This post was written by Christian Brobst, Calamos Vice President, Portfolio Specialist.

The value-driven, bond-by-bond investment approach of the Calamos Fixed Income Team evaluates opportunities across company capital structures. Recently, we have been finding value in several companies’ bank loans, and this year have opportunistically added them to our portfolios either in combination with unsecured high yield bonds or instead of high yield bonds.

Given the building inflation pressure in the domestic economy, and an actively hiking Federal Reserve Board, bank loan coupon income may benefit as additional Fed hikes work into the system. Additionally, the senior position that bank loans enjoy in the capital structure can provide a volatility-dampening effect in times of credit spread volatility.

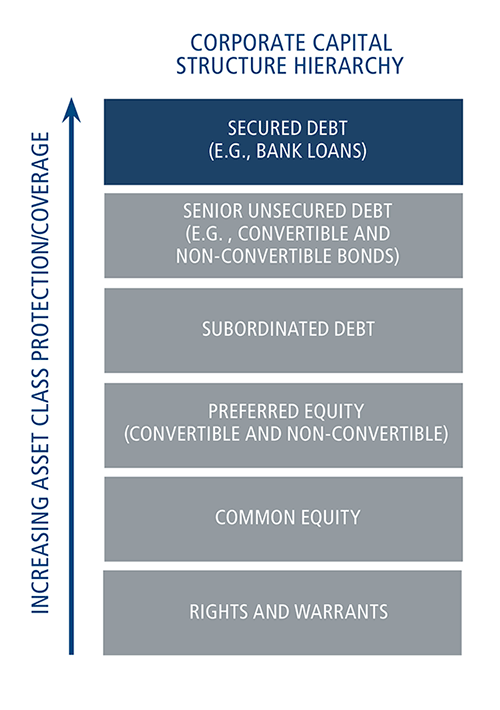

Bank loans have characteristics that differentiate them from other debt instruments in a company’s capital structure.

- Bank loans are floating-rate securities, and the coupons are reset quarterly at a set spread above three-month LIBOR.

- For companies that have unsecured bonds, bank loans are senior to unsecured obligations in the capital structure, meaning in the event of a default they receive principal ahead of bonds. Most companies (even in high yield ratings categories) never face an actual default scenario. Thanks to bank loans’ senior position in the capital structure, they exhibit less volatility than unsecured debt in times of heightened credit spread volatility.

How Bank Loans Seek to Protect Investors

Debt covenants included in bank loans are important sources of protection for investors, as lenders can seek instant repayment of the loan if a covenant is violated. Most often, violation of a covenant also comes with a fee penalty that an issuer must pay to lenders along with the opportunity to renegotiate loan terms.

There are typically two types of debt covenants. Incurrence covenants require the issuer to meet specified financial tests if the company wants to take a distinct action (examples would include paying an equity dividend or issuing additional debt). Maintenance covenants are more restrictive, compelling issuers to meet specified financial tests each quarter even if there is no specific action management would like to take.

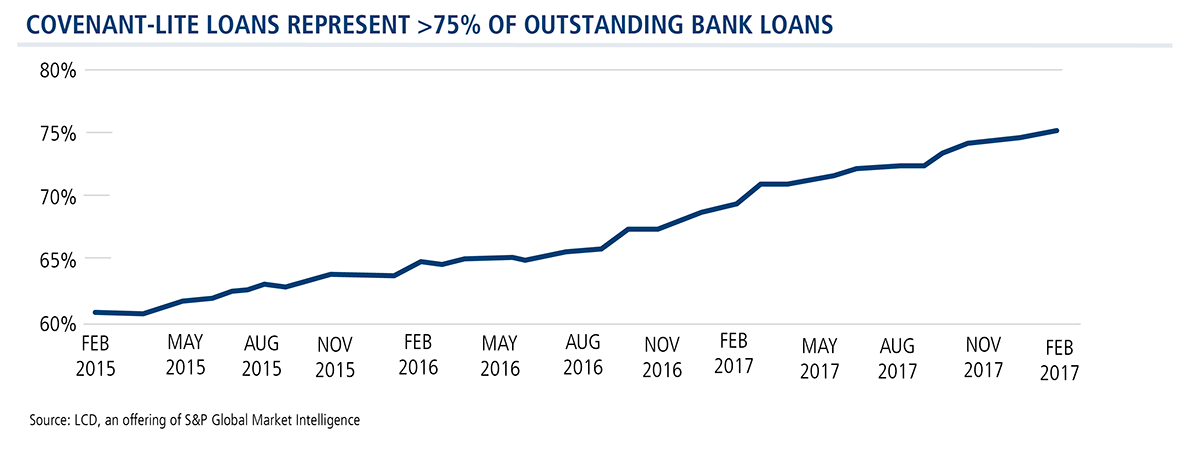

Bank loans that are issued with only incurrence covenants and no maintenance covenants are classified as covenant-lite. This is a term getting a lot of publicity in recent years as covenant-lite loans represent an increasing component of the overall market. Covenant-lite loans now represent over 75% of new loan issuance, and a similar percentage of the outstanding loan market.

Calamos invests in covenant-lite loans. Because the majority of issuance comes in that form, on a case-by-case basis we evaluate whether the additional risk is represented in our expected return analysis. If our team feels we are being well compensated for any additional risk that comes from a lack of maintenance covenants, we will invest.

While it is important to understand the specific covenants involved in any bank loan when investing, the mere presence of covenant-lite terms does not make a loan a bad investment. Most loans with maintenance covenants will never trigger a violation.

Historically, covenant-lite and full covenant loans defaulted at similar rates, although between the years of 2007-2012, defaults among covenant lite loans were actually lower than those with full covenants. The additional flexibility for issuers without maintenance covenants may have allowed borrowers to circumvent default. On the other hand, a lack of maintenance covenants can delay the inevitable in a truly bad situation and may lower the recovery rates for lenders.

Being well compensated for the risks taken is a fundamental component of our investment philosophy. Including bank loans in our investment universe affords our team an additional and valuable relative value lever in positioning our portfolios.

Our team is benchmark-aware, not benchmark-constrained. The flexibility to look outside the benchmark-defined opportunity set for investment options is an important tool in the toolbox of our active management investment process.