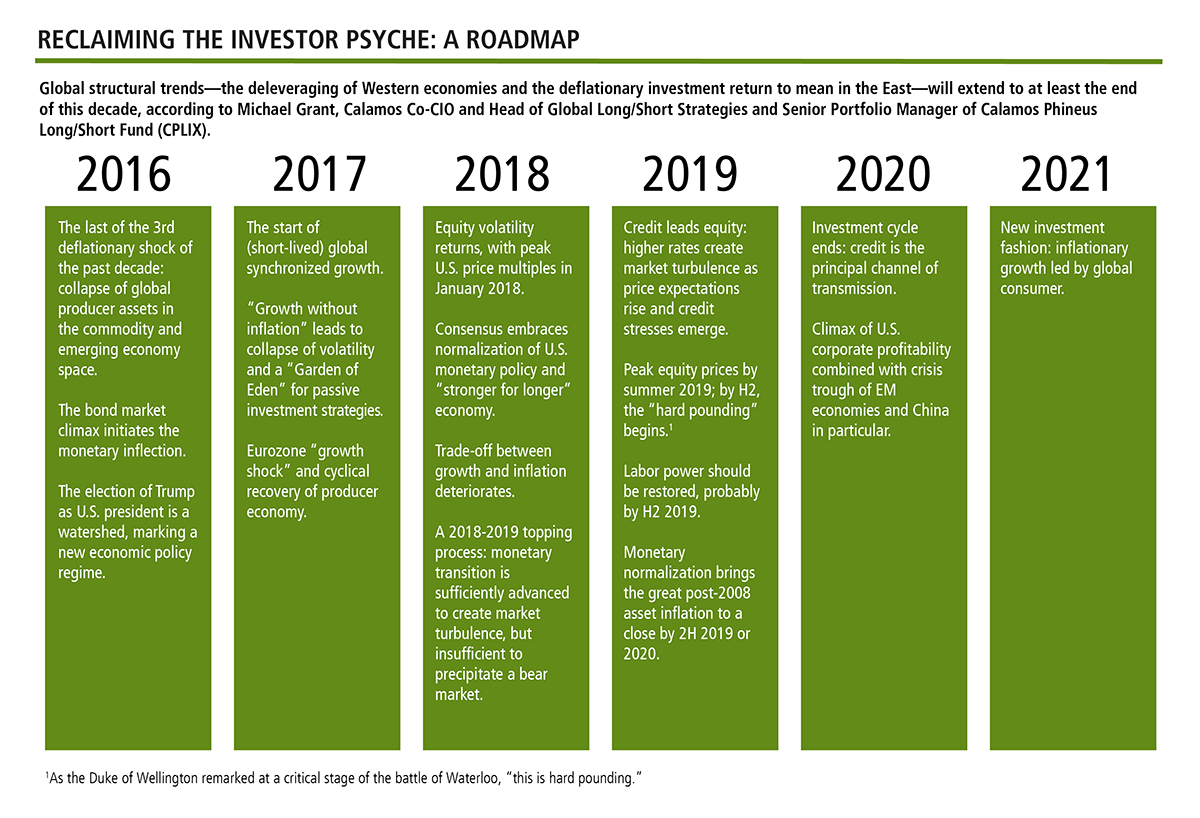

Reclaiming the Investor Psyche: A Roadmap

Michael Grant

Investment success requires taking on risk in exchange for return. Since John P. Calamos, Sr., founded Calamos Investments in 1977, our aim, as active managers, has been not to avoid risk, but to engage it in a sensible and measured manner.

But the years since the Global Financial Crisis (GFC) have skewed how investors think about risk. In the interest of stability, governments and central bankers alike have pursued policies that have remapped investors’ understanding of economic growth, corporate profitability and insolvency risk—and how all of these impact equity returns.

Today we begin a three-part series to help financial advisors think about how the investing landscape has changed, and what this implies for clients’ pursuit of investment returns for the remainder of the investment cycle. In this series, Michael Grant, Calamos Co-CIO, Head of Global Long/Short Strategies and Senior Portfolio Manager of Calamos Phineus Long/Short Fund (CPLIX), provides his perspective.

The U.S.: An Island of Economic Dynamism and Non-monetary Reflation

By some measures, the world has made a spectacular recovery from the Global Financial Crisis (GFC), including what Michael Grant considers “outsized” returns delivered by U.S. equities.

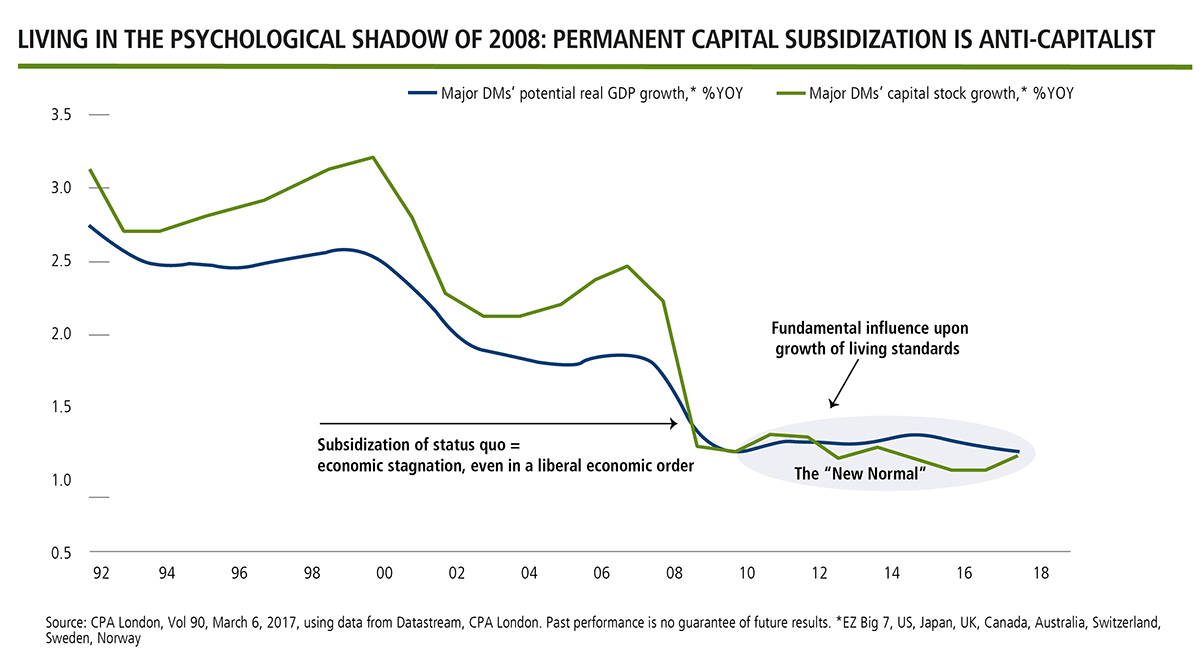

But Grant believes that years of Quantitative Easing (QE) have taken a toll. “Excessive monetary stimulus encourages malaise, misallocates capital and depresses productivity,” he says. “We have seen the symptoms of this across most of the developed economies.”

Grant notes the origins of QE were well founded and timely, with the leadership of the Federal Reserve playing a decisive role in the recovery of the U.S. economy. But “monetary super-stimulus should remain a palliative. Too much dependency for too long distorts the long-term health of the capitalist body,” says Grant.

Nearly a decade has passed since the crisis. And still, Grant believes, we live in its “psychological shadow.”

“The psyche of the financial community and policy-makers in the developed world is dominated by the suspicion of fragility and shared fear of relapse,” he says.

To be sure, this has been an unprecedented time, with the major economies continuing to surprise. But in the U.S., there is no longer an imminent source of systemic economic or financial risk on the horizon. A more normal monetary environment can be restored, helped along by the fiscal and tax reform initiatives of the Trump administration, insists Grant.

How do we recover from economic stagnation and financial repression? Grant’s view: There needs to be a monetary “return-to-more normal,” with an end to the destructive booms and busts that partly resulted from overreliance upon hyperactive monetary policy over the past quarter-century.

As a framework for understanding where we’ve been and the potential for future opportunities for financial advisors seeking to position clients’ risk assets, Grant provides a multi-year roadmap through 2021.

The U.S. equity market since 2008 demonstrates the power of market leadership, according to Grant. “Leadership equities, in terms of sectors and styles, are those that are best suited to the specific features of the investment cycle,” he adds.

Grant highlights two factors to explain the outperformance of U.S. equities:

- First, the U.S. acknowledged and responded to the challenges of the deflationary shock from its inception, facilitating a “first-mover advantage.” Reflecting American social preferences and “collective memory of the 1930s,” the Federal Reserve was determined to avoid the errors of that earlier period. “This pro-business, pro-creditor outlook is a virtue in a deflationary setting,” Grant says.

-

The second edge was the resilient profitability of corporate America. The collapse of the U.S. corporate cost of capital amid sustained U.S. corporate profitability is described by Grant as the “organizing paradigm” of the post-2008 investment cycle. In particular, cash accretive growth companies become acutely valuable in a slowly expanding world of no inflation.

“The extraordinarily low cost of capital for corporate America was the twin of the decline of expected returns on investment,” says Grant. “The falling cost of capital raised today's value of the future profits of comparatively safe growth stocks.” No other major market can compete with U.S. leadership in this respect.

This Growth Is Not ‘Profitless’

Financial assets reprice when investors come to realize that their interpretation of significant features of the investment environment is mistaken, says Grant. In late 2016 investors recognized that the momentum of the global upswing had been underestimated.

In most cycles, improved corporate profit margins should signal improved pricing power. The revival of corporate profitability and capital investment should translate sooner or later into upward pressure on output prices, Grant says.

Instead, he says, “expectations of sustained low inflation and modest growth in the developed world remain embedded in the investor psyche.”

“Sooner or later, higher inflation should materialize. The setting of ‘growth without inflation’ has a sell-by date, at least in the U.S., and investors are awakening to this. The growth that is evident across the global economy is not ‘profitless growth,’” insists Grant.

This link between the profitability regime and inflation expectations is a key debate for his roadmap.

The global upswing that started in 2017 was the most widespread revival of corporate profitability of the past decade because it included the recovery from the producer recession of 2015-2016. Profitability of almost all industries, across almost all regions improved in 2017.

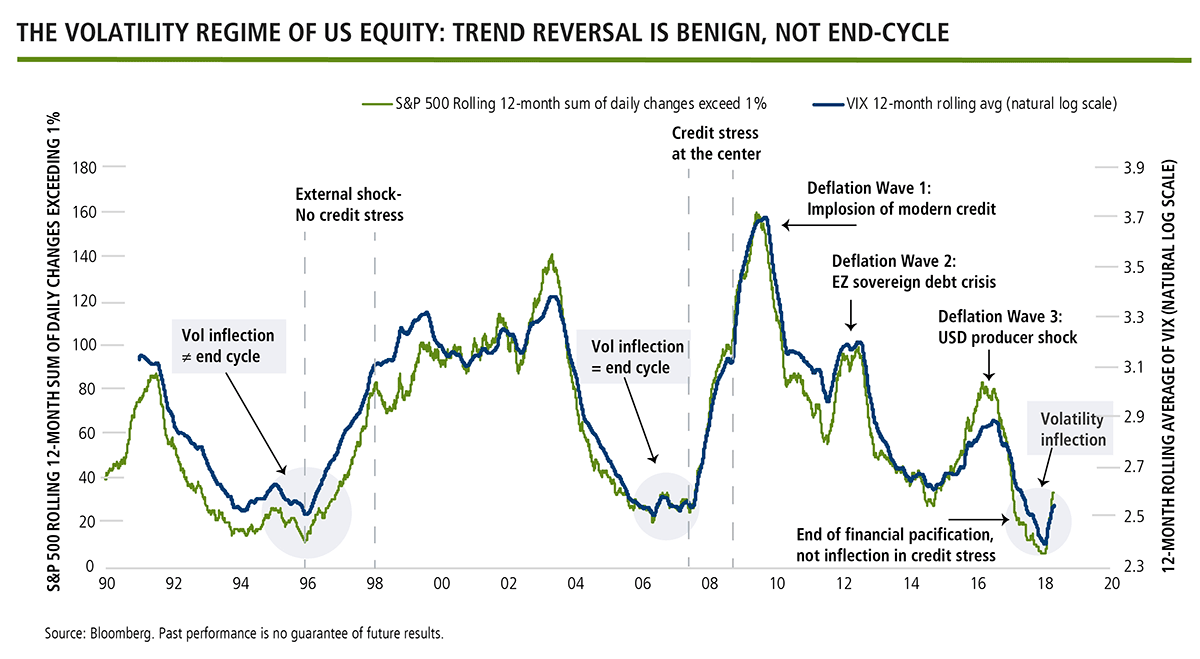

And then came the first quarter of 2018, which Grant considers “a decisive inflection.”

Q1 was the first setback in equities since 2008 that didn’t benefit the defensive sectors. Neither quality debt nor defensive equity in the developed markets delivered outperformance in the first four months of this year. This was what he considers “a genuine discontinuity”—and implies the equity cycle has entered its late stage.

“Most investors assume that higher equity volatility implies lower returns. Wrong,” says Grant.

“A transition to a more normal equity volatility does not necessarily imply lower returns for equities. The end of the investment cycle will be preceded by an increase in financial volatility led by trouble in the bond market." This is why the late-cycle debate is best viewed through the eyes of the credit community.

For now, Grant and the Global Long/Short Team’s view is that late-cycle is not yet end-cycle.

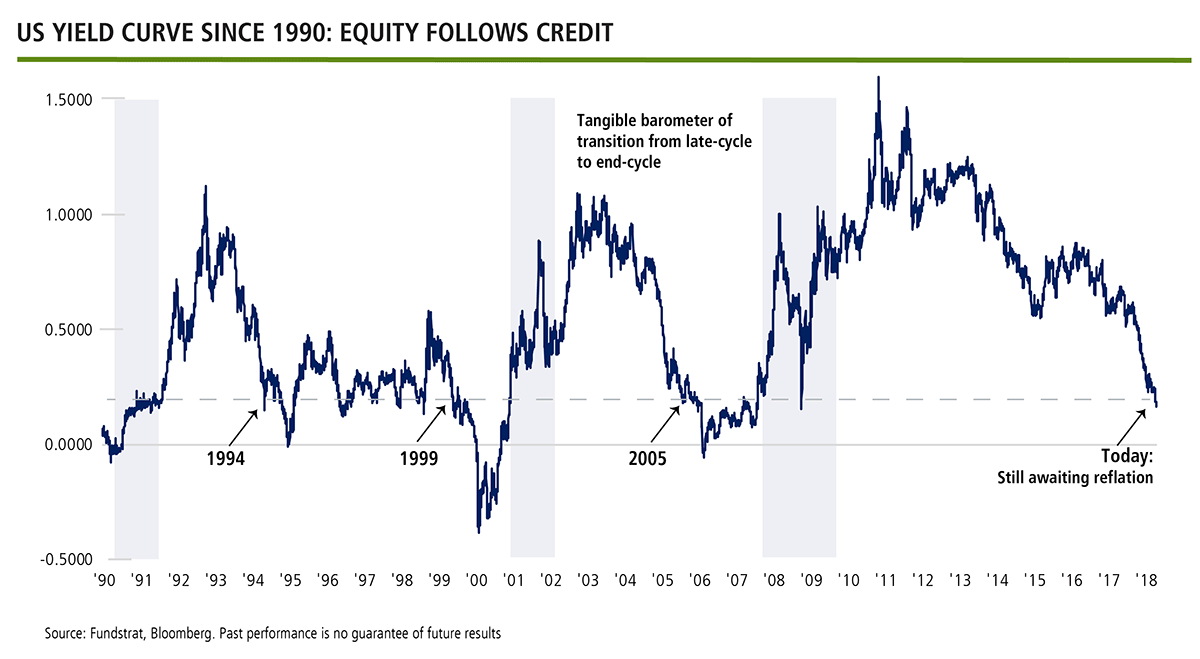

And for Grant this is the central debate today: Will higher rates be a problem for U.S. equities, as they often have been over the past three decades? Or do they signal the end of unease and apprehension after a long deflationary experience, creating a window for the bull market to continue?

Entering the Twilight Zone

Bond markets are not yet signaling the end of the low inflation world. But, Grant says, the post-2008 bull market is entering its “twilight zone”—the beginning of the end.

A window of excess returns opened after 2016 because the initial phase of higher interest rates is beneficial for risk assets. This signaled the relaxation of deflation anxiety, he says.

Higher bond yields are the principal barometer of reflation, a requirement for the extension of the equity bull market. The question is the degree to which higher yields reflect easing deflation and stronger growth on the one hand, versus rising credit risk and rising inflation expectations. In Grant’s view, the latter would generate a much more “disturbed” setting for equities.

Breaking Out of Economic Stagnation

Grant is most positive about the U.S. prospects for breaking out of economic stagnation.

The Quantitative Tightening (“QT”) being undertaken by the Federal Reserve is a true advantage for U.S. assets as it reverses what Grant calls the "economically distortive and socially fractious" effects of Quantitative Easing (QE). He looks for the return-to-mean of interest rates in the developed world to occupy the next several years.

The policy agenda of the Trump presidency is a pro-business message and signals that reflation will continue by non-monetary means. In the context of sub-4% U.S. unemployment, this mix of fiscal initiatives, tax reform, trade and deregulation implies the long awaited turn in the labor share of national incomes is near.

In short, the foundation for higher inflation led by wage growth, likely by 2019, has been set.

“Trump’s non-monetary reflation marks the end of the overreliance upon monetary policy in the U.S.,” says Grant. The Fed will not raise rates aggressively but it is explicitly telling us that monetary policy will become “modestly restrictive” by the end of the decade.

Since 2008, deflation anxiety has fed the long bull market in risk assets. Its comparative absence today is a warning of discontinuity, according to Grant. It suggests more disturbed markets into 2019-2020, including the return of the old axiom: what’s good for Main Street is not always good for Wall Street.

This “late-cycle” diagnosis of financial markets implies that profit growth will slow into 2019, because corporate costs will rise, even as the monetary environment becomes gradually less friendly. The trade-off between growth and inflation is starting to deteriorate, he says, and is the basis for his presumption for more disturbed markets.

The “emotional climax” of January marked the peak of the high momentum bullish phase, often associated with the peak of equity valuations. However, he says, we have not yet reached the end-cycle in terms of equity prices because corporate fundamentals are robust and the deterioration of the monetary environment is not sufficiently advanced.

“We are still some distance from the point where any central bank can be described as restrictive,” he says.

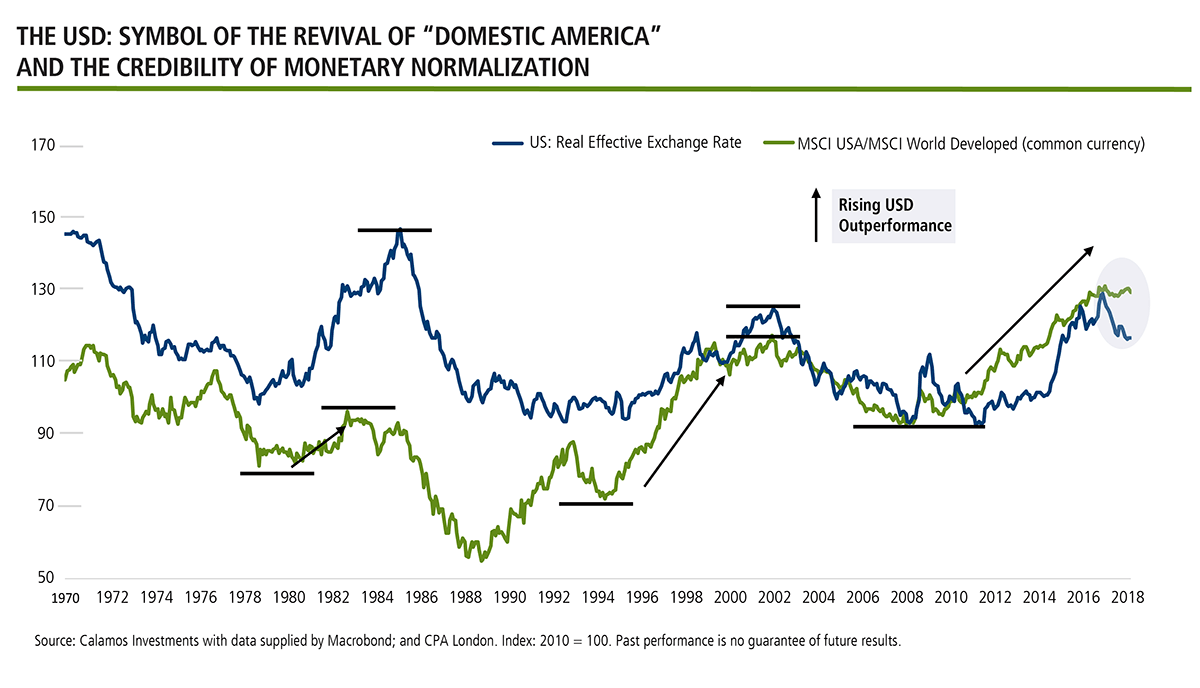

The U.S. dollar is a symbol of the revival of “domestic America” and the credibility of monetary normalization, according to Grant. Every extended period of U.S. dollar strength since the 1970s has been associated with the leadership of U.S. equities, measured in common currency. This is playing out again today.

Grant believes global capital flows are turning markedly in favor of the U.S. economy after decades of the opposite, when capital flowed into the emerging world after the collapse of the Soviet Union and the opening of China. Trump’s trade policies are reinforcing this, as will the gradual splintering of the world into major economic blocs.

The same cannot be said of European equity, as suggested by the graph above. Grant says, “Europe’s markets cannot bear for long the pressure of euro appreciation because there are few alternative, particularly domestic, sources of profitability. This overreliance on external markets is Europe's Achilles heel."

Also see: Part 2: A Global Long/Short View: Why Europe Is In Trouble

Advisors, for more information, talk to a Calamos Investment Consultant at 888-571-2567 or caminfo@calamos.com.