risks, evaluating each issuer’s capital structure and positioning an overall convertible portfolio.

As the firm whose founder (Chairman and Global CIO John P. Calamos, Sr.) pioneered the use of convertible securities to manage risk more than 40 years ago, we welcome opportunities to educate advisors about how convertibles perform and the role that active management necessarily plays.

Advisors, for information about convertibles or CICVX, please talk to your Calamos Investment Consultant at 888-571-2567 or email caminfo@calamos.com.