Capital preservation uncorrelated to equities—that’s the traditional purpose of the fixed income allocation.

But in the 2016 economic environment of historically low yields, low inflation, narrowing credit spreads, building volatility, and the expectation that the Fed will patiently raise rates just a few times over the next year, investors have shifted to lower quality funds for their attractive yields and protection against interest rate risk. This move into credit-sensitive fixed income adds additional risk to the portion of the asset allocation meant to serve as the ballast to equity volatility.

We’d urge caution about the associated risks with such reallocations. Adding alternatives that have similar characteristics to fixed income but protect against credit risk may be a better idea.

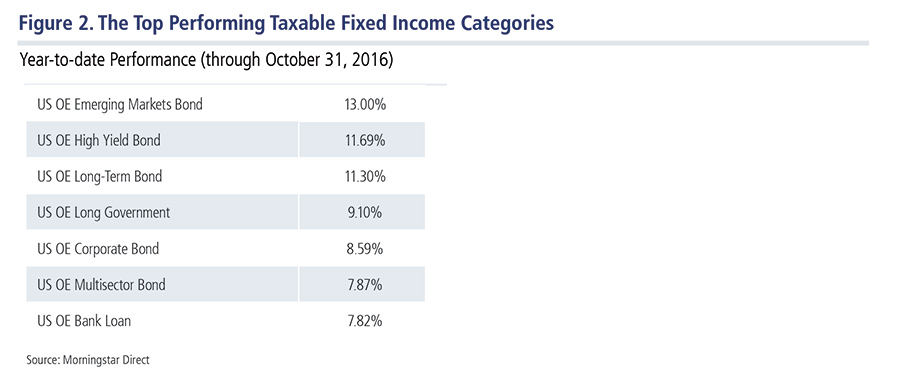

Bank Loan and High Yield Credit Fund Flows & Performance

Two categories that have received the majority of flows are bank loans, also known as leveraged loans, and high yield credit.

Thanks to strength early in the year, the High Yield Bond Morningstar category ranked fourth in the top 10 categories year-to-date for estimated net inflows, as of October 31, 2016.

The Bank Loan Morningstar category has been the second largest category receiving net inflows, behind intermediate-term bond funds and has reached its 14th consecutive week of positive flows as of November 4, 2016. Bank Loan funds have recently seen positive net flows as investors anticipate an increase in yield with the 3-month LIBOR quickly approaching the 1.0% floor level.

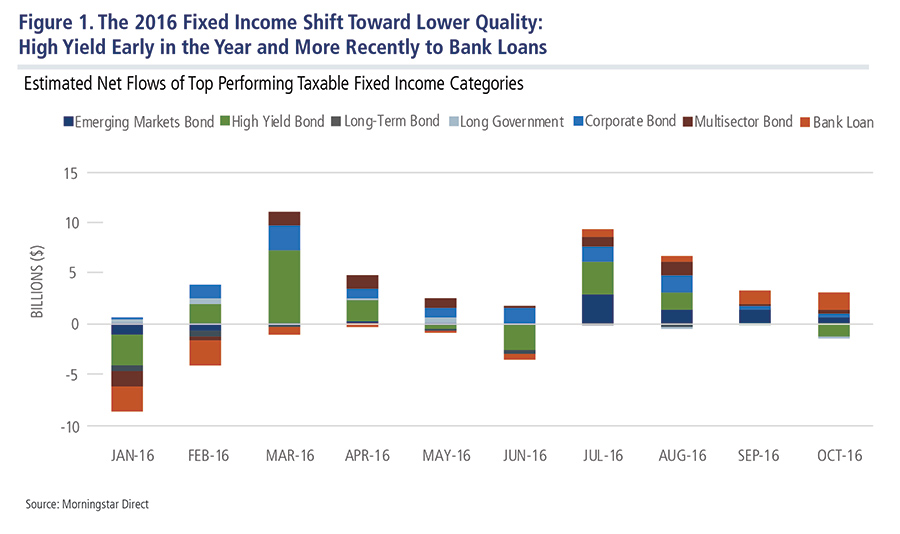

Morningstar research has often noted that category flows have a tendency to follow performance. Below are the top-performing taxable fixed income categories, all of which have outperformed the major equity markets year to date.

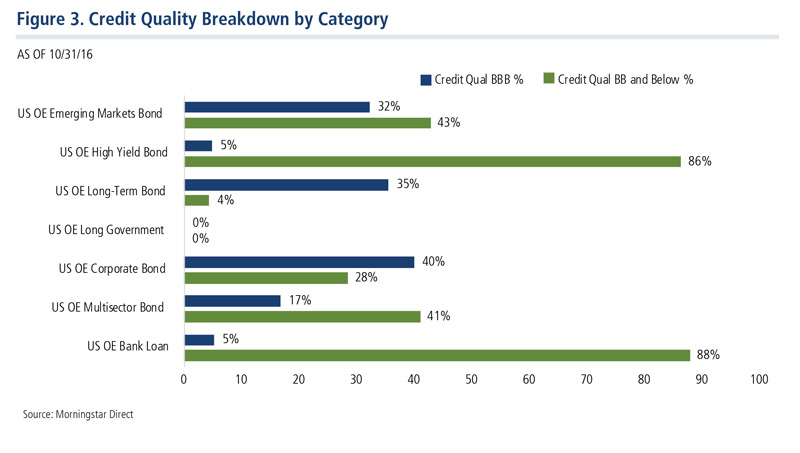

Credit Risk in Exchange for Return

As a reminder, credit risk is the primary risk that investors are being compensated for in bank loan, high yield and other nontraditional bond categories. Below is the credit quality breakdown of 2016’s top performing (and top flow-gathering) taxable bond categories.

The majority of these categories have substantial amounts allocated to below-investment grade credit. While these categories have provided strong returns to date, expectations are that fixed income will not perform as well going forward. Investors are attracted to these categories for their performance, attractive yields, and as a hedge against rising interest rates. What may be overlooked is that they may be increasing the risk of their entire portfolio.

More Correlated, More Volatile

Equity risk is the dominant risk in most investment portfolios. The traditional role of the fixed income allocation has been to provide capital preservation and portfolio stability. This portion of the portfolio is typically negatively correlated to equities and acts as the portfolio’s ballast during periods of market volatility. Although fixed income performance is often positive in times of crisis, it historically has not been enough to offset the drawdowns endured from the equity side of the allocation.

One of the hazards of shifting a fixed income allocation toward lower quality investments is that they are often more correlated with equities and can add greater—even if unrecognized—levels of volatility and potential drawdowns to the portfolio. This can ultimately defeat the purpose of fixed income in a portfolio.

High yield funds are often more volatile and have been considered equity-like alternatives due to similarities in their risk/return characteristics.

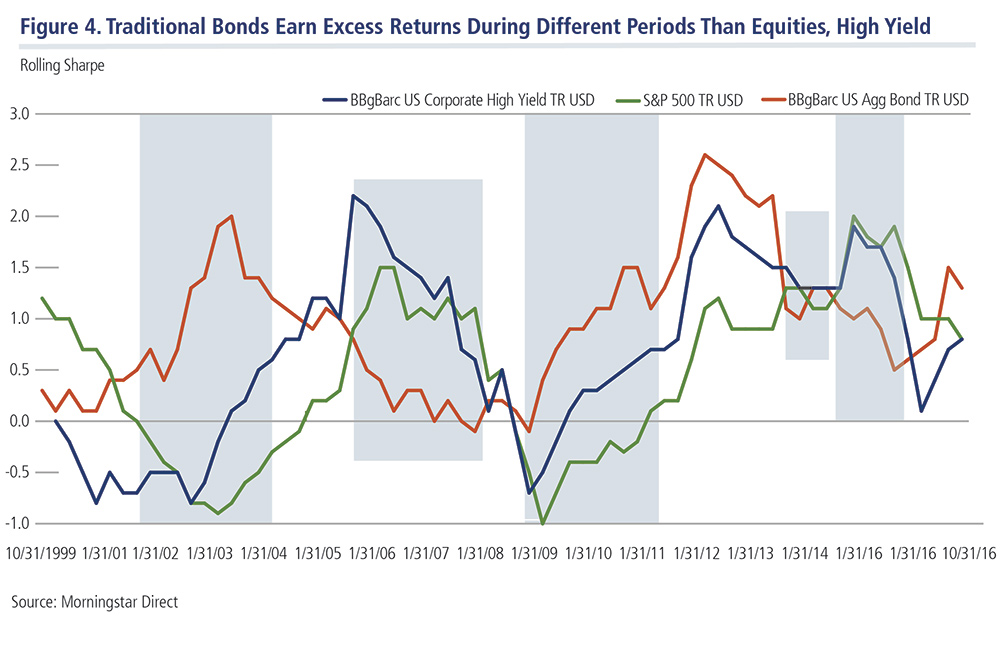

The rolling three-year Sharpe ratio, which is a risk-adjusted measure of excess returns, helps illustrate the point. The chart below shows that traditional bonds, as measured by the BBGBARC AGG, often earn their excess returns during different periods than equities, as measured by the Standard & Poor’s 500. What the chart also illustrates is that high yields, as illustrated by the BBGBARC US Corp HY Index, tend to earn their excess returns in line with equities. High yield’s frequent correlation with equities calls into question its ability to serve as a ballast (as traditional bonds would) when equity markets falter.

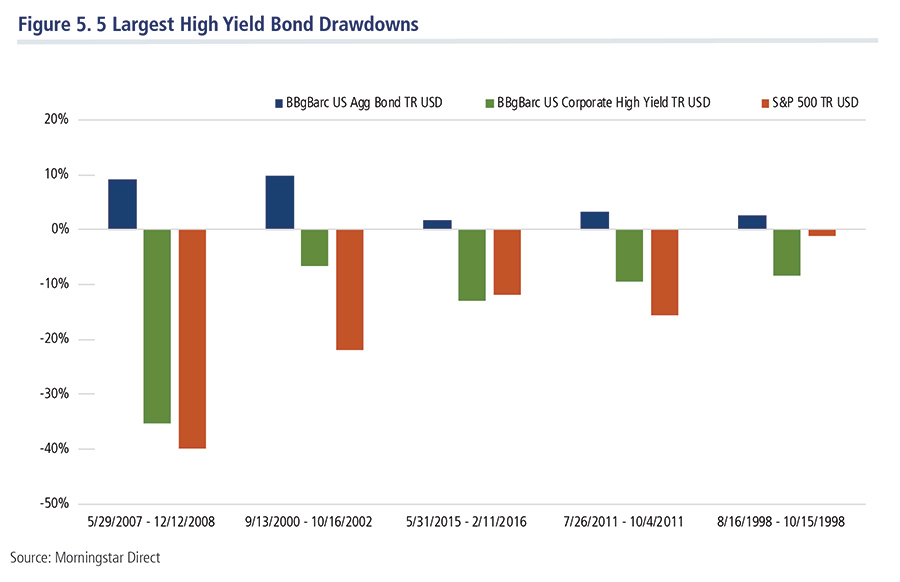

The Credit Crisis-Driven Drawdown

Investors are subject to portfolio drawdowns during both rising interest rate environments and during credit crises. The more severe drawdowns have occurred during credit crises, which have often been associated with equity market declines.

Of course, interest rate risk is a significant risk for many portfolios. Over the last 20 years, the largest drawdowns that the fixed income market (BCAGG) has experienced have been associated with periods of rising rates. Equities and credit sectors generally have performed well during these periods as rising rates typically coincide with an improving economy.

However, it is the drawdowns associated with credit (high yield) that have been significantly greater—and often correlated to equity drawdowns. The chart below illustrates that the five largest drawdowns experienced by high yield bonds in the last 20 years have been shared with drawdowns in the equity market. Portfolios whose fixed income allocations are heavily weighted in high yield will not have the benefit of stability, diversification or capital preservation.

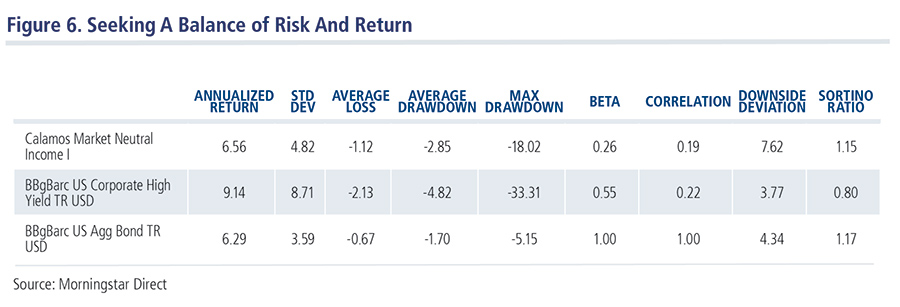

An Alternative: CMNIX

Advisors seeking an alternative to replace low-yielding traditional fixed income investments may want to consider alternative funds. Alternative funds make it possible to achieve similar outcomes as fixed income investments while potentially diversifying away the risks typically associated with the fixed income asset class.

Calamos Market Neutral Income Fund’s combination of its covered call and convertible arbitrage strategies historically has created a risk/return stream similar to an intermediate term bond fund without lowering the credit quality or adding unnecessary levels of volatility to a portfolio. Since its 1990 inception, the fund has provided:

- A consistent return stream similar to that of an intermediate term bond fund

- Protection during past periods of rising rates

- Lower volatility and drawdowns than high yield bonds

Advisors have more options than high yield and bank loan funds. Please talk to your Calamos Investment Consultant for more.

Advisors have more options than high yield and bank loan funds. Please talk to your Calamos Investment Consultant for more.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75% had it been included; the Fund’s return would have been lower. For the most recent month-end fund performance information visit

www.Calamos.com.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus. Alternative investments may not be suitable for all investors, and the risks of alternative investments vary based on the underlying strategies used. Many alternative investments are highly illiquid, meaning that you may not be able to sell your investment when you wish to.

Some of the risks associated with investing in alternatives may include hedging risk – hedging activities can reduce investment performance through added costs; derivative risk- derivatives may experience greater price volatility than the underlying securities; short sale risk - investments may incur a loss without limit as a result of a short sale if the market value of the security increases; interest rate risk – loss of value for income securities as interest rates rise; credit risk – risk of the borrower to miss payments; liquidity risk – low trading volume may lead to increased volatility in certain securities; non-US government obligation risk – non-US government obligations may be subject to increased credit risk; portfolio selection risk – investment managers may select securities that fare worse than the overall market. Alternative investments may not be suitable for all investors.

+ Morningstar ratings shown are for load-waived shares that do not include any front-end sales load. Not all investors have access to or may invest in the load-waived share class shown. Other share classes with front-end or back-end sales charges may have different ratings than the ratings shown. Additionally, some A-share mutual funds for which Morningstar calculates a load-waived A-share star rating may not waive their front-end sales load. There can be no assurance that the Fund(s) will achieve its investment objective.

Class I shares are offered primarily for direct investment by investors through certain tax-exempt retirement plans (including 401(k) plans, 457 plans, employer-sponsored 403(b) plans, profit sharing and money purchase pension plans, defined benefit plans and non-qualified deferred compensation plans) and by institutional clients, provided such plans or clients have assets of at least $1 million. Class I shares may also be offered to certain other entities or programs, including, but not limited to, investment companies, under certain circumstances.

The principal risks of investing in the Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

There are distinct differences between hypothetical performance results and the actual results subsequently achieved by a particular investment portfolio. No representation is being made that an account will or is likely to achieve profits or losses similar to those shown, and any investment may result in loss of principal.

As with any hypothetical illustration there can be additional unforeseen factors that cannot be accounted for within the illustrations included herein.

Hypothetical performance and index returns presented assume reinvestment of any and all earnings/distributions.

Some of the risks associated with investing in alternatives may include hedging risk – hedging activities can reduce investment performance through added costs; derivative risk- derivatives may experience greater price volatility than the underlying securities; short sale risk - investments may incur a loss without limit as a result of a short sale if the market value of the security increases; interest rate risk – loss of value for income securities as interest rates rise; credit risk – risk of the borrower to miss payments; liquidity risk – low trading volume may lead to increased volatility in certain securities; non-US government obligation risk – non-US government obligations may be subject to increased credit risk; portfolio selection risk – investment managers may select securities that fare worse than the overall market. Alternative investments may not be suitable for all investors.

Class I shares are offered primarily for direct investment by investors through certain tax-exempt retirement plans (including 401(k) plans, 457 plans, employer-sponsored 403(b) plans, profit sharing and money purchase pension plans, defined benefit plans and non-qualified deferred compensation plans) and by institutional clients, provided such plans or clients have assets of at least $1 million. Class I shares may also be offered to certain other entities or programs, including, but not limited to, investment companies, under certain circumstances.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

Covered Call Writing: As the writer of a covered call option on a security, the fund foregoes, during the option’s life, the opportunity to profit from increases in the market value of the security, covering the call option above the sum of the premium and the exercise price of the call.

Convertible Securities Risk: The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors also, may have an effect on the convertible security’s investment value.

Convertible Hedging Risk: If the market price of the underlying common stock increases above the conversion price on a convertible security, the price of the convertible security will increase. The fund’s increased liability on any outstanding short position would, in whole or in part, reduce this gain.

Convertible Securities Risk: The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors also may have an effect on the convertible security’s investment value.

Beta is a historic measure of a fund’s relative volatility, which is one of the measures of risk; a beta of 0.5 reflects 1/2 the market’s volatility as represented by the Fund’s primary benchmark, while a beta of 2.0 reflects twice the volatility.

Correlation is a statistical measure that shows how two securities move in relation to each other. A correlation of 1 implies that if one security moves up or down, the other security will move in lockstep, in the same direction. Alternatively, a correlation of 1 means that if one security moves in either direction, the other security will do the exact opposite.

Sharpe ratio is a measure of risk-adjusted performance, where higher values are indicative of better investment decisions rather than the result of taking on a higher level of risk. Sharpe ratio is calculated by the difference between a portfolio’s return and a risk-free rate, often that of the 10-year Treasury bond, and dividing the result by the portfolio’s standard deviation.

Standard Deviation measures the overall risk of a fund.

Upside Deviation measures only deviations above a specified benchmark.

Bloomberg Barclays U.S. Government/Credit Index comprises long-term government and investment grade corporate debt securities and is generally considered representative of the performance of the broad U.S. bond market. Unlike convertible bonds, U.S. Treasury bills are backed by the full faith and credit of the U.S. government and offer a guarantee as to the timely repayment of principal and interest.

The Barclays U.S. Aggregate Bond Index covers the U.S.- denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government-Related, Corporate, MBS (agency fixed-rate and hybrid ARM pass throughs), ABS, and CMBS sectors.

S&P 500 Index is generally considered representative of the U.S. stock market.

Citigroup 30-Day T-Bill Index is generally considered representative of the performance of short-term money market instruments. Morningstar Market Neutral Category represent funds that attempt to eliminate the risks of the market by holding 50% of assets in long positions in stocks and 50% of assets in short positions.

Morningstar Market Neutral Category represent funds that attempt to eliminate the risks of the market by holding 50% of assets in long positions in stocks and 50% of assets in short positions.

The Bloomberg Barclays US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody's, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded.