Calamos’ recently concluded year-end meeting featured a mix of our investment managers’ comments on 2016 and some thoughts on what 2017 may hold. Below are a few highlights.

Continued Slow Growth

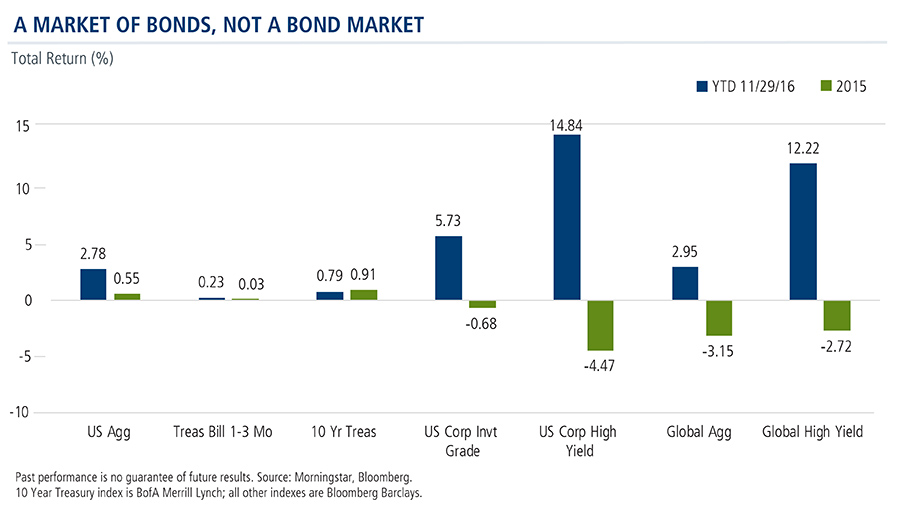

“It’s a market of bonds, not a bond market,” Co-Chief Investment Officer and Head of Fixed Income Strategies R. Matthew "Matt" Freund, CFA, likes to say. In support of the statement, Matt presented this bar chart on the varied performance year-to-date through November 29, 2016, of the different segments of the global bond market.

What could last week's interest rate hike coupled with the pro-growth deregulation positions of the incoming Trump administration mean for fixed income?

Investors always expect that increases in long-term rates will be parallel to those of short-term rates but this may not be the case, said Matt.

While growth is accelerating, optimism is tempered, he said. Since 1987, when Alan Greenspan became chairman of the Federal Reserve, the economy has been in a low- and slow-growth environment that will be hard to break out of.

Long-term rates may stay lower for longer than investors expect. According to Matt, long-term rates have followed a cyclical pattern with trends that have lasted decades—as suggested by this chart dating back to 1790.

Long-term rates may not bottom until the next recession, Matt told the Calamos distribution teams.

Retail Investors Underinvested for Likely Profit Expansion

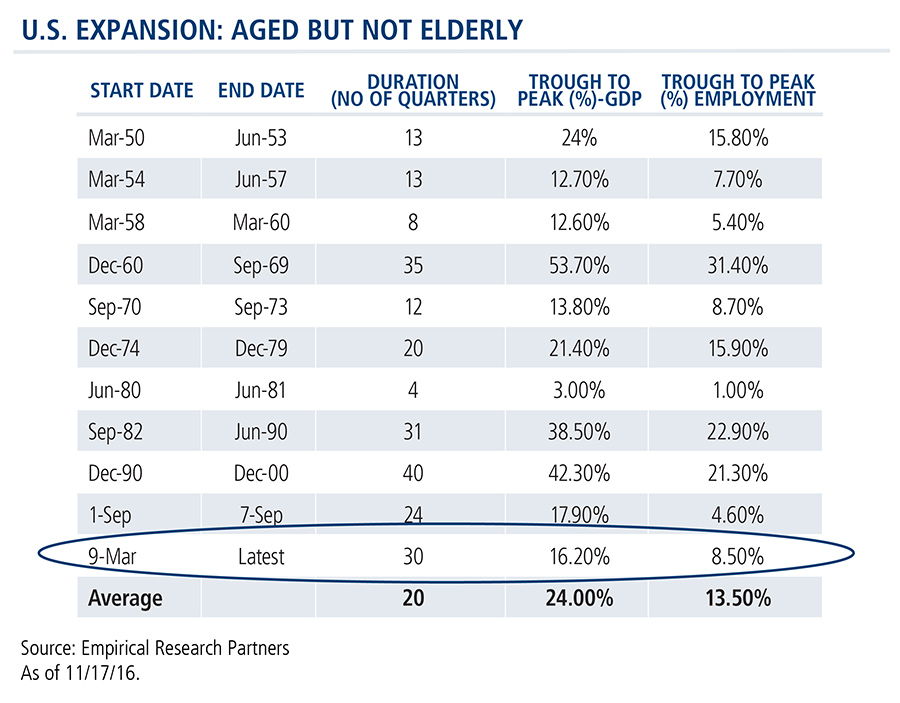

“What if the U.S. just had its [profit] recession?” asked

Michael Grant, Senior Vice President, Senior Co-Portfolio Manager and head of the Global Long/Short team. The current expansion, which began in March 2009, is the fourth in recent history. We’re mid-cycle, not late cycle, Michael believes, and he’s looking for a reflation of the United States middle class. (Also see

Thoughts on the Market In Light of Election Results.)

However, investors are poorly positioned for reflation, according to Michael, who presented this graph showing that equities are “an under-owned” inflation hedge. Since 2009, he noted, the only significant purchaser of equities has been the corporate sector. Household and pension fund weightings in equities are low. Since 2008, $1.4 trillion has flowed into global bond funds, while equity funds have seen outflows.

The coming year should have more upside than downside, Michael said—earnings expectations for MSCI USA sectors (shown below) assume an only modest recovery in nominal GDP.

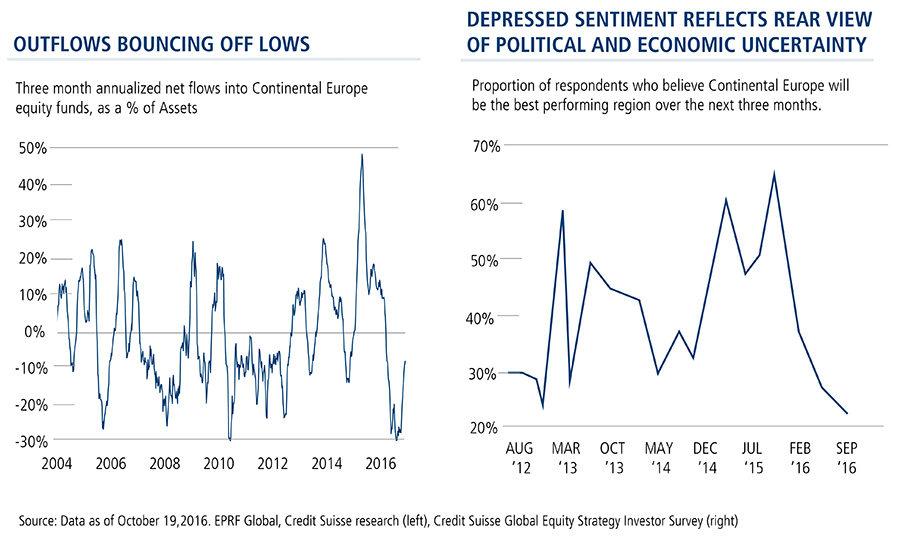

There’s reason to look for a positive “surprise” in Europe next year, too, according to Michael. Political uncertainty is driving investor pessimism, overshadowing the positive case to be made for equities based on European companies’ high operating leverage.

For more information, please talk to your Calamos Investment Consultant at 888-571-2567 or

caminfo@calamos.com.

Past performance is no guarantee of future results.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Information contained herein is for informational purposes only and should not be considered investment advice.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country's borders in a specific time period. Though GDP is usually calculated on an annual basis, it can be calculated on a quarterly basis as well.

Earnings per share (EPS) is the portion of a company's profit allocated to each outstanding share of common stock. Earnings per share serves as an indicator of a company's profitability.

Indexes are unmanaged, do not include fees and expenses and are not available for direct investment.

The MSCI U.S.A Index is designed to measure the performance of the large and mid-cap segments of the U.S. market. With 616 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the U.S.

Bloomberg Barclays U.S. Aggregate Bond Index: Is an unmanaged index composed of securities from the Bloomberg Barclays Government/Corporate Bond Index, Mortgage-Backed Securities Index and the Asset-Backed Securities Index. Total return comprises price appreciation/depreciation and income as a percentage of the original investment. Indices are rebalanced monthly by market capitalization.

Bloomberg Barclays U.S. Treasury Bills 1-3 Month Index: Is a component of the Short Treasury index. The Bloomberg Barclays Short Treasury Index includes aged U.S. Treasury bills, notes and bonds with a remaining maturity from 1 up to (but not including) 12 months. It excludes zero coupon strips.

BofA Merrill Lynch 10+ Year Treasury Index: Is a subset of the Bank of America Merrill Lynch Treasury Master Index. The index measures the total return performance of U.S. Treasury bonds with an outstanding par that is greater than or equal to $25 million. The maturity range of these securities is greater than ten years.

Bloomberg Barclays U.S. Corporate Bond Index: a rules-based market-value weighted index engineered to measure the investment grade, fixed-rate, taxable, corporate bond market. It includes USD-denominated securities publicly issued by U.S. and non-U.S. corporate issuers. To be included in the index a security mU.S.t have a minimum par amount of 250MM.

Bloomberg Barclays U.S. Corporate High Yield Index: Is an unmanaged index that is comprised of issues that meet the following criteria: at least $150 million par value outstanding, maximum credit rating of Ba1 (including defaulted issues) and at least one year to maturity.

Bloomberg Barclays U.S. Aggregate Corporate Index: An unmanaged index considered representative of the U.S. investment-grade, fixed-rate bond market.

Bloomberg Barclays Global Aggregate Bond Index: A measure of global investment grade debt from twenty-four different local currency markets. This multi-currency benchmark includes fixed-rate treasury, government-related, corporate and securitized bonds from both developed and emerging markets issuers.

Bloomberg Barclays Global High Yield Index: represents the U.S. High Yield Index, Pan-European High Yield Index, High Yield CMBS Index, and non-investment grade portion of the Bloomberg Barclays Global Emerging Markets Index.